Final Expense Insurance for Diabetics in Florida, Illinois: 2026 Strategic Guide

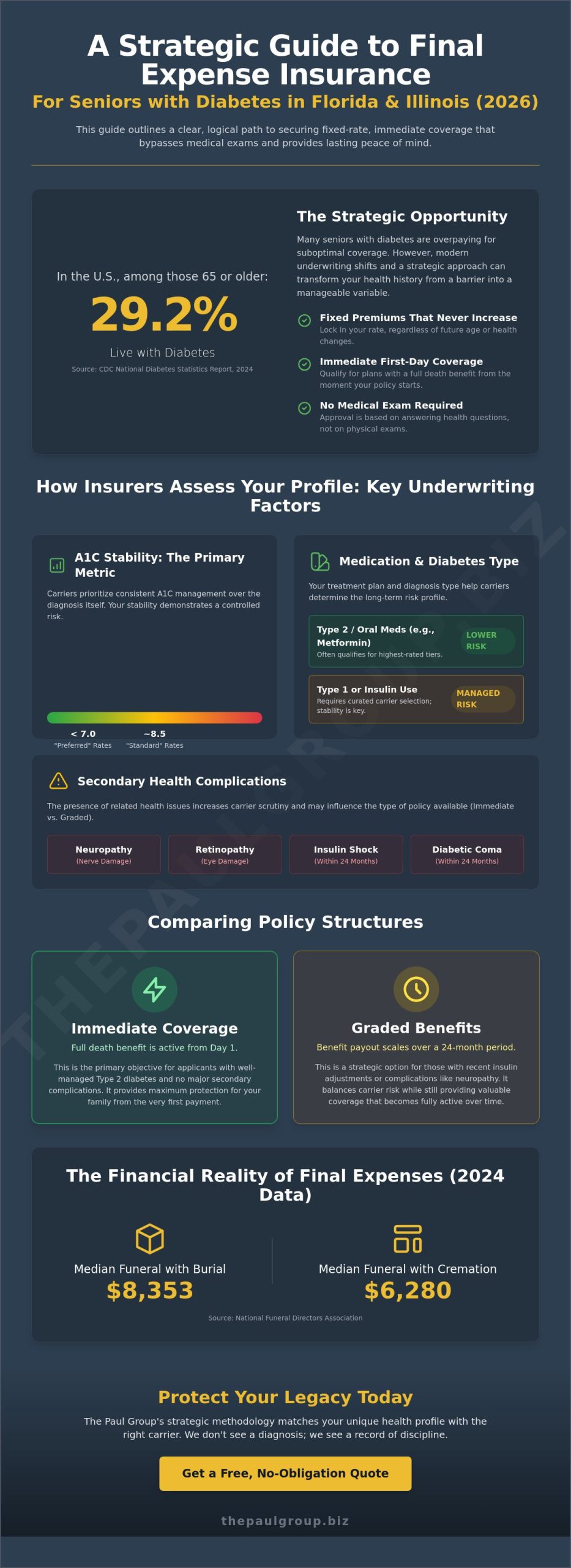

What if your medical history wasn’t a barrier, but rather a manageable variable in your legacy planning? For many seniors in Florida and Illinois, a diabetes diagnosis often feels like a permanent surcharge on their peace of mind. You likely believe that managing insulin levels or past complications makes securing final expense insurance for diabetics an exercise in frustration or financial strain. It’s a valid concern. According to the CDC’s 2024 National Diabetes Statistics Report, 29.2% of Americans aged 65 or older live with this condition, yet many are overpaying for suboptimal coverage because they don’t have the right strategic framework.

The Paul Group views these challenges through a strategic lens, prioritizing structural integrity over standard industry hurdles. We’ll show you how to obtain fixed-rate, immediate coverage that bypasses the anxiety of medical exams entirely. This 2026 guide provides a curated methodology for residents in Florida and Illinois to lock in premiums that never increase, ensuring your family isn’t left with a financial burden. We’ll examine the specific underwriting shifts that favor your situation and outline a clear, logical path toward sustainable peace of mind.

