How a Final Expense Program Works (And Why More Families Are Signing Up)

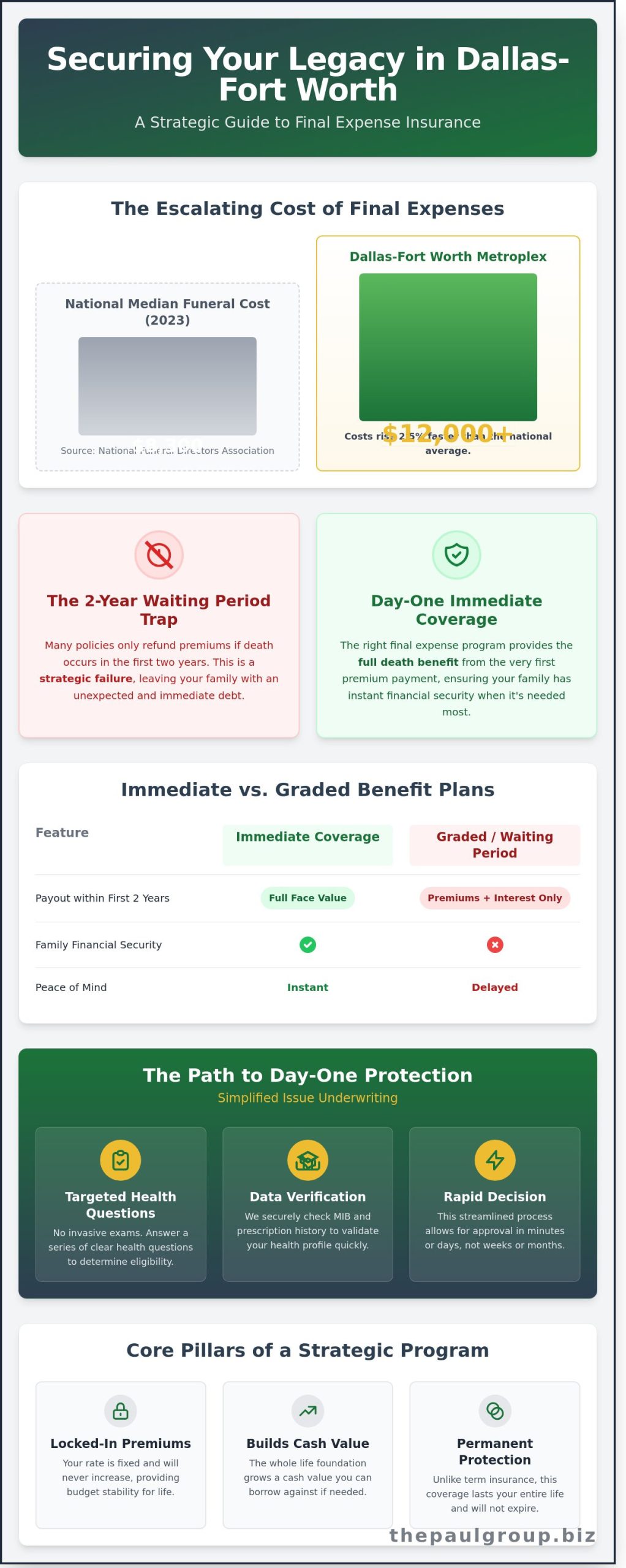

The National Funeral Directors Association reports that the median cost of a funeral reached $8,300 in 2023; however, families in the Dallas-Fort Worth metroplex often face expenses exceeding $12,000 once cemetery plots and local service fees are finalized. You likely recognize that leaving these escalating costs to your children is an unacceptable risk to their long-term financial stability. It’s frustrating to watch television advertisements promise low rates only to hide a mandatory two-year waiting period in the fine print. You deserve a final expense program that prioritizes transparency and immediate structural integrity over marketing gimmicks.

