Funeral Expense Insurance for Seniors

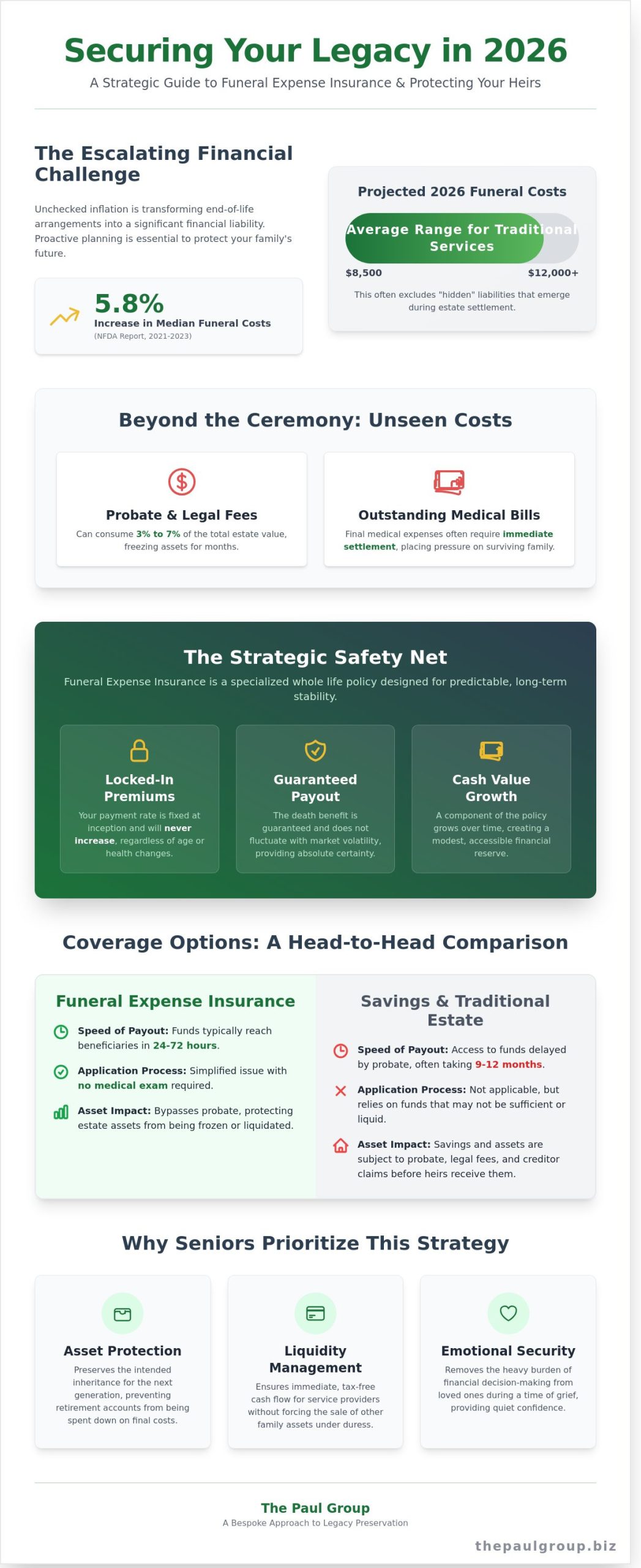

The National Funeral Directors Association reported a 5.8% increase in median funeral costs between 2021 and 2023, a data point that signals a complex fiscal challenge for families entering 2026. You likely recognize that unchecked inflation can transform a dignified farewell into a significant liability for your heirs. Most seniors share your desire to avoid becoming a financial burden; however, the choice between term and whole life structures often creates unnecessary friction. Our collective at The Paul Group views funeral expense insurance not merely as a policy, but as a critical component of a holistic legacy optimization strategy.

It’s time to move beyond the anxiety of rising costs and toward a position of quiet confidence. We’ll show you how to strategically secure your family’s financial future by mastering the nuances of end-of-life cost management. You’ll discover the methodology behind locking in fixed premium rates that never increase, ensuring long-term stability regardless of market shifts. This briefing details the path to immediate coverage and a simplified application process that requires no medical exam, providing a curated solution for your family’s unique DNA.