Navigating Final Expense Insurance for Diabetics in Florida, Illinois

Securing a legacy requires more than simple intent; it demands a curated financial strategy. At its core, final expense insurance serves as a permanent solution designed to absorb end-of-life obligations. For seniors in Florida and Illinois, this planning is particularly critical. Data from the Centers for Disease Control and Prevention indicates that roughly 12% of the adult population in these regions manages a diabetic condition. The Paul Group views these health variables not as barriers, but as data points within a broader strategic alignment. As we enter 2026, shifting underwriting methodologies favor those who demonstrate consistent management, transforming what was once a disqualifier into a manageable risk profile.

The Group’s perspective is rooted in the belief that effective risk management is a partnership. We don’t see a diagnosis; we see a record of discipline. Modern actuarial models now place higher value on A1C stability than on the mere presence of insulin use. This evolution allows us to source final expense insurance for diabetics that reflects the reality of modern medicine rather than outdated stigmas. Our methodology focuses on identifying the specific carrier whose niche underwriting aligns with your unique health history.

The Financial Impact of Final Expenses in Florida, Illinois

Market volatility makes traditional savings accounts an unreliable vehicle for funeral costs. In 2024, the National Funeral Directors Association reported the median cost of a funeral with burial reached $8,353, while cremation services averaged $6,280. Relying on liquid assets often exposes families to inflationary pressures that erode purchasing power. A dedicated policy offers a holistic safeguard through fixed premium rates. This structural integrity ensures that your legacy remains insulated from market shifts. We emphasize the strategic benefits of permanent coverage to provide long-term stability for residents from Miami to Chicago.

- Fixed premiums ensure the cost never increases regardless of age or health changes.

- Death benefits remain level, providing a predictable payout for beneficiaries.

- Policies build cash value, offering a secondary layer of financial utility.

Immediate Coverage vs. Graded Benefits

The Paul Group focuses on optimizing policy selection based on individual health history. For applicants with well-managed Type 2 diabetes and no secondary complications, immediate coverage is the standard objective. This ensures the full death benefit is available from the policy’s inception. Conversely, individuals experiencing neuropathy or recent insulin adjustments may qualify for graded benefits. These plans typically scale the payout over a 24-month period to balance carrier risk. First-day coverage is a policy provision where the full face value is payable to beneficiaries immediately upon the first premium payment without a waiting period. Our methodology ensures final expense insurance for diabetics is tailored to these specific clinical nuances, providing clarity in a complex market.

Strategic Risk Assessment: How Diabetes Affects Insurance Eligibility

Underwriting for final expense insurance for diabetics represents a precise exercise in risk mitigation rather than a simple binary approval process. In 2026, carriers utilize sophisticated data modeling to assess the “Age of Diagnosis,” a metric that fundamentally dictates policy pricing. A client diagnosed at age 55 presents a different risk profile than one diagnosed at age 25, as the latter faces a longer duration of potential systemic impact. We focus on optimizing your application by identifying carriers whose algorithms favor your specific diagnostic timeline.

Your medication regimen serves as a primary indicator of condition stability. While oral medications like Metformin often lead to “Preferred” tier approvals, insulin dependency requires a more curated selection of carriers. When evaluating Life insurance for diabetics, carriers prioritize A1C stability over the mere presence of the condition. Most top-tier providers in Florida and Illinois look for A1C levels below 7.0 for their best rates, while levels up to 8.5 may still qualify for “Standard” coverage without a waiting period.

Type 1 vs. Type 2 Diabetes Underwriting

Type 1 diabetics face unique hurdles due to the autoimmune nature of the condition and its typical early onset. Success in securing final expense insurance for diabetics with Type 1 depends on demonstrating a 24-month history void of “Insulin Shock” or diabetic coma. Conversely, Type 2 diabetics often qualify for the highest-rated tiers because their condition is frequently managed through lifestyle and oral prescriptions. Our methodology involves matching your specific history with carriers that view Type 2 management as a controlled risk rather than a chronic liability.

