Funeral and Burial Expenses Are Rising — Here’s How to Protect Your Family

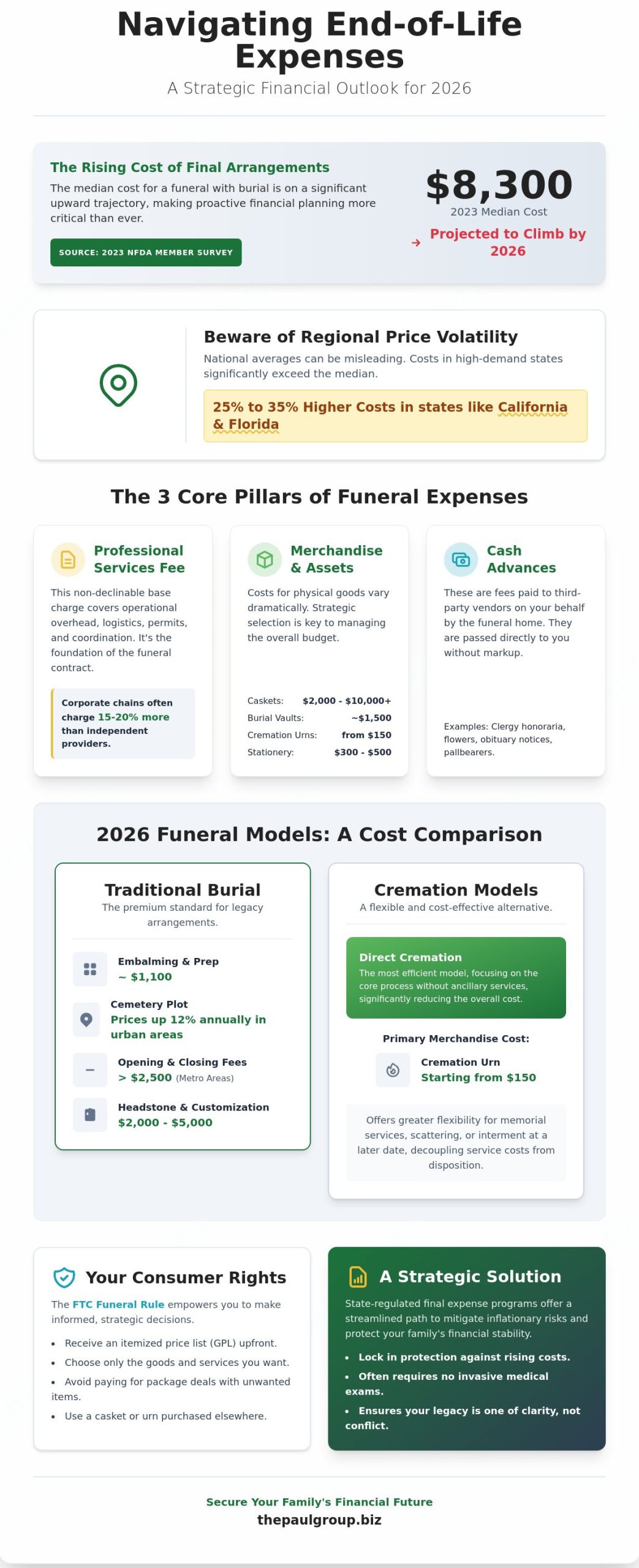

According to the 2023 NFDA Member Compensation and Operating Survey, the median cost of a funeral with viewing and burial has surged to $8,300, a figure projected to climb significantly by 2026 as labor and material costs continue their upward trajectory. You likely recognize that managing funeral and burial expenses is no longer just an emotional transition; it’s a complex financial event that requires the same level of optimization as any other major investment. The confusion surrounding itemized versus package pricing often creates unnecessary friction, yet you don’t have to leave your family’s stability to chance.

