How to Become a Final Expense Agent: A Career Guide for 2026

The U.S. Census Bureau projects that the population aged 65 and older will reach 80.8 million by 2040, yet the insurance industry remains plagued by high-volume recruitment models that prioritize headcount over professional mastery. You’ve likely noticed that the traditional path of learning how to become a final expense agent often feels less like a career launch and more like an initiation into a predatory sales cycle. It’s a valid concern; many agencies operate on churn rather than the strategic alignment of agent expertise and client needs. We understand the frustration of seeking a legitimate professional transformation only to be met with vague promises and low-quality leads.

This guide provides a disciplined methodology to help you transition from uncertainty to a position of quiet confidence in the 2026 market. We’ll outline the precise state-specific licensing requirements and the critical differences between captive and independent models to ensure your career architecture is built for sustainable scaling. You’ll gain a clear roadmap for selecting a partnership-driven group that values intellectual rigor over sheer call volume. This briefing details the framework necessary to establish a bespoke practice that serves both your professional ambitions and your clients’ long-term stability.

Key Takeaways

-

Analyze the 2026 demographic shifts to understand why the surging demand for senior life insurance coverage presents a high-growth opportunity for strategic professionals.

-

Master the essential pre-licensing education and state-specific examination requirements to understand exactly how to become a final expense agent in a competitive landscape.

-

Evaluate the structural advantages of independent brokerage models and a curated portfolio of carriers over the limitations of restrictive captive agency environments.

-

Cultivate sophisticated emotional intelligence and technical underwriting expertise to navigate sensitive end-of-life discussions with professional rigor and empathy.

-

Discover the precise methodology for transitioning from a licensed professional to an operational expert within The Paul Group’s strategic collective of industry specialists.