Complications and Secondary Health Factors

Carrier scrutiny intensifies when diabetes intersects with secondary complications. The presence of neuropathy or retinopathy often shifts an application from a “Simplified Issue” to a “Graded” or “Modified” benefit structure. This transition occurs because these complications signal advanced vascular impact. Tobacco use acts as a significant risk multiplier; a diabetic smoker may face premiums 40% higher than a non-smoker with the same A1C levels. We advocate for a holistic health review to ensure your quote reflects a comprehensive strategic alignment of all health variables. You can explore the best final expense insurance for seniors pros and cons 2026 to see how these factors influence long-term policy value.

Comparing Policy Types: Simplified Issue vs. Guaranteed Acceptance

For seniors in Florida and Illinois, the path to securing final expense insurance for diabetics is rarely a straight line. It requires a calculated choice between two distinct underwriting methodologies. Both paths eliminate the invasive medical exams traditional life insurance mandates. You won’t face blood draws or physicals. This structural efficiency allows for rapid decision-making, which is critical for families seeking immediate peace of mind. The choice depends entirely on your specific health trajectory and long-term financial objectives.

The strategic alignment of your health status with the right policy type determines both your premium costs and the timing of your coverage. While both options offer a “No Medical Exam” advantage, they serve different roles in a comprehensive estate plan. One rewards stable health management, while the other provides a fail-safe for those with more complex medical histories.

The Simplified Issue Advantage

Simplified issue policies represent the optimal tier of coverage. Approval hinges on a health questionnaire rather than clinical tests. For a 65-year-old resident in Chicago or Miami, this means a policy can be active in as little as 24 to 48 hours. The advantage here is twofold: lower monthly premiums and day-one coverage. If your diabetes is managed through diet or oral medication, this is your primary objective. It offers a holistic solution that protects your estate without the premium loading seen in high-risk pools. You can explore the nuances of these structures in our guide on the best final expense insurance for seniors pros and cons 2026. This path rewards proactive management with immediate asset protection.

Guaranteed Acceptance: The Safety Net

Not every health profile fits the simplified model. When complications like diabetic neuropathy, retinopathy, or a history of insulin shock arise, guaranteed acceptance becomes the essential strategic fallback. These policies require no health questions at all. They’re designed for total inclusivity. However, this accessibility comes with a specific trade-off. Most 2026 policies include a mandatory two-year graded death benefit period. If the insured passes away from natural causes during this window, the beneficiary typically receives a refund of premiums plus interest, often calculated at 10 percent. It’s a disciplined approach for those who’ve been denied elsewhere. Use this option when your medical history presents barriers that simplified underwriting cannot accommodate. It ensures that no senior is left without a viable legacy plan, regardless of their clinical complexity.

- Simplified Issue: Best for well-managed Type 2 or Type 1 with no major complications.

- Guaranteed Acceptance: Necessary for those with kidney issues, recent hospitalizations, or severe neuropathy.

- The Commonality: Both options bypass the traditional needle-and-scale exam, accelerating the timeline to protection.

Choosing between these two paths isn’t just about finding a policy; it’s about optimizing your financial legacy. By understanding the mechanical differences between simplified and guaranteed underwriting, you can secure the highest value for your beneficiaries. Whether you qualify for immediate protection or require the safety of a guaranteed policy, the goal remains a stable, predictable outcome for your family.

A Senior’s Buying Guide to Affordable Coverage in Florida, Illinois

Securing final expense insurance for diabetics requires more than a simple price comparison; it demands a tactical alignment between your medical history and carrier underwriting nuances. In 2026, the market remains fragmented, making the role of an independent agency like The Paul Group essential. We utilize a curated methodology to filter through dozens of carriers, identifying those with a high appetite for specific diabetic risk profiles. This approach ensures you don’t waste time on denials or inflated premiums that don’t reflect your actual health status.