This guide will empower you to master the complexities of these costs with a sophisticated breakdown of 2026 projections and state-regulated solutions designed to mitigate inflationary risks. We’ll examine the shift toward transparent cost structures, explore curated state programs, and establish a methodology for a sustainable funding strategy. By aligning your end-of-life arrangements with a disciplined financial framework, you can transform a period of potential conflict into a legacy of clarity and structural integrity. Our collective expertise ensures that your most complex organizational challenges are both understood and solvable through strategic intervention.

Key Takeaways

-

Gain a clear understanding of the three core pillars of end-of-life costs to navigate regional price volatility effectively across states like California and Florida.

-

Analyze the fiscal implications of traditional interment versus cremation models to optimize your budget for funeral and burial expenses in 2026.

-

Leverage your rights under the FTC Funeral Rule to ensure you only invest in the specific goods and services that align with your strategic vision.

-

Discover how state-regulated final expense programs offer a streamlined path to senior protection without the necessity of invasive medical examinations.

-

Implement a disciplined financial strategy that begins with a holistic audit of your resources to secure long-term stability and structural integrity for your estate.

Table of Contents

-

Understanding the Architecture of Funeral and Burial Expenses

-

State Regulated Life Insurance Programs in California and Beyond

Understanding the Architecture of Funeral and Burial Expenses

Effective end-of-life planning requires a shift from emotional reaction to strategic management. In 2026, the landscape of funeral and burial expenses is defined by three distinct structural pillars: professional service fees, merchandise costs, and third-party cash advances. While the National Funeral Directors Association (NFDA) reported a median cost of $8,300 for a funeral with burial in 2023, these national figures often obscure the reality of regional price volatility. In high-demand markets like California and Florida, families often encounter costs 25% to 35% higher than the national mean. This financial delta creates a significant risk for those relying on outdated or overly generalized estimates.

Unexpected debt adds a layer of cognitive load to the grieving process, often leading to decision fatigue and suboptimal financial choices. We view this planning not as a morbid necessity, but as a strategic alignment of one’s personal legacy with contemporary financial reality. It’s about ensuring that a family’s final tribute doesn’t compromise their long-term economic stability. For many, securing a policy for the best final expense insurance for seniors is a primary method for mitigating these volatile costs and ensuring a seamless transfer of responsibility.

The Basic Services Fee: The Industry Foundation

The cornerstone of any funeral contract is the non-declinable basic services fee. This charge represents the funeral home’s operational overhead and the professional expertise required to manage complex logistics. It covers the essential coordination of death certificates, the drafting of notices, and the securing of necessary permits. Under the FTC’s Funeral Rule, providers must disclose this fee upfront to ensure transparency. You’ll find that corporate-owned chains often have higher fixed overhead, resulting in fees that can be 15% to 20% higher than those of boutique, independent providers who offer more curated, bespoke services.

Merchandise and Physical Assets

Selecting physical assets requires a disciplined approach to value and utility. In the 2026 market, the price gap between traditional metal caskets and high-end wooden models remains substantial, often ranging from $2,000 to over $10,000. For those choosing cremation, urn costs provide a more flexible entry point, typically starting at $150. Beyond the primary vessel, cemeteries often mandate outer burial containers or vaults to prevent soil subsidence, adding another $1,500 to the total. Strategic planners must also account for silent costs like memorial stationery and guest books, which can add $300 to $500 to the final invoice if they aren’t included in a holistic service package.

A Comparative Analysis of 2026 Funeral Models

The funeral industry in 2026 reflects a broader cultural shift toward personalization and fiscal responsibility. Families now approach funeral and burial expenses as strategic investments in legacy rather than static obligations. This evolution requires a granular understanding of the various service models available today. Traditional burials remain the premium standard, requiring sophisticated coordination of logistics and multi-day facilities. To ensure your planning remains aligned with current market rates, utilizing a funeral costs and pricing checklist from the Federal Trade Commission provides a necessary baseline for vendor comparisons.

