Burial Insurance for Low Income Seniors in Florida, Illinois: A 2026 Strategic Guide

What if the most profound act of leadership you exercise for your family isn’t an inheritance, but the absolute removal of financial uncertainty? For many, securing burial insurance for low income seniors feels like a complex organizational challenge that clashes with a rigid monthly budget. We recognize that for residents in Florida and Illinois, the desire to protect loved ones often competes with the reality of a fixed income. You shouldn’t have to choose between current stability and a dignified legacy.

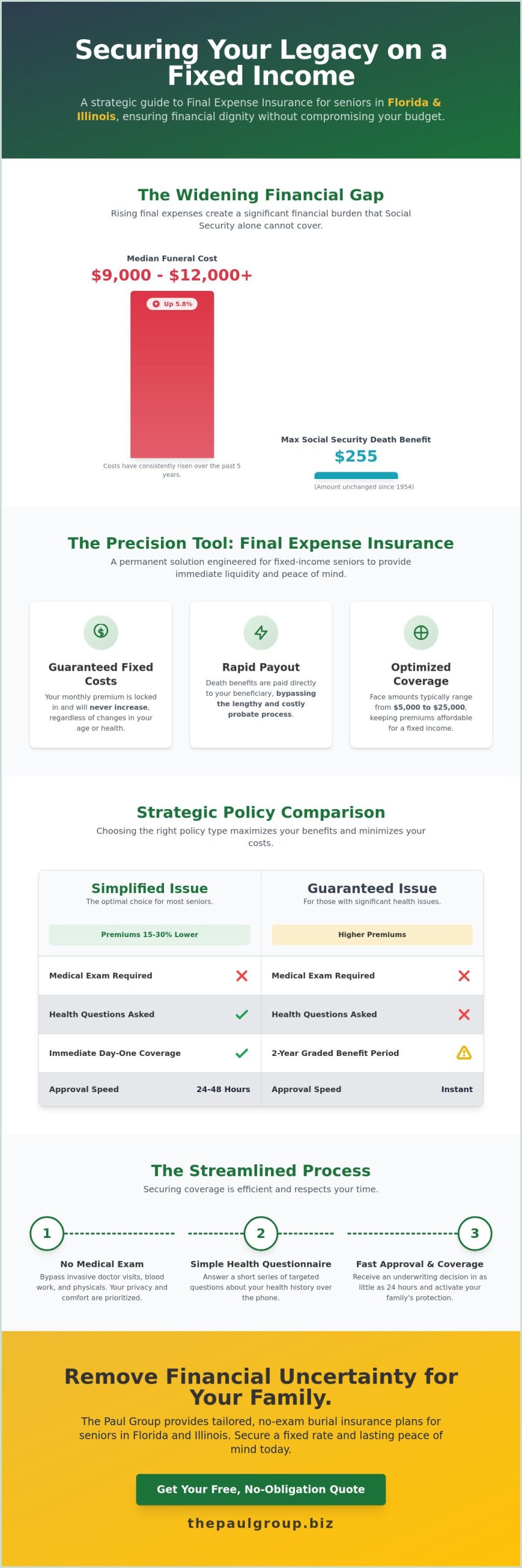

This strategic guide clarifies the 2026 landscape for final expense planning, ensuring you can secure a plan that requires no medical exams and guarantees rates that will never increase. According to 2023 industry projections, the median cost of a funeral increased by 5.8% over the previous five years, making a disciplined methodology for your legacy more critical than ever. We’ll examine the specific criteria for Florida and Illinois residents, detailing how to optimize your coverage while maintaining total fiscal control.

The Strategic Importance of Burial Insurance for Low-Income Seniors in Florida, Illinois

For seniors living on fixed incomes in Florida and Illinois, financial planning isn’t just about wealth accumulation; it’s about maintaining structural integrity at the end of life. Burial insurance for low income seniors serves as a precision-engineered tool designed to mitigate the immediate liquidity crisis that follows a death. Traditional life insurance policies often demand rigorous medical underwriting or carry high premium thresholds that don’t align with a modest budget. These legacy products fail because they prioritize long-term estate building over immediate, tactical cash flow needs. The Paul Group views burial insurance as the foundation of Financial Dignity, a strategic objective that ensures a senior’s legacy isn’t defined by debt or state-funded disposal.

Understanding Final Expense Realities in Florida, Illinois

In 2026, the cost of final services in the Florida and Illinois corridors continues to reflect broader inflationary pressures on labor and logistics. While specific prices fluctuate by county, the upward trajectory of service fees remains constant. Social Security provides a one-time death benefit of only $255, a figure that hasn’t changed since 1954. This leaves a massive capital gap that families must bridge within 48 hours of a loss. Without a dedicated funding mechanism, the burden often falls on survivors who are already struggling with their own economic pressures. You can analyze the best final expense insurance for seniors pros and cons 2026 to see how these plans bridge that specific gap through disciplined capital allocation.