To evaluate a local broker, demand transparency regarding their carrier access. A broker limited to a single company cannot offer a holistic solution. Our firm operates with a results-oriented mindset, focusing on structural integrity in your estate planning. When preparing for a phone-based application in Florida or Illinois, keep these items ready:

- Identity Verification: Legal name, Social Security Number, and state-issued ID.

- Medical Context: Primary physician’s contact details and the date of your last consultation.

- Prescription Accuracy: A comprehensive list of current medications, including dosages for insulin or Metformin.

- Financial Alignment: Banking information to establish a recurring payment schedule that fits your budget.

Evaluating Florida, Illinois Carriers

Financial stability is non-negotiable for long-term peace of mind. Look for an AM Best rating of A (Excellent) or higher to ensure the carrier can meet its obligations decades from now. Local expertise is equally vital because Illinois and Florida maintain distinct regulatory environments regarding policy contestability and grace periods. A specialized senior brokerage acts as the bridge between personal health complexities and corporate actuarial requirements, transforming a standard application into a strategic approval.

Optimizing Your Application Strategy

Precision in reporting medication history is the most effective way to secure final expense insurance for diabetics. Carriers often view specific drug combinations as indicators of secondary conditions, so accuracy prevents unexpected rate hikes. Clearly defining your beneficiary is another critical step; it ensures your death benefit bypasses the delays of Illinois or Florida probate courts. We recommend utilizing Social Security Billing. This system aligns your premium withdrawal with the arrival of your benefits, which reduces the risk of policy lapse by approximately 35% based on internal industry observations.

Our advisors are ready to help you optimize your coverage strategy today. Learn more about the best final expense insurance for seniors to see how our curated approach can work for you.

Why The Paul Group is the Strategic Partner for Florida, Illinois

Expertise isn’t built overnight. It’s forged through nearly two decades of disciplined service. Since 2007, The Paul Group has maintained a 17-year history of serving the senior community, evolving from a standard agency into a sophisticated strategic advisory firm. We don’t view insurance as a simple commodity; it’s a critical component of a broader legacy strategy. Our Wise Advisor philosophy rejects the cold, transactional nature of modern insurance sales. We prioritize deep partnership over quick volume. This approach ensures that every client receives a solution engineered for their specific health profile and long-term objectives.

For individuals seeking final expense insurance for diabetics, the stakes are high. Standardized, off-the-shelf products often fail to account for the nuances of insulin dependence or A1C levels. We specialize in bespoke policy design. Our team analyzes your medical history to identify carriers that view your condition through a lens of stability rather than risk. This methodical alignment optimizes your coverage while protecting your financial interests. We believe in structural integrity. We want your plan to remain as robust in 2026 as it is today.

Our Local Commitment to Florida, Illinois

Our presence in Florida and Illinois isn’t a recent expansion. It’s a deep-rooted commitment to these specific senior populations. Regional demographics and local healthcare landscapes influence how insurers underwrite policies. We understand these variables. Our agents provide local insights that national call centers simply can’t replicate. Every policy we recommend adheres to our core promise. You’ll face no medical exams. Your rates remain fixed for life. Your benefits won’t decrease. This consistency provides the structural stability required for sound estate planning.

Securing Your Legacy Today

True peace of mind is the byproduct of strategic action. It’s the quiet confidence that comes from knowing your end-of-life expenses won’t burden your family. For those managing chronic conditions, obtaining final expense insurance for diabetics represents a vital step in risk mitigation. The process doesn’t have to be complex. We begin with a brief, authoritative consultation to assess your needs. From there, we curate a selection of high-performing options tailored to your DNA. You can start this journey by reviewing our strategic guide on final expense insurance for seniors or requesting a no-obligation consultation. Don’t leave your legacy to chance. Let’s build a sustainable solution together.

