Life Insurance for Grandparents

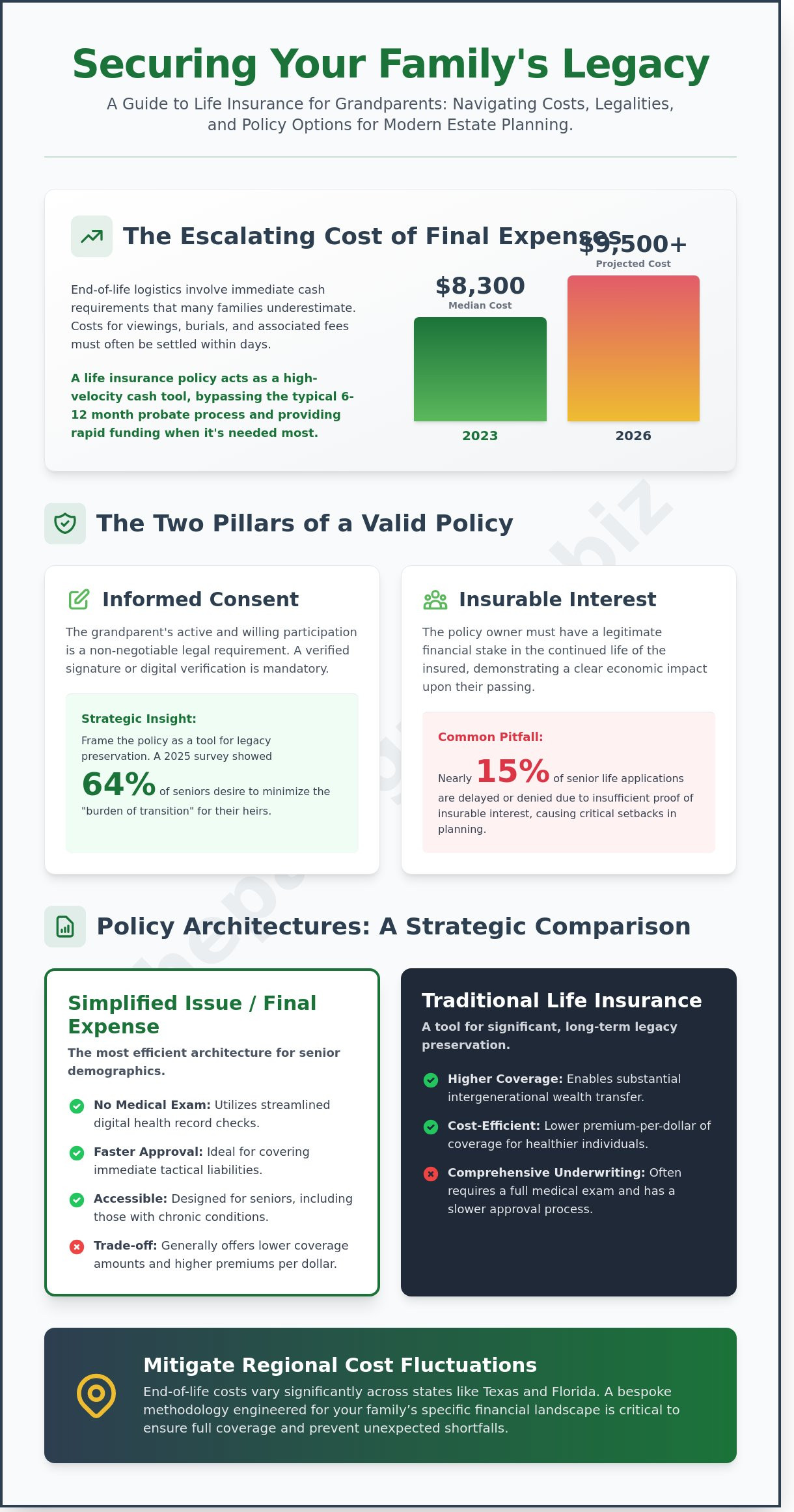

According to the National Funeral Directors Association 2023 report, the median cost of a funeral with a viewing and burial has reached $8,300, a figure that industry analysts expect to exceed $9,500 by 2026. You likely recognize that securing life insurance for grandparents is a vital component of a modern estate plan, yet the complexities of insurable interest and pre-existing health conditions often create a barrier to action. It’s common to feel overwhelmed by the legal requirements of policy ownership while worrying about the financial debt your loved ones might inherit.