Why “Burial Insurance” is the Precise Tool for the Task

Generic life insurance plans are often too broad for the specific requirements of a fixed-income household. Strategic understanding life insurance reveals that burial insurance is a permanent solution with level premiums. These policies offer small face amounts, typically ranging from $5,000 to $25,000, which optimizes monthly cash flow by keeping premiums affordable. The Paul Group focuses on these curated plans because they provide immediate protection without the volatility of term products.

- Fixed Costs: Premiums never increase regardless of age or health changes.

- Liquidity: Death benefits are paid directly to beneficiaries, bypassing lengthy probate processes.

- Equity: Policies build small amounts of cash value over time, providing a layer of financial fallback.

This methodology ensures that burial insurance for low income seniors remains a sustainable part of a monthly budget while providing total certainty. It’s a disciplined intervention against the unpredictability of the market. We believe that every senior deserves a plan that respects their current financial reality while securing their future transition. By choosing a plan tailored to the specific regulatory and economic environments of Florida and Illinois, families can achieve a state of clarity that generic policies simply cannot offer.

Strategic Coverage: Understanding Simplified Issue for Low-Income Profiles

Securing burial insurance for low income seniors requires a shift from broad market searches to a more disciplined, strategic methodology. The Paul Group identifies Simplified Issue life insurance as the primary vehicle for this transformation. This specific product class bypasses the traditional medical exam, replacing it with a targeted health questionnaire designed to assess risk through data rather than physical intervention. It’s a streamlined process that prioritizes efficiency without sacrificing the intellectual rigor of sound underwriting.

Bypassing the Medical Exam: How it Works

The health questionnaire acts as a disciplined diagnostic tool. Rather than requiring blood work or physician statements, carriers in Florida and Illinois utilize real-time database queries to analyze prescription histories and previous insurance applications. This approach allows for approval windows as short as 24 to 48 hours. For seniors managing chronic but controlled conditions, this speed provides a clear path to stability. The Paul Group facilitates this by identifying carriers whose underwriting niches align with specific health profiles, ensuring that a history of hypertension or managed diabetes doesn’t become a barrier to entry.

Simplified vs. Guaranteed Issue: Which is More Strategic?

The distinction between these two paths is a matter of capital optimization. Simplified Issue plans typically offer premiums that are 15% to 30% lower than Guaranteed Issue alternatives. More importantly, they provide immediate, day-one coverage. Guaranteed Issue plans often include a two-year graded benefit period; if the insured passes away during this time, the payout is limited to a return of premiums plus interest. Qualifying for Simplified Issue is a significant financial win for a limited budget because it maximizes the death benefit from the first payment.

While local safety nets like Pinellas County’s Burial and Cremation Program exist for those in extreme financial distress, private burial insurance for low income seniors offers a level of autonomy and choice that public programs cannot match. Choosing the right plan involves a careful analysis of the pros and cons associated with each policy type. Our group focuses on curated carrier selection to ensure our clients don’t settle for graded benefits when their health profile warrants immediate protection. If you’re ready to evaluate your eligibility for these strategic options, you can consult with our advisory team to begin your assessment.

Financial Optimization: Comparing Affordable Burial Insurance Options

True financial optimization requires looking past the surface level cost of a monthly premium. For many, burial insurance for low income seniors is viewed as a burden; however, it functions as a critical asset when structured with precision. We evaluate these options based on their long-term stability and their ability to protect a fixed income from future volatility. Sophisticated planning ensures that the death benefit remains intact while the cost of entry remains manageable. High quality coverage isn’t a luxury. It’s a strategic necessity that protects the family unit from sudden, unmanageable debt.

The Paul Group views these policies as structural tools. We move beyond the transactional nature of the insurance industry to focus on sustainable scaling of your final estate. By identifying the intersection of premium affordability and benefit reliability, we help seniors in Florida and Illinois secure their legacy without compromising their current quality of life.

Fixed Rates vs. Increasing Premiums

Many seniors fall into the trap of teaser rates found in term life policies. These products often feature premiums that escalate every five years or expire entirely once the policyholder reaches age 80. This creates a dangerous liability. Permanent burial insurance offers level premiums, meaning the rate locked in today remains the same for life. This strategic alignment is vital for those on Social Security. It eliminates the risk of losing coverage when it’s needed most. You can explore a deeper technical comparison in our curated guide on the best final expense insurance for seniors pros and cons 2026.