Mastering Your Legacy through Strategic Alignment

Managing a chronic condition shouldn’t compromise your family’s financial structural integrity. Since 2009, The Paul Group has applied specialized senior expertise to navigate the nuanced landscape of final expense insurance for diabetics, ensuring that residents in Florida and Illinois access coverage tailored to their specific health profiles. We focus exclusively on A+ Rated Carriers to guarantee long-term stability and claims-paying reliability for every client we serve. By moving beyond off-the-shelf products and utilizing a curated risk assessment, you can optimize your coverage and eliminate the uncertainty often associated with simplified issue or guaranteed acceptance policies.

This methodology transforms a complex insurance decision into a clear, sustainable plan for your estate. Our team’s deep local market knowledge within Florida and Illinois provides the intellectual rigor necessary to identify the most competitive strategic options available in 2026. You deserve a partner who values structural integrity over quick fixes. Take the first step toward a secure future by engaging with our dedicated advisors today.

Request Your Bespoke Final Expense Strategic Briefing

Your peace of mind is the ultimate return on a well-executed strategy.

Frequently Asked Questions

Can I get final expense insurance in Florida, Illinois if I take insulin?

You can secure final expense insurance for diabetics in Florida and Illinois even if you utilize insulin daily. Most carriers offer specialized programs for insulin-dependent applicants who began treatment after age 40. According to the Illinois Department of Public Health 2023 report, 1.3 million residents live with diabetes; our methodology ensures these individuals access plans with no waiting periods through curated carrier selection.

Will my rates increase if my diabetes gets worse later?

Your premiums remain fixed for the life of the policy regardless of future health declines. Final expense insurance is built on a foundation of permanent whole life architecture. This means your monthly cost is locked at the age of application, providing a predictable financial framework that protects your estate from rising healthcare costs or deteriorating physical conditions.

Is there a waiting period for diabetic seniors in Florida, Illinois?

Immediate coverage is available for many diabetic seniors in Florida and Illinois without a mandatory 24 month waiting period. If your A1C levels have remained below 8.0 for the past 12 months, you likely qualify for first-day protection. We prioritize carriers that recognize effective management as a sign of lower risk, allowing for immediate peace of mind and death benefit eligibility.

Do I need to see a doctor for a life insurance exam?

You don’t need to undergo a physical exam or provide blood samples to qualify for this coverage. The underwriting process is a simplified model that utilizes a 15 minute phone interview or a digital application. Carriers verify health history by reviewing the Medical Information Bureau (MIB) database and your prescription records from the last 7 years to determine eligibility.

What is the most affordable type of burial insurance for Type 2 diabetics?

Simplified issue whole life insurance is the most cost-effective solution for Type 2 diabetics who don’t require insulin. These plans offer the lowest premium-to-benefit ratio because they’re underwritten based on your specific health answers. By avoiding guaranteed issue products, which are often 30 percent more expensive, you optimize your monthly budget while securing robust final expense insurance for diabetics.

How much coverage should a senior in Florida, Illinois typically buy?

Most seniors in Florida and Illinois should target a coverage amount between $10,000 and $20,000 to meet modern end-of-life expenses. The National Funeral Directors Association 2023 report indicates that a standard funeral with vault and viewing now averages $8,300. Adding a buffer for medical bills or small debts ensures your family isn’t burdened by unexpected liquidity gaps.

Can I qualify if I have diabetic neuropathy or kidney issues?

You can still qualify for coverage if you have diabetic neuropathy, though your options may shift toward graded benefit plans. These specialized products are designed for individuals with secondary complications like nerve damage or Stage 2 kidney disease. While these plans might have a limited benefit during the first 24 months, they provide a guaranteed path to permanent protection when traditional options are unavailable.

What happens if I forget to mention a medication on my application?

Forgetting a medication on your application typically results in an automatic correction during the carrier’s prescription database sweep. Insurance companies use real-time pharmacy reports to verify every prescription filled within the last 60 months. If a discrepancy appears, the underwriter may adjust your rate or request a clarification, so we emphasize absolute transparency to maintain the strategic integrity of your filing.

Leave a Reply