Table of Contents

Understanding the Final Expense Market Dynamics in 2026

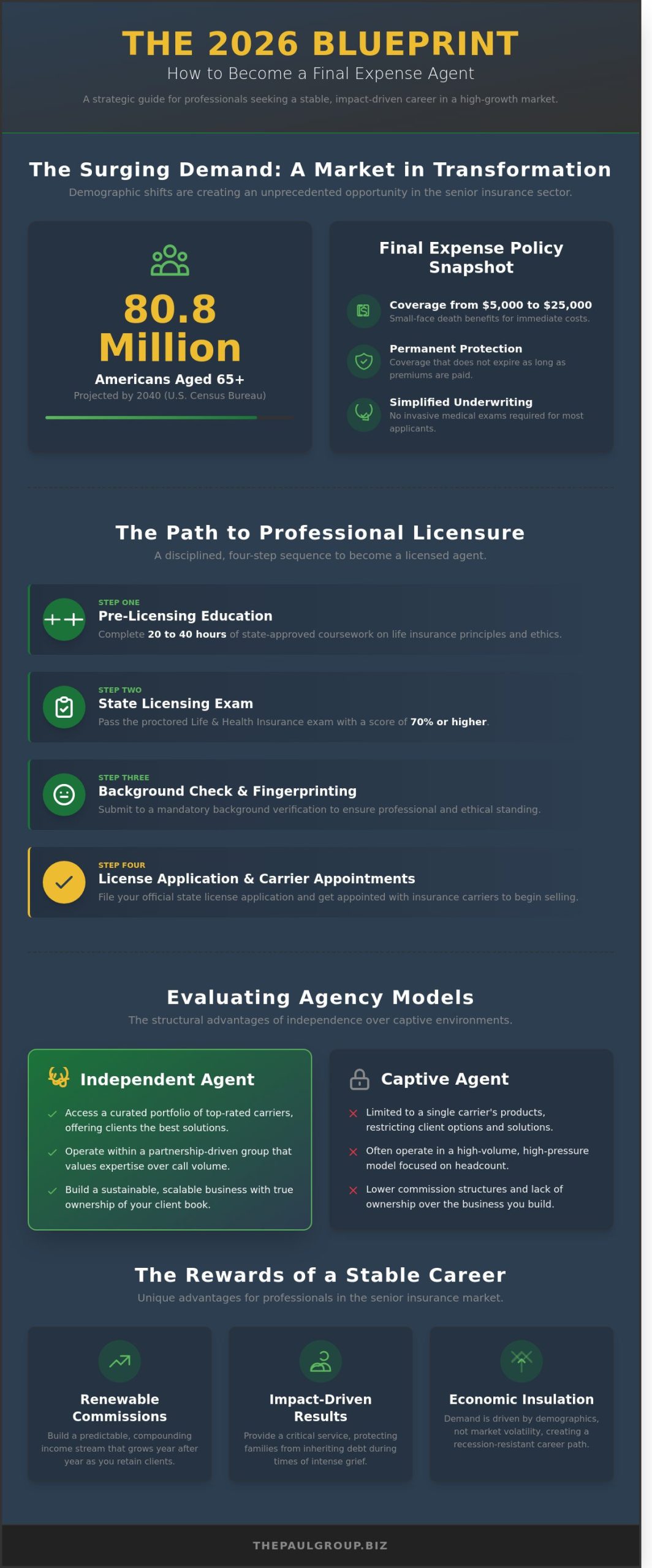

The role of a Final Expense Agent has matured into a specialized discipline within the broader life insurance sector. As you investigate how to become a final expense agent, you’ll find that success requires more than a simple license. It demands a deep understanding of the senior psychological profile and the socioeconomic factors that drive their decision-making. By 2026, the United States Census Bureau projects that over 68 million individuals will be aged 65 and older. This demographic shift represents a massive expansion of the addressable market. It isn’t a temporary trend; it’s a structural change in the American economy that prioritizes end-of-life planning and legacy preservation.

The Scope of Final Expense Insurance

Small-face permanent death benefits define these policies, with coverage typically ranging from $5,000 to $25,000. Unlike traditional term life policies that often expire before they’re needed, final expense insurance provides permanent protection that stays in force as long as premiums are paid. The absence of invasive medical exams makes these products accessible to seniors who might otherwise be uninsurable due to chronic health conditions. The focus is narrow and vital: covering immediate funeral costs, medical bills, and legal fees. Data from the National Funeral Directors Association shows funeral costs rising consistently, making these policies a practical necessity for middle-income families who want to avoid passing debt to their children.

Why This Career Path Offers Stability

Market resilience is a hallmark of the senior insurance sector. While high-growth investment products suffer during periods of market volatility, the need for burial coverage remains non-negotiable. This creates a foundation for a stable, long-term career that isn’t tethered to interest rate fluctuations. Professionals in this space enjoy several unique advantages:

-

Renewable Commissions: Building a book of business creates a predictable, compounding income stream that grows year over year as you maintain your client base.

-

Economic Insulation: The demand for end-of-life products is driven by biology and demographics, not the performance of the S&P 500.

-

Impact-Driven Results: Agents provide a critical social service by preventing families from inheriting thousands of dollars in debt during times of intense grief.

The Paul Group distinguishes itself by moving beyond the transactional salesperson archetype. We implement the Wise Advisor approach, a methodology rooted in strategic intervention and holistic planning. This means prioritizing the client’s long-term dignity over a quick commission. For those learning how to become a final expense agent, this distinction is the difference between a temporary job and a sustainable career. We focus on curated solutions that fit the unique DNA of each family’s financial situation. You can explore our detailed breakdown of the best final expense insurance for seniors to understand the rigorous standards we apply to product selection and strategic alignment.

Navigating Licensing and State Requirements Across the US

The foundation of a successful career in this sector rests on a rigorous regulatory framework. Precision is mandatory. Mastery of these legal prerequisites ensures that your practice begins with structural integrity. To understand how to become a final expense agent, you must first commit to a disciplined four step sequence that satisfies both state and federal oversight. This process transforms a candidate into a legitimate professional ready for high level engagement.

-

Step 1: Pre-licensing Education. Most states require 20 to 40 hours of coursework through approved providers. This ensures you grasp the technical nuances of life insurance contracts and the ethical standards governing the 2026 market.