Sizing Your Policy to Your Strategic Needs

Determining the correct coverage amount is a matter of precision. Over-insuring wastes monthly capital. Under-insuring leaves families with a deficit. According to 2024 data from the National Funeral Directors Association, the median cost of a funeral with viewing and burial is approximately $8,300. In states like Florida and Illinois, medical debt or probate costs can also impact the final estate. A $10,000 policy is often the optimal strategic anchor for low-income seniors. This amount covers the core service while providing a modest buffer for administrative fees or final utility bills. Our methodology focuses on this Goldilocks zone to ensure every dollar spent serves a specific purpose.

- Level Benefit: The full face value is available from day one if health requirements are met.

- Cash Value Accumulation: Some permanent policies build a small equity component over decades.

- Guaranteed Renewability: The carrier cannot cancel the policy as long as premiums are paid.

Selecting burial insurance for low income seniors isn’t about finding the cheapest price. It’s about finding the most resilient contract. We look for providers with a history of claims-paying excellence. This ensures that when the time comes, the transition of funds is seamless and professional.

Implementation: Securing Your Policy in Florida, Illinois

Moving from the conceptual phase to active coverage requires a disciplined, strategic framework. At The Paul Group, we view the acquisition of burial insurance for low income seniors as a critical structural optimization for your family’s future. It’s not merely a transaction; it’s the establishment of a financial firewall. Our approach replaces the typical confusion of insurance shopping with a streamlined, executive-level process that prioritizes your time and your legacy.

The 4-Step Enrollment Methodology

Our methodology is engineered to minimize friction while maximizing the precision of the fit. We follow a rigorous progression to ensure your policy remains a sustainable asset rather than a financial burden. This structured path provides the clarity necessary for confident decision-making.

- Step 1: Strategic Consultation. We define your budgetary boundaries to ensure the premium aligns perfectly with your monthly cash flow.

- Step 2: Curated Carrier Selection. We filter through carriers authorized in Florida and Illinois to find those with the most favorable underwriting for your specific profile.

- Step 3: Qualification Interview. You’ll complete a brief health-based assessment. There’s no physical exam or invasive medical testing required.

- Step 4: Policy Activation. We finalize the documentation and deliver your coverage guarantee, providing immediate protection for your beneficiaries.

Navigating Local Florida, Illinois Requirements

Regional nuances often dictate the success of an application. In Illinois, the Department of Insurance mandates specific cost disclosures that must be presented clearly to every applicant. Florida’s regulatory landscape requires precise documentation regarding policy replacement to protect seniors from unnecessary churn. The Paul Group maintains a deep bench of expertise in these jurisdictions, ensuring every application meets 2026 compliance standards. We handle the bureaucratic complexity so you can focus on the long-term vision for your estate.

Strategic beneficiary designation serves as the final component of this implementation. It’s a calculated move to ensure funds bypass the delays of probate. By designating a specific individual or trust, you ensure the capital is available exactly when it’s needed. This level of foresight is what separates a standard policy from a comprehensive legacy plan. For those exploring burial insurance for low income seniors, this direct transfer of benefits is the ultimate tool for preserving family dignity during a transition.

Effective planning requires an understanding of both the advantages and the potential pitfalls of different products. To better understand how these choices impact your strategy, review our analysis of the best final expense insurance for seniors pros and cons for 2026.

Ready to secure your family’s financial future? Partner with The Paul Group today to begin your strategic enrollment.

The Paul Group: Tailored Final Expense Solutions for Local Seniors

Since 2009, The Paul Group has functioned as a strategic collective focused on the long-term security of the senior community. We reject the high-pressure tactics common in the insurance industry. Our firm operates on the principle that financial protection is a cornerstone of family stability. We combine deep industry expertise with a partnership-driven mindset. This approach ensures that every client receives a solution engineered for their specific circumstances. We bridge the gap between human empathy and operational excellence. Our methodology treats your legacy as a project requiring precision and care.

The Wise Advisor Advantage

A single captive agent is tethered to the products of one company. This often results in suboptimal coverage or inflated premiums because the agent lacks the flexibility to shop for better rates. The Paul Group operates as a specialized brokerage. We maintain a curated portfolio of top-rated carriers to ensure our clients have access to the most competitive structures available. In Florida and Illinois, our local expertise allows us to account for regional cost-of-living adjustments and state-specific protections. We provide the intellectual rigor necessary to identify the ideal burial insurance for low income seniors without compromising on quality. Our commitment to these communities is rooted in years of localized data and successful client outcomes.

- Access to a diversified portfolio of A-rated insurance carriers.

- Strategic alignment of policy terms with specific household budgets.

- Deep understanding of 2026 regulatory changes in Florida and Illinois.

- A focus on long-term structural integrity rather than quick, superficial fixes.