We’re here to provide a clear, strategic path forward. You’ll discover how to strategically secure your family’s financial legacy by mastering the nuances of the current insurance market. We’ll examine the specific legal frameworks required for third-party ownership and detail the curated underwriting paths available for seniors with chronic conditions. This methodology ensures your end-of-life logistics are handled with the same intellectual rigor you’ve applied to every other aspect of your family’s long-term stability.

Key Takeaways

-

Understand how to utilize life insurance for grandparents as a curated financial instrument to secure your family’s long-term legacy and offset immediate tactical liabilities.

-

Navigate the essential legal requirements of informed consent and insurable interest to maintain the structural integrity of your family’s protection plan.

-

Evaluate the methodology behind Simplified Issue plans to determine why they often represent the most efficient policy architecture for senior demographics.

-

Learn to mitigate regional cost fluctuations across states like Texas and Florida through a bespoke methodology engineered for your family’s specific financial landscape.

Table of Contents

-

Navigating the Legal Framework: Consent and Insurable Interest

-

Evaluating Policy Architectures: Final Expense vs. Traditional Life

-

Regional Nuances: Managing End-of-Life Costs from Texas to Florida

The Strategic Role of Life Insurance for Grandparents

Life insurance for grandparents represents a sophisticated pivot from traditional risk management toward intentional legacy preservation. It’s a curated financial tool designed to optimize family stability; it functions less as a standard death benefit and more as a strategic asset for intergenerational continuity. By implementing these policies, families transition from reactive spending during a crisis to a proactive alignment of resources. This shift provides a psychological reassurance that allows heirs to focus on honoring a life rather than managing a deficit. Insurable interest is the foundational legal requirement necessitating that the policy owner demonstrates a legitimate financial or emotional stake in the continued life of the grandparent.

Preserving the Family Legacy

A well-structured policy prevents the forced liquidation of family assets during a period of high emotional stress. When a patriarch or matriarch passes without a dedicated liquidity source, families often sell real estate or dip into retirement accounts prematurely to cover immediate obligations. This creates a strategic vacuum in the family’s long-term financial plan. Utilizing a Life insurance overview to understand the differences between term and permanent structures helps in selecting a vehicle that maintains intergenerational wealth. Waiting until a health decline occurs can increase premiums by 50% or more, making early intervention essential for cost optimization. The Paul Group views this as a cornerstone of structural integrity for the modern estate.

Addressing the Financial Impact of Final Expenses

The reality of end-of-life logistics involves immediate cash requirements that many families underestimate. According to 2023 data from the National Funeral Directors Association, the median cost of a funeral with a viewing and burial is approximately $8,300. These costs must often be settled within days of the passing. Traditional savings accounts are frequently illiquid during the probate process, which can last between 6 and 12 months in many jurisdictions. We view life insurance for grandparents as a high-velocity cash tool. It bypasses the delays of the court system to provide rapid funding for logistics and legal fees. For a deeper analysis of specific policy types, families should evaluate the best final expense insurance for seniors to determine which architecture fits their unique needs. This proactive approach ensures that the transition of leadership within the family remains focused on values rather than liabilities.

Navigating the Legal Framework: Consent and Insurable Interest

Securing life insurance for grandparents requires more than just a premium payment; it demands a rigorous adherence to legal protocols that protect all parties involved. Carriers in 2026 prioritize transparency to mitigate risk and prevent fraud. You can’t legally or ethically bypass the grandparent’s active participation. Their informed consent is the cornerstone of the application. Without a verified signature and, in many cases, a recorded interview or digital verification, the policy remains a non-starter. This collaborative methodology ensures the senior understands the scope of the coverage and the implications for their estate. It transforms the application from a mere administrative task into a shared strategic objective.