-

Step 2: The Life and Health Insurance Exam. You must achieve a passing score, typically 70% or higher, on your primary state proctored exam. This test validates your intellectual rigor and readiness to advise seniors on complex financial products.

-

Step 3: National Producer Number (NPN) and Licensing. Once you pass the exam, you apply for your NPN. This unique identifier allows you to track your credentials across all jurisdictions via the state licensing requirements portal.

-

Step 4: Errors and Omissions (E&O) Insurance. Secure a policy with a minimum of $1,000,000 in coverage. This protects your personal assets and business reputation from potential litigation, providing a layer of security for your growing practice.

Regional Nuances: Florida, Texas, and California

Strategic expansion requires an understanding of localized mandates. The Florida Department of Financial Services mandates a specific fingerprinting process through Identogo before license approval. In Texas, the Department of Insurance utilizes the Sircon portal for streamlined application processing, which typically takes 5 to 10 business days. California remains the most rigorous; it requires 12 hours of specific ethics training and a deep focus on consumer protection laws that govern senior insurance sales. These variations demand a curated approach to compliance.

The Power of Reciprocal Licensing

Building a multi state agency is a hallmark of sustainable scaling. By leveraging reciprocity, you can extend your reach into growth markets like Arizona, New Mexico, and Oregon without retaking exams. Managing these non resident licenses through the National Insurance Producer Registry (NIPR) provides the administrative clarity needed for efficient operations. This methodology allows agents to diversify their portfolio and mitigate regional economic shifts. As you refine your approach, you might also explore the best final expense insurance for seniors to ensure your product knowledge matches your licensing expertise.

The Paul Group views licensing not as a hurdle, but as a strategic asset. It’s the first step toward professional excellence. If you seek to optimize your entry into this market, consider a consultation with The Paul Group to align your professional trajectory with high level industry standards.

Evaluating Agency Models: The Power of Strategic Alignment

Choosing the right infrastructure is the most critical decision when learning how to become a final expense agent. Your choice of agency model dictates your long-term scalability and the quality of your client relationships. Captive agencies often restrict agents to a single carrier; this creates a bottleneck that limits your ability to serve the diverse health profiles of the senior market. If a client doesn’t fit that one carrier’s strict underwriting, you lose the sale and the client loses protection.

Independent brokerage groups offer a superior alternative through a curated portfolio of 12 to 15 top-tier carriers. This flexibility ensures you can always find a placement for a client, regardless of their medical history. Strategic alignment also extends to commission structures. You should prioritize "vested day-one" contracts. This means you own your renewals from the first policy sold, providing immediate equity in your business rather than waiting three to five years for ownership to kick in.

Cultural fit is equally vital. High-pressure "boiler room" environments prioritize volume over value, which leads to high churn and agent burnout. A "Wise Advisor" culture fosters a disciplined, consultative methodology that focuses on long-term stability and professional integrity. It’s the difference between a transactional job and a sustainable professional practice.

Why The Paul Group Identity Matters

The Paul Group doesn’t provide generic sales training; it offers a specialized methodology focused exclusively on the unique needs of seniors. You gain access to bespoke training modules that go beyond basic scripts to address the complex psychological and financial nuances of the 65-plus demographic. This intellectual rigor is essential for success. For a deeper look at the market you’ll serve, review our analysis on the Best final expense insurance for seniors pros and cons 2026 to understand the product landscape.

Lead Generation vs. Lead Ownership

Many agencies distribute "recycled" leads that have been sold to multiple agents, which often results in a 90% rejection rate. We prioritize lead ownership and fresh data. Our strategy involves reaching seniors who are actively searching for protection, ensuring high-intent interactions. The Paul Group supports regional agents in AZ, FL, and TX with quality data and proprietary systems. This targeted approach transforms lead generation from a chaotic numbers game into a predictable, scalable system for growth. When you own the lead, you own the relationship from the very first touchpoint.