Your Path to Peace of Mind

Achieving financial peace of mind is a deliberate act of leadership for your family. It transforms a potential crisis into a managed transition. We believe that limited financial resources shouldn’t preclude a senior from accessing high-level advisory services. Our methodology focuses on optimization. We find the intersection where affordability meets comprehensive protection. This ensures that your final expenses are handled with dignity. It’s about creating a sustainable plan that stands the test of time.

Low income is not a barrier to professional strategic planning; it is a reason to pursue it with greater discipline. We invite you to take the next step toward structural financial integrity. Contact us for a no-obligation strategic briefing to review your 2026 options. Exploring the best final expense insurance for seniors is the first step toward securing a legacy that your family can rely on. Our team is ready to provide the clarity you need to move forward with confidence.

Securing Your Legacy Through Disciplined Financial Oversight

Achieving a state of financial readiness requires more than a standard policy; it demands a curated approach to risk management that respects your current economic landscape. By utilizing simplified issue methodologies, you can bypass the friction of medical examinations while securing immediate coverage options. This strategic alignment ensures that burial insurance for low income seniors remains an accessible tool for legacy preservation rather than an administrative burden. Since 2009, The Paul Group has applied disciplined expertise to the Florida and Illinois senior communities, focusing on the intersection of personal dignity and structural integrity. Our methodology prioritizes bespoke solutions that adapt to your specific needs, ensuring your final arrangements are handled with the intellectual rigor they deserve. Don’t leave your family’s future to chance when a structured framework is available today.

Request your bespoke final expense strategic briefing from The Paul Group today.

Your commitment to a well-ordered future starts with a single, decisive step toward lasting protection.

Frequently Asked Questions

Is burial insurance for low income seniors actually affordable on Social Security?

Yes, it’s designed for fixed budgets. According to the Social Security Administration’s 2024 data, the average monthly benefit is $1,907, and approximately 45% of retirees allocate roughly 3% to 5% of this for protection. Burial insurance for low income seniors remains a viable strategic tool because premiums are locked in at the time of purchase. This prevents inflation from eroding your financial stability as you age in Florida or Illinois.

Can I get burial insurance in Florida, Illinois if I have a pre-existing condition?

You can secure coverage regardless of your medical history through guaranteed issue policies. In states like Illinois and Florida, carriers offer simplified issue or guaranteed acceptance products that bypass traditional medical exams. While 100% of applicants are typically accepted for guaranteed plans, those with managed conditions like Type 2 diabetes often qualify for immediate coverage. This ensures your health status doesn’t derail your long-term legacy planning or organizational goals.

How much does the average burial insurance policy cost per month in 2026?

While individual rates vary based on age and gender, the National Funeral Directors Association 2023 report indicates that the median cost of a funeral is approximately $8,300. To cover this, approximately 70% of policyholders find monthly rates ranging from $50 to $120. We focus on optimizing these costs by aligning your policy limit with actual regional expenses in Florida or Illinois. This precision prevents you from overpaying for unnecessary coverage.

What happens if I outlive my burial insurance policy term?

You won’t outlive these policies because they’re structured as whole life insurance, which remains active until age 121. Unlike term insurance that expires after 10 or 20 years, burial insurance for low income seniors provides permanent security. As long as you maintain premium payments, the contract stays in force. This structural integrity is a core component of a disciplined financial strategy, ensuring the death benefit is available when it’s required by your family.

Is there a waiting period before the full death benefit is available?

Approximately 90% of guaranteed issue policies involve a 24 month graded benefit period where full payouts are restricted. If death occurs from natural causes during these first 730 days, beneficiaries usually receive all paid premiums plus 10% interest. However, immediate coverage is available for those who qualify through medical underwriting. We help you navigate these timelines to ensure your transition into a fully protected state is both swift and strategically sound.

How do my beneficiaries in Florida, Illinois actually claim the money?

Beneficiaries initiate the claim by submitting a certified death certificate and a completed claim form directly to the insurer. In Florida and Illinois, state statutes require insurers to process undisputed life insurance claims within 30 to 60 days of receipt. The Paul Group recommends keeping a digital copy of the policy in a secure location. This proactive step accelerates the capital transfer, allowing families to manage funeral costs without delay.

What is the difference between burial insurance and a pre-paid funeral plan?

Burial insurance provides a cash benefit to your beneficiaries, whereas pre-paid plans are contracts with specific funeral homes. According to the 1984 Federal Trade Commission’s Funeral Rule, consumers have the right to choose only the goods and services they want. Burial insurance offers superior flexibility, as the funds can be used at any facility or for any final expense. This bespoke approach ensures your family retains control over the ceremony and costs.

Leave a Reply