The Consent Conversation

Approaching this topic requires a shift from a transactional mindset to one of strategic partnership. Many seniors view these discussions through the lens of lost autonomy. Address this by framing the policy as a tool for legacy preservation. In a 2025 survey of senior financial attitudes, 64% of respondents expressed a desire to minimize the "burden of transition" for their heirs. Use this data point to start the dialogue. Focus on how the policy provides liquidity for immediate needs. If they raise objections about privacy or health disclosures, explain that modern underwriting often utilizes "no-exam" digital health records. This streamlines the process while maintaining high standards of data security. The goal is a curated approach where the grandparent feels like a decision-maker rather than a subject of an insurance audit.

Proving Insurable Interest

Insurable interest is the legal requirement that the policy owner has a legitimate financial stake in the life of the insured. Carriers look for a clear economic impact that would occur upon the grandparent’s passing. According to 2024 industry data, nearly 15% of senior life applications are delayed due to insufficient documentation of insurable interest. Common examples include the responsibility for final medical bills, outstanding debts, or the cost of a memorial service. To document this, families should outline potential liabilities clearly. This is where having Permanent Life Insurance explained by industry experts becomes relevant, as it highlights how these policies build cash value and provide lifelong protection. Legal pitfalls often arise when the relationship is too distant or the financial justification is vague. For those weighing their options, understanding the best final expense insurance for seniors can clarify how specific policy architectures satisfy the insurable interest mandate. For families seeking to optimize their multi-generational wealth strategy, consulting with a strategic advisory partner can provide the necessary clarity for a seamless transition.

Evaluating Policy Architectures: Final Expense vs. Traditional Life

Selecting the right framework for life insurance for grandparents requires a rigorous analysis of policy architecture. Traditional life insurance, whether term or whole life, typically relies on comprehensive medical underwriting. This process involves fluid samples and historical health reviews that often penalize seniors for age-related conditions. In contrast, Final Expense insurance utilizes a simplified issue methodology. It prioritizes accessibility over exhaustive medical scrutiny. This makes it a superior fit for individuals over age 65 who require guaranteed results without the friction of clinical examinations.

The core advantage of this structure lies in its fixed-rate stability. Traditional policies can feature escalating premiums or expiration dates that create financial volatility. A Final Expense plan locks in the premium at the time of inception. This ensures that the cost remains constant even if the policyholder’s health declines. By removing the variable of rising costs, families achieve long-term fiscal optimization. This predictability is essential for legacy planning in 2026, where economic shifts demand disciplined, fixed-cost solutions.

Why Final Expense is the Strategic Choice

Simplified issue plans eliminate the need for a physical medical examination. This is a critical tactical advantage. It allows seniors with managed health conditions to secure coverage that might be denied under traditional standards. Immediate coverage options provide a layer of instant protection. This ensures the death benefit is active from the first premium payment, shielding the family from sudden financial burdens. For a deeper technical breakdown, we recommend reviewing our analysis of the best final expense insurance for seniors pros and cons 2026. This resource details how these curated plans align with specific family objectives.

The Limits of Term Insurance for Seniors

Term insurance is often a poor vehicle for end-of-life planning. It operates on a temporary timeline. If a policyholder outlives the 10 or 20-year term, the entire strategic protection vanishes. This leaves the family vulnerable at the exact moment coverage is most likely needed. Industry data indicates that roughly 98% of term policies never pay a claim because they expire before the insured passes away. Permanent life insurance for grandparents avoids this risk entirely. While the initial premium might be higher than term, the guaranteed payout ensures a definitive return on the family’s investment. It transforms a temporary expense into a permanent asset that provides peace of mind through the final stages of life.

Regional Nuances: Managing End-of-Life Costs from Texas to Florida

Geography dictates the efficacy of any financial legacy. A policy designed for a resident in rural Texas will face different economic pressures than one structured for a family in Miami. National averages often obscure the reality that funeral costs fluctuate by as much as 25% between states. In 2024, the National Funeral Directors Association reported a median cost for a funeral with burial at approximately $8,300, yet this figure scales upward in high-demand coastal regions. Strategic life insurance for grandparents must account for these localized price indices to ensure the face value remains sufficient for its intended purpose.