Developing the Expertise: Skills for the Sophisticated Agent

Transitioning from a general insurance producer to a sophisticated advisor requires a commitment to intellectual rigor and strategic alignment. When you analyze how to become a final expense agent, it’s clear that technical knowledge serves as the baseline while strategic execution acts as the differentiator. Mastering simplified issue underwriting is the first pillar of this professional evolution. It requires a deep understanding of pharmaceutical databases and health impairments to ensure clients receive the most favorable ratings. Elite agents achieve a 95% placement rate by meticulously pre-qualifying applicants before the digital application begins.

Beyond the initial sale, practice sustainability hinges on structural integrity. A high-volume client base demands a holistic approach to retention. Sophisticated agents implement automated touchpoints and annual policy audits to maintain a persistency rate above 88%. This disciplined intervention prevents lapses. It reinforces your role as a long-term strategic partner rather than a transactional salesperson.

The "Wise Advisor" Communication Style

Effective communication in the senior market requires authoritative brevity. You aren’t merely pitching a product; you’re facilitating a legacy preservation consultation. This methodology shifts the focus from monthly premiums to the structural stability of a family’s future. Active listening techniques allow you to identify specific financial gaps, such as outstanding medical debt or specific burial preferences. By explaining complex policy riders with clarity, you build the trust necessary for a long-term partnership. Success in 2026 depends on this ability to transform a sales pitch into a curated advisory session.

Technical Proficiency and Tools

Digital transformation has reshaped the insurance landscape. Agents now utilize mobile quote tools to provide field accuracy within seconds, eliminating the friction of traditional paper applications. By 2026, 90% of top-tier carriers will prioritize digital-first submissions for rapid, often instant, underwriting decisions. Integrating a CRM system allows for the sustainable scaling of a localized practice. It transforms a list of names into a structured database of relationships. This optimization ensures no client is overlooked during critical annual reviews, allowing the Group identity to remain strong through consistent service delivery.

Ready to align your professional strategy with high-performing products? Review our analysis of the best final expense insurance for seniors to better serve your clients.

Launching Your Career with The Paul Group

Entering the final expense sector requires more than a license. It demands a partnership that prioritizes long-term structural integrity and professional excellence. At The Paul Group, we view our application process as a gateway to joining a collective of diverse experts. We don’t prioritize mass recruitment; we focus on strategic alignment with individuals who embody our commitment to professional integrity. Our onboarding methodology is designed to move you from being merely licensed to fully operational through a disciplined, systems-based approach that ensures your success isn’t left to chance.

Understanding how to become a final expense agent involves mastering both human leadership and operational systems. We provide the structural support necessary for sustainable scaling in high-growth markets. Our current expansion focuses on the robust economic landscapes of California, Texas, and Florida, while also establishing a premium presence in the Pacific Northwest. These territories offer a dense concentration of the target demographic, allowing our agents to build portfolios based on stability rather than fleeting trends. By focusing on these strategic regions, we help you capitalize on the 7% projected increase in senior insurance needs expected by the end of 2026.

Your First 90 Days as a Paul Group Agent

The initial three months of your tenure are defined by curated mentorship and direct alignment with our senior leadership team. You won’t be left to decipher market complexities alone. We prioritize building your local presence in key metropolitan hubs like Phoenix and Miami, where demand for sophisticated final expense solutions remains high. During this phase, you’ll move through specific operational milestones designed to secure your first layers of commission-based independence. This isn’t a trial period; it’s a focused period of transformation where we refine your methodology to match the unique DNA of your local market. We ensure you have the tools to achieve consistent results within your first 90 days.

Ready to Transform Your Professional Path?

The path to becoming a top-tier producer requires a departure from traditional, transactional insurance models. It’s time to adopt a visionary approach to your career. If you’re a motivated professional seeking a partnership-driven environment, we invite you to contact our team for a confidential career briefing. We’ll discuss your goals, our strategic methodology, and how we can achieve mutual growth. Take the definitive step toward a career built on intellectual rigor and results. Join The Paul Group and lead with expertise today to begin your professional evolution.