Key Takeaways

-

Analyze the macro-economic shifts of 2026 to insulate your household from the escalating costs of end-of-life services through proactive financial planning.

-

Discover how funeral expense insurance functions as a sophisticated safety net, utilizing fixed premiums and cash value accumulation to ensure permanent financial alignment.

-

Contrast simplified issue policies with traditional life insurance to identify the most efficient methodology for securing coverage without being priced out by age-related premiums.

-

Explore how regional regulatory environments and local trends in states like Texas and California necessitate a curated approach to legacy preservation.

-

Understand the value of a bespoke, agent-driven partnership that prioritizes long-term structural integrity over the cold, transactional experiences of mass-market providers.

Table of Contents

-

How Funeral Expense Insurance Functions as a Strategic Safety Net

-

Evaluating Coverage Options: Simplified Issue vs. Traditional Life Insurance

-

Regional Considerations: Planning Across the Western and Southern U.S.

-

Securing Your Legacy with The Paul Group: A Bespoke Approach

The Economic Reality of End-of-Life Costs in 2026

Funeral expense insurance serves as a specialized whole life policy, engineered specifically to mitigate the financial friction of final arrangements. It’s not merely a policy; it’s a structural safeguard for the modern estate. As we enter 2026, the macro-trend of funeral inflation has intensified, placing unprecedented pressure on household liquidity. Families often find themselves in a reactive posture, forced to liquidate assets under duress when planning is absent. The Paul Group advocates for a shift toward the Wise Advisor methodology, where families prioritize proactive architecture over last-minute crisis management. Understanding What is burial insurance? provides the foundational clarity needed to see these policies as tools for long-term organizational stability. Traditional savings accounts, while useful, frequently lack the speed and tax-efficiency required to address holistic end-of-life needs during the immediate window following a loss.

The Median Cost Breakdown: Beyond the Casket

In 2026, the average traditional funeral service in the U.S. ranges from $8,500 to $12,000 depending on regional variables. This figure encompasses professional service fees, viewing costs, and complex logistics like transportation. Beyond the visible ceremony, hidden liabilities often emerge. These include probate legal fees, which can consume 3% to 7% of an estate’s total value, and outstanding medical bills that require immediate settlement. A curated approach to funeral expense insurance ensures these variables are accounted for before they impact the surviving family’s financial health. Relying on liquid cash is often a strategic error, as those funds are frequently frozen during the initial stages of estate settlement.

Why Seniors are Prioritizing Strategic Alignment

Modern seniors are increasingly focused on protecting liquid assets for their heirs. They view spending down a retirement account on final costs as an operational failure. By utilizing immediate coverage options, policyholders achieve instant peace of mind and organizational clarity. This strategic alignment ensures that the legacy remains intact, while the funeral expense insurance provides the necessary capital for a dignified transition. It’s about transformation from a state of uncertainty to a position of disciplined control. For a deeper dive into the specific advantages and trade-offs of these plans, families should review our analysis of the best final expense insurance for seniors pros and cons 2026. Our collective expertise suggests that the most successful outcomes result from early intervention and a commitment to structural integrity.

-

Asset Protection: Preserving the intended inheritance for the next generation.

-

Liquidity Management: Ensuring immediate cash flow for service providers.

-

Emotional Security: Removing the burden of financial decision-making during grief.

How Funeral Expense Insurance Functions as a Strategic Safety Net

Strategic planning requires tools that offer absolute predictability. Our methodology at The Paul Group focuses on structural integrity, which is why funeral expense insurance operates on a whole life chassis. This structure ensures that premiums remain locked at the inception rate. It creates a fixed line item in a senior’s budget, shielding the family from the volatility of the 2026 financial environment. The death benefit is guaranteed. It doesn’t fluctuate with market cycles or interest rate shifts. Partnering with a Wise Advisor ensures that the carrier selected has the fiscal solvency to honor these long-term commitments, providing a bespoke fit for your family’s unique financial DNA.