Traditional Burial Cost Breakdown

Embalming and professional body preparation costs have stabilized near an average of $1,100 in 2026, though high-end providers charge significantly more for restorative artistry. Cemetery expenses represent the most volatile variable. Urban plot prices in 2024 increased by 12% annually; this makes early acquisition a critical financial maneuver. Opening and closing fees now frequently exceed $2,500 in major metropolitan areas, while headstone customization adds another $2,000 to $5,000 to the final ledger. Transportation logistics, including hearse and limousine services, require meticulous scheduling to avoid overtime surcharges that can inflate a bill by 15% within a single afternoon.

Cremation and Alternative Methodologies

Direct cremation has emerged as the efficiency-driven leader, particularly in high-growth corridors like Texas and Arizona. In these states, the adoption rate for cremation surpassed 65% in 2025 as families prioritized flexibility over tradition. Alkaline hydrolysis, often called water cremation, is now legal in over 30 states. It offers a sustainable alternative with a price point typically 20% higher than flame-based cremation but significantly lower than traditional burial. Strategic cost-saving occurs when families separate the disposition of remains from the memorial event. Holding a "Celebration of Life" at a private residence or public park eliminates the high facility rental fees associated with traditional funeral homes, which often range from $500 to $1,500 per hour.

Green burials are no longer a niche preference. They represent a holistic commitment to environmental stewardship. By removing the need for concrete vaults and chemical embalming, this model reduces the long-term ecological footprint. It also simplifies the funeral and burial expenses by focusing on biodegradable materials and natural land conservation. For those evaluating the long-term impact of these choices, reviewing the best final expense insurance for seniors can provide the necessary liquidity to secure these bespoke arrangements. This transition from rigid tradition to curated experience allows for a more meaningful, and often more affordable, final tribute.

Consumer Rights and the FTC Funeral Rule

The Federal Trade Commission (FTC) Funeral Rule has regulated the industry since 1984, establishing a baseline for fiscal transparency. It mandates that providers present a General Price List (GPL) at the very start of any discussion. This document is your primary tool for strategic oversight. You have the legal right to select only the specific goods and services you desire rather than being forced into bundled packages. This itemization prevents the inflation of funeral and burial expenses by allowing you to decline non-essential components that don’t align with your vision.

Federal law prohibits funeral homes from charging a "casket handling fee" if you purchase a container from a third-party vendor. This allows for significant cost optimization through external sourcing. To ensure full compliance, utilize the FTC’s official checklist to audit every quote against the provider’s stated GPL. This disciplined approach ensures that your final statement reflects your choices rather than a provider’s sales targets.

Transparency in Pricing

Strategic planning requires viewing the Casket Price List (CPL) before you enter a showroom. This prevents the psychological pressure of viewing high-end inventory before you understand the baseline costs. You must also scrutinize "Cash Advance Items" on your final statement. These are third-party charges for services like obituary notices, clergy honoraria, or flowers. In competitive markets like Los Angeles or Miami, pricing for identical services often varies by 35% or more between providers. Comparing multiple quotes is a necessary step in professional financial management. Managing funeral and burial expenses requires a blend of legal knowledge and rigorous market research to ensure the highest value.

State-Specific Protections in California and Texas

Regional regulations offer additional layers of security for your estate. The California Department of Consumer Affairs provides strict guidelines on how arrangements are finalized and how survivors are treated. For those evaluating funding mechanisms, the California Department of Insurance defines the parameters of funeral and burial insurance to protect residents from predatory practices. This oversight ensures that the policies you purchase meet the state’s rigorous solvency and consumer protection standards.

In Texas, the Texas Funeral Service Commission oversees licensing and resolves consumer disputes with a focus on administrative accountability. Both states have rigorous standards for "Pre-need" contracts. These regulations ensure that funds paid in advance are held in trust or backed by insurance products. Understanding these regional nuances is vital when considering the best final expense insurance for seniors pros and cons 2026. This level of diligence transforms a difficult process into a well-managed transition that respects both the individual and the estate’s long-term stability.