Architecting Your Strategic Future in Senior Insurance

Navigating the complexities of the 2026 senior market requires more than a simple career change; it demands a total professional transformation. Success in this sector hinges on mastering the nuances of state-specific licensing across 15+ states, including key markets like California, Texas, and Florida. While many focus on the technicalities of how to become a final expense agent, the most successful professionals prioritize strategic alignment and a holistic understanding of senior demographics. Since our founding in 2009, The Paul Group has championed a partnership-driven model that replaces the traditional transactional approach with a curated methodology for sustainable scaling. We don’t just offer a job; we provide the operational systems and human leadership necessary for high-level optimization of your career trajectory. This journey is about building structural integrity within your business while delivering genuine value to a growing population. You’ve the potential to lead in an industry that rewards intellectual rigor and disciplined intervention. Your path to excellence starts with a decision to move beyond the ordinary and embrace a partnership built for the long term.

Partner with The Paul Group: Start Your Strategic Insurance Career Today

Frequently Asked Questions

Do I need a college degree to become a final expense agent?

You don’t need a college degree to learn how to become a final expense agent. State regulatory bodies, such as the Texas Department of Insurance, require a high school diploma or equivalent as the primary educational baseline. We prioritize intellectual rigor and strategic alignment over formal credentials. Success in this sector depends on your ability to master complex regulatory frameworks and execute disciplined sales methodologies.

How long does it typically take to get an insurance license in Florida or Texas?

Obtaining an insurance license typically requires 14 to 30 days of focused preparation in Florida and Texas. Florida mandates a 40 hour pre-licensing course for life and variable annuity lines. Texas doesn’t enforce a specific hourly requirement but necessitates passing a rigorous state examination and completing a fingerprint background check. This timeframe allows you to transition from a candidate to a licensed professional with strategic speed.

What is the average cost of starting a final expense insurance business?

Starting a final expense business requires a capital investment ranging from $400 to $900 for initial regulatory compliance. This includes state exam fees often priced between $40 and $60, licensing fees averaging $50 to $150, and Errors and Omissions insurance. Maintaining lean operational costs ensures sustainable scaling. These figures exclude lead generation expenses, which vary based on your chosen acquisition strategy and the specific market density you target.

Can I sell final expense insurance part-time while keeping my current job?

You can absolutely sell final expense insurance part-time while maintaining your current employment. Many successful partners utilize a 15 to 20 hour weekly schedule to build their initial book of business. This phased approach provides financial stability while you refine your strategic methodology. It’s a pragmatic way to transition into a full-time role once your renewal commissions reach a self-sustaining threshold.

What is the difference between a life insurance license and a health insurance license?

A life insurance license permits you to sell death benefit products, while a health insurance license focuses on medical and disability coverage. Final expense agents primarily utilize the life license to provide families with immediate liquidity for end-of-life costs. While some agents hold both for holistic client protection, the life authority is the core requirement for this specific niche. Precise licensing ensures you remain compliant with state statutes.

How much can a new final expense agent realistically earn in their first year?

New agents often earn between $45,000 and $75,000 in their first year, according to 2023 industry data for independent life insurance producers. High-performing individuals who master the nuances of how to become a final expense agent can exceed $100,000 by optimizing their lead conversion rates. Your income reflects your disciplined adherence to a proven sales system. Results correlate directly with the volume of strategic client interactions you conduct weekly.

Is a medical exam required for the agent or the client in final expense plans?

Medical exams aren’t required for agents, and most final expense plans use simplified issue underwriting that skips the physical exam for clients. This streamlined process allows for rapid policy approval, often within 24 to 48 hours. Clients simply answer a series of health questions to determine eligibility. This efficiency reduces friction in the sales cycle, enabling you to provide immediate reassurance to the families you serve.

Does The Paul Group provide training for newly licensed agents?

The Paul Group provides a comprehensive training ecosystem designed for newly licensed agents seeking strategic mastery. Our methodology moves beyond basic product knowledge to focus on operational excellence and sustainable scaling. We offer a curated mentorship program that aligns your individual goals with our proven organizational systems. This partnership ensures you aren’t just selling policies but are building a resilient, professional practice with long-term stability.

Leave a Reply