Beyond the death benefit, these policies accumulate a cash value component. It serves as a secondary layer of financial integrity, providing a modest reserve that grows over time. Speed is the primary differentiator here. While traditional estates often languish in probate for 9 to 12 months, insurance proceeds typically reach beneficiaries within 24 to 72 hours of claim approval. This immediate liquidity is vital. It allows families to adhere to The Funeral Rule, which empowers consumers to choose only the services they want, provided they have the capital to settle accounts promptly. Selecting the right carrier requires a holistic view of the market. You might find it helpful to review our analysis of the best final expense insurance for seniors to see how different structures align with your goals.

The Power of Fixed Rates and Permanent Coverage

Locking in a policy today serves as a strategic hedge against the 3.5% average annual inflation rate seen in the death care industry. Rates will never increase. Your health might change, but the contract won’t. This permanent coverage offers a psychological dividend, removing the anxiety of a policy cancellation. It’s about structural stability. By securing 2026 rates, you’re essentially fixing your future costs at today’s prices, a move that reflects disciplined financial leadership.

Simplified Issue: The Methodology of No-Exam Qualification

Traditional underwriting is often a barrier for seniors. The Simplified Issue methodology replaces invasive physical exams with a curated series of health questions. It’s an optimized process. This approach is specifically engineered for those managing common health conditions like hypertension or type 2 diabetes. By reducing application friction, we ensure that the path to protection is both efficient and dignified. This methodology allows for a rapid turnaround, often securing coverage in a fraction of the time required by traditional term policies.

Evaluating Coverage Options: Simplified Issue vs. Traditional Life Insurance

Seniors often face a structural misalignment when utilizing traditional life insurance for end-of-life planning. While term policies offer high death benefits during peak earning years, they lack the permanence required for final arrangements. Most term policies expire after a fixed duration. If a policyholder outlives the term, they lose all equity and protection. This expiration risk makes term insurance a volatile vehicle for funeral expense insurance, where the primary objective is guaranteed liquidity at an uncertain date. The Paul Group advocates for a shift from temporary coverage to permanent, whole-life solutions that offer stability through the final stages of a financial legacy.

Why Term Insurance Often Fails the Senior Demographic

Requalifying for coverage at age 75 or 85 is often a mathematical impossibility for the average consumer. Health shifts and rigorous age-based risk assessments mean seniors are frequently priced out of the traditional market. Whole life or simplified issue policies represent a sustainable scaling of personal protection. They provide a permanent solution that skips the invasive medical exams required by traditional carriers, focusing instead on a streamlined health questionnaire. This accessibility ensures the policy remains in force regardless of how long the individual lives. For a deeper analysis of these structures, families should review the Best Final Expense Insurance for Seniors: Pros and Cons 2026.

Determining Your Ideal Coverage Amount

Policy sizing is a bespoke process. It isn’t about maximizing a payout; it’s about strategic alignment with actual costs. According to a consumer guide to funeral insurance, understanding the distinction between standard and pre-need options is critical for family clarity. With the median cost of a funeral with a casket and vault reaching $8,300 in recent 2023 industry reports, most families target a range between $5,000 and $25,000. This methodology addresses a specific equation: the sum of the funeral service, outstanding minor debts, and final medical bills.

A curated approach to coverage selection involves three primary factors:

-

Service Specifics: Deciding between cremation and traditional burial, which can differ in cost by over 40%.

-

Debt Resolution: Accounting for credit card balances or small personal loans that shouldn’t burden survivors.

-

Legacy Goals: Including a small "buffer" to provide an immediate cash gift to grandchildren or a chosen charity.

The beneficiary acts as the executor of this final financial plan. By matching the funeral expense insurance payout to these specific variables, families avoid the trap of being over-insured while ensuring no costs are left uncovered. Our group identity is rooted in this level of precision. We believe that a well-structured policy is the intersection of human leadership and operational systems, providing a clear path forward during a time of emotional complexity.

Regional Considerations: Planning Across the Western and Southern U.S.

Geography dictates the financial architecture of end-of-life planning. While federal guidelines provide a baseline, state-level regulations in California, Texas, and Florida create distinct environments for funeral expense insurance. Families must align their policies with local statutes to ensure seamless benefit disbursement. California’s Department of Insurance enforces strict consumer protection laws that influence policy transparency. In Florida, high demand in markets like Miami drives premium structures that reflect the state’s unique demographic density. Our methodology focuses on these nuances to ensure your policy remains resilient against regional economic shifts.