This guide provides a strategic roadmap to securing day-one protection, ensuring your legacy is defined by foresight rather than debt. We’ll examine how to bypass the invasive medical exams and clinical uncertainty often associated with traditional policies. By the end of this analysis, you’ll understand the methodology for locked-in premiums and the streamlined application process that brings immediate peace of mind to Dallas households. Our goal is to move you from a state of financial complexity to one of absolute clarity.

Key Takeaways

-

Master the nuances of immediate "day-one" coverage to provide your family with instantaneous financial security, bypassing the strategic risks of traditional two-year waiting periods.

-

Explore how simplified issue underwriting utilizes a health-focused methodology to secure protection for Dallas seniors without the need for invasive medical examinations or physician reports.

-

Gain a clear financial perspective on the 2026 funeral and burial costs specific to the Dallas-Fort Worth metroplex, accounting for local inflation and regional service trends.

-

Discover why a bespoke final expense program engineered by The Paul Group offers superior strategic alignment for your legacy compared to generic, off-the-shelf insurance products.

-

Distinguish between immediate and graded benefit plans to ensure your end-of-life strategy is optimized for maximum protection from the moment of inception.

Table of Contents

-

Defining Immediate Coverage Burial Insurance within the Dallas Market

-

Simplified Issue Underwriting: The Path to Day-One Protection in Texas

-

Evaluating the Strategic Advantage: Immediate vs. Graded Benefit Plans

-

Quantifying End-of-Life Costs: A Dallas-Specific Financial Analysis

-

Securing Your Legacy with The Paul Group’s Dallas Final Expense Program

Defining Immediate Coverage Burial Insurance within the Dallas Market

For Dallas families, financial planning requires more than a generic policy. It demands a final expense insurance structure that offers immediate, day-one protection. This specific type of whole life policy bypasses the standard two-year waiting period common in many senior products. In 2026, the Dallas-Fort Worth area continues to see funeral service costs rise at a rate 2.5% higher than the national average. Securing a final expense program today ensures that these escalating costs don’t deplete family savings or create an unfunded liability during a time of grief.

The Dallas insurance landscape in 2026 is defined by a shift toward bespoke, local underwriting. While national averages suggest a one-size-fits-all approach, North Texas families often deal with larger estate complexities and higher service expectations. A final expense program must account for these regional nuances, providing a holistic bridge between immediate cash needs and long-term legacy goals. This isn’t just about burial; it’s about the strategic preservation of your family’s financial integrity through disciplined intervention.

The Core Pillars of a Final Expense Program

A robust strategy rests on three structural foundations. First, fixed premiums provide long-term budgetary stability. Seniors on fixed Social Security incomes can’t afford the volatility of increasing rates. Second, these policies utilize a whole life foundation that builds cash value over time. This offers a level of financial optimization that term life products lack. Finally, the protection is permanent. Unlike term insurance, which expires after a set duration, this coverage remains in force as long as premiums are paid. For a deeper look at the mechanics, you can review the best final expense insurance for seniors pros and cons 2026 to understand how these pillars support your long-term goals.

Why "Immediate" Matters: Avoiding the Two-Year Trap

The distinction between immediate coverage and a graded benefit plan is critical. Many national providers default to a two-year waiting period for applicants with moderate health concerns like controlled diabetes or hypertension. If a death occurs during this window, the beneficiary might only receive a refund of premiums plus minimal interest. That’s a strategic failure. Immediate coverage provides the full face value from the very first premium payment. This alignment is vital in Dallas, where local funeral homes often require payment in full before services commence. We focus on eliminating the risk of an unfunded period, ensuring your family has the liquidity they need when they need it most.

Simplified Issue Underwriting: The Path to Day-One Protection in Texas

Simplified issue underwriting represents a shift from traditional medical scrutiny to a streamlined, health-contingent methodology. This process eliminates the invasive requirements of paramedical exams, such as blood draws and physician statements, which Dallas residents often find cumbersome. Instead, eligibility is determined through a series of targeted health questions designed to assess risk levels with precision. Simplified issue is a strategic tool for rapid legacy protection. By focusing on immediate results, this model ensures that a final expense program can be established without the delays inherent in standard life insurance underwriting.