State Regulated Life Insurance Programs in California and Beyond

State-regulated programs provide a critical layer of consumer protection for those managing funeral and burial expenses. In California, these programs operate under strict Department of Insurance oversight to ensure solvency and reliable claim payouts. Simplified issue life insurance removes the friction of invasive medical exams; it utilizes digital health records and prescription databases for rapid, high-integrity underwriting. This efficiency is a cornerstone of a modern estate plan. Fixed premium structures serve as a primary defense against the 2026 inflationary environment. When you lock in a rate today, you’re effectively decoupling your final costs from the rising consumer price index. These programs aren’t just insurance; they’re strategic tools designed to neutralize burial liabilities with surgical precision.

Qualifications for Senior Final Expense Plans

Eligibility for these programs is remarkably inclusive, yet it requires a nuanced understanding of carrier appetite. Most California plans target residents between ages 50 and 85, focusing on permanent protection rather than temporary coverage. Immediate coverage offers the full death benefit from the policy’s effective date, which is the preferred outcome for our clients. Graded benefits provide a tiered payout over the initial 24 months, typically reserved for those with complex medical histories or chronic conditions. It’s about finding the right fit for your specific health profile. Learn more about the best final expense insurance for seniors to see which structure aligns with your goals.

The Paul Group Methodology

Our firm doesn’t believe in one-size-fits-all solutions. We employ a curated approach to match seniors with top-tier insurance carriers, selecting from a portfolio of 15+ highly rated providers. Our reach extends across 15+ states including Texas, Arizona, and Florida, allowing us to facilitate a seamless application process regardless of your primary residence. We align human leadership with operational systems to ensure your application moves from submission to approval with zero friction. Our commitment is to provide clear, authoritative guidance that simplifies complex financial decisions. We prioritize long-term stability over quick fixes, ensuring your funeral and burial expenses are fully accounted for long before they’re needed.

Secure your family’s future and eliminate financial uncertainty by scheduling a strategic financial consultation with our expert team today.

Implementing Your End-of-Life Financial Strategy

Strategic financial planning requires a transition from theoretical knowledge to disciplined execution. To protect your family’s stability, you must follow a methodical four-step framework. First, conduct a holistic audit of your current liquid assets and dedicated savings. This clarity allows you to identify where your current resources end and where external funding must begin. Second, define your service model; choosing between traditional burial or cremation dictates the baseline of your funeral and burial expenses. Third, secure a final expense policy to eliminate the funding gap. Finally, communicate the structural details of this strategy to your beneficiaries to ensure seamless implementation when the time arrives. Clarity is the foundation of legacy.

-

Step 1: Audit your current portfolio for liquidity.

-

Step 2: Select a service model to establish a cost baseline.

-

Step 3: Bridge the deficit with a dedicated final expense policy.

-

Step 4: Formalize the communication of these plans to your heirs.

Funding the Gap

Relying on the Social Security Administration’s one-time death payment of $255 is a mathematically flawed strategy. This figure has remained stagnant since 1954, while the average cost of a funeral with burial reached $8,300 in 2023. Families without a dedicated plan often resort to high-interest credit cards, which carried average APRs exceeding 22% in 2024. This creates a cycle of debt during a period of grief. A curated final expense policy solves this by ensuring liquidity. These funds are typically disbursed within 24 to 48 hours of a claim, providing the immediate capital necessary to manage funeral and burial expenses without fiscal strain.

Finalizing the Plan with The Paul Group

The Paul Group approaches end-of-life planning with the same rigor applied to corporate optimization. We offer access to an independent broker network to compare the market, ensuring your strategy is cost-effective and resilient. Our methodology focuses on a bespoke quote tailored to your specific regional cost profile and personal legacy goals. We don’t provide off-the-shelf products; we engineer solutions that prioritize structural integrity and family protection. By closing the loop on your financial legacy today, you ensure that your family’s future remains governed by your vision, not by market volatility or emergency debt. It’s about securing a future that is both stable and dignified.

Mastering the Architecture of Your Financial Legacy

Strategic foresight in 2026 demands a shift from reactive spending to a methodology of proactive optimization. You’ve navigated the structural complexities of the modern funeral industry, identifying how the FTC Funeral Rule and state-specific programs in California provide a framework for consumer protection. Managing funeral and burial expenses isn’t a solitary task; it’s a sophisticated alignment of resources designed to protect your family’s long-term stability. Clarity is the ultimate result of professional intervention.