Navigating Costs in California and Florida

Strategic planning in coastal hubs requires an understanding of localized inflation. In Los Angeles, the median cost of a traditional funeral often exceeds national averages by 18 percent. Florida residents face similar pressures, particularly regarding cemetery property in land-scarce regions. Effective policy curation involves accounting for these regional price tiers. The Paul Group prioritizes structural integrity by reviewing how state-specific benefits, such as those provided by the VA for veterans interred at Riverside National Cemetery, integrate with private coverage. This holistic approach ensures that no capital is left underutilized. We help families tailor their coverage to the high cost of living prevalent in Miami and San Francisco, ensuring the death benefit retains its purchasing power.

The Texas and Arizona Landscape: Burial vs. Cremation

The Southwest presents a study in cultural divergence. Texas remains a stronghold for traditional burial; Dallas and Houston see a consistent demand for multi-day services and ornate monuments. Conversely, Arizona reflects a significant shift toward cremation. The Cremation Association of North America (CANA) reported in 2023 that Arizona’s cremation rate surpassed 70 percent. Choosing the right funeral expense insurance means matching the death benefit to these specific preferences. The Paul Group serves as a Wise Advisor in these markets, offering a regional broker network that understands the nuances of Phoenix’s memorial trends versus the traditional expectations found in San Antonio. This localized expertise transforms a standard policy into a precision-engineered financial tool for retirees in these growing hubs.

Ready to optimize your family’s financial legacy with a strategy tailored to your specific region? Explore our detailed analysis of the best funeral expense insurance for seniors to find the right fit for your state.

Securing Your Legacy with The Paul Group: A Bespoke Approach

Since its founding in 2009, The Paul Group has refined a methodology specifically engineered for the senior demographic. We reject the cold, transactional nature of modern call centers that prioritize volume over value. Our firm operates on an agent-driven partnership model that emphasizes human leadership alongside sophisticated operational systems. This ensures your funeral expense insurance is not a generic commodity but a strategic asset. Every family possesses a unique financial DNA. We take the necessary time to diagnose your specific challenges before prescribing a solution, ensuring your legacy is built on a foundation of structural integrity.

The Paul Group Advantage: Expertise and Empathy

Our identity as a Wise Advisor combines intellectual rigor with underlying warmth. This professional posture is essential when addressing the complexities of estate planning. Generalist insurance firms often lack the granular knowledge required to navigate the nuances of senior health profiles, leading to delays or suboptimal coverage. The Paul Group offers a specialized alternative. We focus on securing immediate coverage and no-exam qualifications, removing the traditional barriers that often stall the application process. This bespoke quality is the hallmark of our premium positioning. We aim for total optimization, providing a sense of reassurance that your most complex organizational challenges are solvable through disciplined intervention.

Your Path Forward: Starting the Transformation

The journey toward strategic alignment begins with a focused consultation designed to move you from a state of complexity to one of absolute clarity. During the application phase, you aren’t merely engaging a salesperson; you’re accessing a collective of experts dedicated to excellence. Our process follows a logical, rhythmic cadence:

-

Strategic Alignment: An initial session to define your legacy goals and financial boundaries.

-

Market Synthesis: Our experts analyze the 2026 landscape using a proprietary curation methodology.

-

Bespoke Delivery: We provide a tailored quote that reflects your specific risk profile and long-term objectives.

This partnership-driven approach ensures your final arrangements are governed by order and foresight. We invite you to move beyond the uncertainty of generalist advice. For those seeking a deeper analysis of available options, our guide on the best final expense insurance for seniors provides further clarity. Secure your future through a disciplined intervention that values stability over superficial fixes. The Paul Group stands ready to serve as your trusted strategic partner in this essential transformation.