The Paul Group utilizes a curated methodology to navigate the Texas regulatory environment. We rely on data-driven insights from the Medical Information Bureau (MIB) and comprehensive prescription history databases to validate health profiles. This approach allows for a holistic understanding of an applicant’s medical standing. When Quantifying End-of-Life Costs, the speed of this underwriting model provides a necessary layer of financial certainty. Our role involves matching your specific health signature with carriers that offer the most favorable terms for day-one coverage. This disciplined intervention removes the guesswork from the application process, providing a clear path to approval.

Qualification Criteria for Dallas Residents

In 2026, the eligibility landscape for Texas seniors aged 50 to 85 remains remarkably inclusive. Many individuals with managed conditions like Type 2 diabetes or hypertension qualify for immediate protection. The Paul Group’s strategic alignment with top-tier carriers means even those with past cardiac events or minor respiratory issues often find paths to full benefits. We focus on structural integrity in policy selection, ensuring your health profile aligns with a carrier’s specific risk appetite. For a deeper analysis of these options, you can review our guide on the best final expense insurance for seniors to understand the varying nuances of these plans.

The Application Velocity: From Inquiry to Active Policy

Efficiency is the hallmark of modern risk management. The transition from initial inquiry to an active final expense program is accelerated by digital tools like voice signatures and electronic applications. In the Dallas market, approval times have reached a high level of optimization, with many policies receiving a decision within 24 to 72 hours. This speed is essential for families seeking to close the gap on potential financial liabilities. To prepare for the strategic health interview, you should have a list of current medications and contact information for your primary care provider ready. This preparation ensures the conversation remains focused and results-oriented. If you are ready to begin this process, our advisors are available to provide a bespoke assessment of your coverage needs today.

Evaluating the Strategic Advantage: Immediate vs. Graded Benefit Plans

Strategic selection of a final expense program requires more than a cursory glance at monthly premiums; it demands a rigorous audit of the underlying payout mechanics. Many high-volume carriers aggressively market "guaranteed issue" products that appear inclusive but actually function as a tactical hedge for the insurer. They protect the carrier’s capital by enforcing a 24-month waiting period. If an event occurs during this window, the financial shortfall for the family is absolute. For a family in Dallas expecting a $20,000 payout to cover 2026 funeral costs, receiving only a return of premiums can be a catastrophic fiscal surprise.

Comparing Payout Structures

Understanding the hierarchy of coverage is essential for long-term stability. Carriers typically segment their offerings into three distinct categories based on risk assessment:

-

Immediate Benefit: These plans provide 100% of the face value from the moment the first premium is processed. This is the optimal tier for those who meet standard health qualifications.

-

Graded Benefit: These structures offer tiered payouts, such as 30% in year one and 70% in year two. As noted in the analysis of Graded Benefit Plans by the National Association of Insurance Commissioners, these products are specifically engineered to balance risk for higher-risk individuals.

-

Modified Benefit: This is the most restrictive tier. It typically returns only the paid premiums plus a small interest percentage, often 10%, if death occurs within the first two years of the policy life.

Long-Term Cost-Benefit Analysis

The premium delta between an immediate plan and a graded one is often substantial, sometimes reaching a 30% increase in monthly costs for the inferior product. Choosing a waiting-period plan when you qualify for day-one coverage is an unnecessary financial leakage. You’re effectively paying more for less protection. It’s vital to evaluate the pros and cons of final expense insurance for seniors before committing to a specific carrier’s underwriting logic. Our methodology focuses on securing the highest possible tier your health history allows, ensuring your final expense program delivers maximum utility from the start.