Since 2009, The Paul Group has operated as a seasoned strategic partner for seniors across 15+ states. We don’t offer off-the-shelf products. Instead, our independent brokerage delivers curated insurance solutions tailored to the specific needs of your estate. Our model prioritizes certainty through fixed rates and a streamlined process that requires no medical exams. This disciplined approach transforms a period of potential chaos into one of quiet confidence and structural integrity. You’ve done the work to understand the landscape; now it’s time to implement a solution that reflects your commitment to excellence.

Secure your family’s future with a bespoke Final Expense Quote from The Paul Group

Taking this step ensures your legacy remains as organized and impactful as the life you’ve built.

Frequently Asked Questions

How much does a traditional funeral cost in 2026?

A traditional funeral with viewing and burial costs approximately $9,135 according to 2023 NFDA data adjusted for 3% annual inflation. Strategic planning requires accounting for these escalating funeral and burial expenses to ensure long term financial stability. By 2026, families should anticipate costs exceeding $10,000 when including vault requirements and cemetery fees. This proactive adjustment allows for a more resilient and prepared estate strategy.

What is the difference between funeral insurance and burial insurance?

Funeral insurance typically refers to a pre-need contract with a specific provider; burial insurance is a simplified issue whole life policy. The Paul Group views these as distinct strategic tools for legacy preservation. Burial insurance offers a cash benefit to beneficiaries, whereas funeral insurance locks in specific services at current rates to mitigate future price volatility. We recommend a bespoke analysis to determine which vehicle aligns with your family goals.

Can I get life insurance for funeral expenses without a medical exam?

Guaranteed issue life insurance provides coverage without a medical exam or health inquiries. These policies cater to individuals between ages 50 and 85 who require immediate financial alignment for end of life costs. While premiums are higher, the simplified underwriting process ensures that 100% of applicants who meet age requirements can secure necessary funding for funeral and burial expenses. It’s a reliable methodology for those with complex health histories.

What happens if I cannot afford funeral and burial expenses?

Local county coroners or indigent burial programs provide basic services when a family lacks the financial resources to pay. In 2024, many municipal programs transitioned to direct cremation as the primary method for these cases. Families may also apply for FEMA assistance if the death was related to a declared disaster. This program covered up to $9,000 per funeral in recent cycles, providing a critical safety net during crises.

Is the Social Security death benefit enough to cover a cremation?

The Social Security one-time death benefit remains fixed at $255; this is insufficient to cover even the most basic direct cremation. Since the average cost of a direct cremation in the United States surpassed $2,100 in 2023, this federal payment covers less than 12% of the total liability. Relying on this benefit alone creates a strategic deficit. It requires additional private insurance or personal savings to achieve full fiscal coverage.

How do state-regulated life insurance programs work in California?

California state-regulated programs operate as private insurance products that must comply with strict Department of Insurance consumer protection standards. These plans utilize a methodology focused on price transparency and non-forfeiture values. The Paul Group analyzes these programs to ensure clients receive a curated selection of policies that meet the specific legal mandates of the California Insurance Code. This structural integrity is vital for long term estate stability.

Can I use a life insurance policy to pay a funeral home directly?

You can utilize a life insurance assignment to direct a portion of the death benefit straight to the service provider. This optimization of the claims process allows the funeral home to verify coverage and begin arrangements without waiting for a full probate settlement. Most providers charge a small processing fee, often around 3% to 5% of the assigned amount. This facilitates a seamless administrative transfer during a sensitive transition period.

What are the most common hidden costs in funeral planning?

Hidden costs frequently manifest as cemetery opening and closing fees; these can add $1,500 to $3,000 to the total invoice. Other overlooked line items include obituary placements in major newspapers, which often cost $200 to $500 per day. A holistic approach to financial planning identifies these logistical variables early. We prioritize this level of detail to prevent unexpected budgetary strain during the implementation of your final wishes.

Leave a Reply