Securing Your Family’s Financial Architecture for 2026

The economic landscape of 2026 demands a proactive shift in how families approach end-of-life planning. Relying on traditional savings often proves insufficient when faced with the 4.4% average annual cost increase reported by industry benchmarks over the last decade. By integrating funeral expense insurance into your broader estate strategy, you transform a potential period of financial volatility into a structured, predictable transition. The Paul Group has specialized in the unique needs of seniors since 2009, offering a methodology that prioritizes immediate stability over bureaucratic delay. Our reach extends across California, Texas, Florida, Arizona, and 12 other states, ensuring your coverage aligns with specific regional market realities. We provide immediate coverage options that require no medical exam, removing the barriers that typically stall essential legacy planning. This isn’t just about a policy; it’s about the structural integrity of your family’s future. You deserve a partner who understands that true peace of mind is engineered through discipline and foresight.

Request Your Bespoke Final Expense Strategy and Quote Today

Your legacy is a reflection of your lifelong commitment to your loved ones, and we’re here to help you protect it with the precision it deserves.

Frequently Asked Questions

What is the difference between funeral expense insurance and burial insurance?

Funeral expense insurance and burial insurance are functionally identical terms describing a small whole life policy. These instruments provide a death benefit specifically intended to mitigate the financial impact of end-of-life logistics. While names differ based on regional marketing, the underlying strategic methodology remains focused on permanent protection with fixed premiums. Families shouldn’t view them as distinct products but rather as curated tools for maintaining structural estate integrity.

Can I qualify for funeral expense insurance if I have existing health issues?

You can secure coverage despite existing health conditions by selecting a guaranteed issue or simplified issue policy. The Paul Group prioritizes strategic alignment between your medical history and specific underwriting criteria to optimize approval rates. For individuals with chronic conditions, a guaranteed issue path ensures no medical exam is required. This methodology guarantees that 100% of applicants within the eligible age range receive a policy regardless of their physical transformation.

How much does a typical funeral expense insurance policy cost in 2026?

Industry data from the 2023 NFDA report indicates the median cost of a funeral reached $8,300, which informs the necessary funeral expense insurance coverage levels for 2026. Premiums are calculated based on your age at enrollment and the total benefit amount selected. While we don’t set flat rates, a 65-year-old male might pay between $50 and $100 monthly for a $10,000 policy. This investment provides a sustainable scaling of protection against rising service costs.

Is there a waiting period before my coverage becomes active?

Coverage begins immediately with simplified issue policies, whereas guaranteed issue options typically include a 24-month graded benefit period. If a natural death occurs within the first two years of a graded policy, beneficiaries often receive a return of premiums plus 10% interest. This structural safeguard allows the insurance carrier to manage risk while offering protection to those with complex health profiles. We help you evaluate which timeline aligns with your family’s immediate needs.

Are the death benefits from funeral insurance taxable for my beneficiaries?

Death benefits are generally exempt from federal income tax under Internal Revenue Code Section 101(a)(1). This tax-advantaged status ensures that the full liquidity of the policy is available for its intended purpose. It’s a critical component of a holistic financial strategy, preventing the erosion of assets during the transfer of wealth. Your beneficiaries receive the total curated benefit amount without the burden of a 15% or 20% tax liability on the payout.

Can the insurance company cancel my policy if my health declines later?

Your policy cannot be canceled by the insurer due to a decline in your health as long as you maintain premium payments. These contracts are designed for long-term stability and are legally classified as guaranteed renewable. This means your protection remains intact even if you develop a chronic illness or experience a significant physical transformation after the policy’s effective date. The Paul Group emphasizes this feature to ensure your family’s future remains secure.

How quickly does the beneficiary receive the payout after a claim is filed?

Beneficiaries typically receive funds within 24 to 72 hours once the death certificate and claim forms are verified. This rapid liquidity is essential for managing immediate operational requirements like transportation and service arrangements. We streamline the claim process to ensure that the transition is handled with professional discipline. Quick access to capital prevents the need for families to utilize high-interest credit or liquidate long-term investments during a period of emotional transition.

Does The Paul Group offer policies in my state?

The Paul Group provides strategic advisory services and policy placement in 48 states, though we don’t currently offer coverage in New York or Hawaii. Our collective of experts maintains deep knowledge of state-specific regulations to ensure your coverage meets local compliance standards. This broad geographic reach allows us to deliver a consistent, high-level experience for families across the country. We focus on tailoring solutions that reflect the unique legal DNA of your region.

Leave a Reply