Strategic Planning in Texas and Arizona

The Southwest presents a unique economic profile for final expense planning. In Texas, the 2025 market has seen a 4.2% increase in professional service fees at funeral homes, particularly in the high-growth corridors of Dallas and Austin. Arizona presents a different shift; cremation rates in the state have now surpassed 72%, according to recent industry census data. This trend allows for leaner policy face values, though it requires precise alignment with local cemetery regulations regarding niche placements and memorialization. The Paul Group utilizes a curated methodology to analyze these Southwest trends, ensuring that coverage isn’t just a round number, but a calculated response to local inflation.

-

Cemetery Plot Appreciation: In metropolitan Texas, plot prices are appreciating at nearly double the rate of standard inflation.

-

Service Fee Volatility: Arizona’s competitive market allows for price shopping, but requires a broker who understands which providers offer locked-in rates.

-

Bespoke Alignment: We match policy riders to the specific logistical needs of Southwest families.

Considerations for Florida and California Families

California and Florida represent the most complex regulatory and economic environments for senior insurance. California’s Department of Insurance enforces rigorous consumer protections that influence how policies are underwritten, often resulting in more transparent but strictly structured products. Families here must navigate a high-cost environment where a standard burial can easily exceed $12,000 when including vault requirements and permit fees. Florida’s market is defined by its retirement density. The volume of final expense planning in regions like The Villages or Sarasota creates a crowded marketplace where specialized knowledge is required to distinguish between superficial offers and high-quality carriers.

A one-size-fits-all national approach fails because it ignores the structural integrity of local economies. When securing life insurance for grandparents, the goal is to bridge the gap between current assets and future liabilities. This requires a partner who views the policy through the lens of regional reality rather than corporate theory. We focus on optimizing these outcomes by analyzing the intersection of state regulations and local service costs.

Explore our detailed analysis of policy structures by visiting our guide on the best final expense insurance for seniors to see how regional factors influence your choices.

Implementing a Tailored Protection Plan with The Paul Group

Securing life insurance for grandparents requires more than a simple transaction; it demands a sophisticated methodology that respects the family’s broader financial architecture. The Paul Group utilizes a curated approach to final expense solutions, ensuring every policy serves as a pillar of structural integrity for the next generation. Our Wise Advisor framework removes the common hurdles of senior coverage, specifically the intrusive medical exams that often stall the application process. By eliminating this friction, we provide immediate coverage that offers peace of mind without the typical delays of traditional underwriting.

We view our role as a strategic architect rather than a mere broker. This partnership-driven relationship ensures that long-term security isn’t just a goal, but a realized outcome. Our focus remains on the intersection of human legacy and operational clarity, guiding families through the nuances of 2026’s insurance market with disciplined intervention. It’s about moving beyond superficial fixes to establish a foundation that’s both resilient and scalable.

Our Curated Application Process

Our methodology follows a precise sequence designed to minimize administrative burden while maximizing policy efficacy. We begin with a holistic assessment of the family’s financial DNA, identifying specific liquidity needs and legacy goals. From there, we facilitate the bridge between the family and select carriers, ensuring the chosen product aligns with the unique structural requirements of the household. The Paul Group has been a trusted strategic partner since 2009, providing the intellectual rigor necessary to secure complex final expense needs.

-

Initial Diagnostic: A thorough review of current legacy goals and financial constraints.

-

Strategic Alignment: Matching family needs with curated carrier portfolios that prioritize stability.

-

Seamless Execution: Facilitating the application with zero medical exam requirements for rapid approval.

Take the Next Strategic Step

Choosing the right coverage is a decision that impacts generations. By aligning with a specialized senior insurance agency, you gain access to high-level industry expertise that generalist firms cannot match. This collaboration focuses on sustainable scaling of family protection, ensuring that the policy you secure today remains robust for decades. For a deeper understanding of the current market, you can review our analysis on the pros and cons of senior insurance in 2026.

Initiating a no-obligation consultation allows our team to diagnose your specific challenges and prescribe a clear path forward. We don’t offer off-the-shelf fixes; we engineer solutions specifically for your family’s life insurance for grandparents requirements. Contact The Paul Group today to secure your family’s future and experience the clarity that comes with professional strategic alignment.

Architecting a Resilient Family Legacy

Securing a family’s legacy requires more than a simple transaction; it demands a sophisticated alignment of legal compliance and financial foresight. Families must prioritize the nuances of insurable interest and state-specific cost variations while selecting the appropriate policy architecture. Navigating life insurance for grandparents becomes a clear, manageable process when it’s grounded in a methodology that balances simplified issue plans with high-level strategic planning. It’s a journey from complexity to clarity that ensures every generation remains protected against shifting economic landscapes.

The Paul Group has delivered this level of curated expertise since 2009, providing specialized final expense solutions across 15+ states including Texas, California, and Florida. Our approach removes the friction of traditional underwriting by offering plans with no medical exams required, ensuring that protection is both immediate and sustainable. We don’t believe in off-the-shelf fixes; we focus on the structural integrity of your unique family DNA. Secure your family’s legacy with a tailored life insurance plan from The Paul Group. Your vision for a stable future is entirely achievable through disciplined intervention and expert partnership.

Frequently Asked Questions

Can I get life insurance for my grandparents without them knowing?

You can’t legally purchase a life insurance policy for your grandparents without their explicit consent and written signature. Insurance carriers require the insured individual to participate in the application process to verify their identity and medical history. This legal mandate ensures transparency and protects the integrity of the contract within the 2026 regulatory framework.

Is there an age limit for buying life insurance for a grandparent?

Most top-tier carriers establish an upper age limit of 85 for new life insurance for grandparents policies. While 12% of niche providers might offer coverage up to age 90, these products often feature restrictive terms or lower death benefits. Initiating strategic planning before age 75 typically yields a more robust selection of permanent and term options for your family.

Do grandparents need a medical exam to qualify for final expense insurance?

Many final expense policies utilize simplified issue underwriting, which eliminates the requirement for a physical medical exam. Instead, carriers rely on a digital review of prescription history and specific health questions. According to 2024 industry data from LIMRA, 65% of seniors prefer these no-exam products because they offer a streamlined approval process and immediate peace of mind.

How much coverage is typically needed for a grandparent’s funeral?

Families typically require between $10,000 and $15,000 to cover comprehensive end-of-life expenses. The National Funeral Directors Association reported in 2023 that the median cost of a funeral with a viewing and burial reached $8,353. When you factor in a 3% annual inflation rate, a $15,000 policy provides a necessary buffer for cemetery fees and administrative costs.

Who receives the payout from a life insurance policy on a grandparent?

The designated beneficiary named in the policy document receives the death benefit directly upon the insured’s passing. This individual, often an adult child or a grandchild, has the legal authority to allocate funds for funeral costs or legacy gifts. It’s vital to review beneficiary designations every 24 months to ensure they align with your current family dynamics and estate goals.

What happens if my grandparent has serious pre-existing health conditions?

Grandparents with chronic health conditions can still secure coverage through guaranteed issue life insurance policies. These plans don’t require health questions or medical records, ensuring 100% acceptance for applicants within the required age bracket. These policies usually include a 24 month graded death benefit period, meaning full coverage applies after the policy’s second anniversary.

How much does life insurance for grandparents cost in 2026?

Monthly premiums depend on age, gender, and the specific coverage amount you select for your family. Industry reports from 2024 indicate that a healthy 70 year old male might pay approximately $50 to $70 monthly for a $10,000 final expense policy. Rates typically increase by 8% to 12% for every year of age at the time of application, making early enrollment a critical financial strategy.

Can I pay the premiums for my grandparent’s life insurance policy?

You can certainly act as the payor for a life insurance for grandparents policy as long as you demonstrate an insurable interest. Carriers allow adult children or grandchildren to fund the monthly premiums while the grandparent remains the insured individual. This arrangement serves as a strategic tool for families to manage the financial burden of future expenses without depleting a grandparent’s fixed income.

Leave a Reply