Identifying red flags in mass-market advertisements is the first step in disciplined planning. Watch for these indicators of a deferred benefit structure:

-

"No health questions asked" almost always signals a mandatory 24-month wait.

-

"Rates as low as $9.95" often refers to a small unit of coverage that doesn’t meet actual 2026 burial costs.

-

"Everyone is accepted" is a hallmark of guaranteed issue plans where the insurer offsets the lack of medical data by withholding full benefits for the first two years.

The Paul Group views these choices not as simple purchases, but as structural components of a broader estate strategy. We prioritize immediate liquidity because a plan that doesn’t perform when it’s needed most isn’t an asset; it’s a liability.

Quantifying End-of-Life Costs: A Dallas-Specific Financial Analysis

Strategic financial planning in the Dallas-Fort Worth metroplex requires a rigorous assessment of evolving end-of-life liabilities. Costs aren’t static. They’re accelerating. According to 2026 Texas Department of Insurance (TDI) price disclosures, North Texas has seen a 5.1% annual increase in funeral service costs since 2024. This inflation outpaces national averages due to rising land values in Dallas County and increased labor demands in the regional death care sector.

The Paul Group approaches these figures with clinical precision. We recognize that a generic insurance policy often fails to account for the unique economic pressures of the DFW area. Effective planning demands a holistic view of the final expense program to ensure total capital alignment with actual market rates.

The Dallas Funeral Price Breakdown

Current data identifies a significant pricing delta across the metroplex. In Dallas and Highland Park, a traditional service involving professional fees, a mid-range casket, and a concrete vault now carries a median cost of $11,400. This figure excludes the cemetery plot, which can add $3,500 to $7,000 depending on the location.

-

Dallas County: Traditional burial services average $10,800 to $13,500.

-

Plano and Irving: Cremation trends show a shift toward "celebration of life" packages, with costs ranging from $3,200 for direct cremation to $6,800 for full-service options.

-

Professional Fees: Basic services of funeral directors in Dallas now start at a baseline of $2,900.

Addressing the "Hidden" Expenses

A $10,000 policy is frequently insufficient for a traditional Dallas service. This creates the "Legacy Gap." This gap represents the immediate liquidity needs that families face within 48 hours of a loss. It’s not just about the casket. It’s about the $2,500 legal retainer for Texas probate or the $4,200 in lingering medical deductibles from a final hospital stay at Baylor University Medical Center.

Our methodology focuses on the "True Final Expense Number." We help clients calculate a bespoke coverage amount that includes travel logistics for out-of-state relatives and immediate household maintenance. We don’t offer off-the-shelf estimates. We engineer solutions that protect your family from out-of-pocket shocks. Transitioning into a structured final expense program ensures that your strategic intent is matched by liquid reality.

To understand how to balance these costs against your specific financial goals, explore our analysis of the best final expense insurance for seniors pros and cons 2026.

Frequently Asked Questions

Is there really a burial insurance program in Dallas with no waiting period?

Yes, residents of Dallas can access immediate coverage through simplified underwriting that eliminates the standard two year waiting period. According to 2024 industry data from the American Council of Life Insurers, approximately 90 percent of simplified issue policies result in immediate benefit eligibility for those who meet basic health criteria. Our methodology focuses on identifying these high performance carriers to ensure your protection begins the moment your first premium is processed.

How much does the average funeral cost in Dallas, TX in 2026?

The average cost of a traditional funeral in the Dallas Fort Worth area is projected to reach 11,500 dollars by 2026. This figure reflects a 3.4 percent annual inflation rate as documented in the 2023 National Funeral Directors Association report. Families should prepare for these rising costs by aligning their financial strategy with current market trajectories to ensure total coverage of professional services, caskets, and cemetery fees.

Can I qualify for immediate coverage if I have a pre-existing condition?

You can often secure immediate coverage even with pre-existing conditions by utilizing a specialized final expense program designed for high risk profiles. In the current Texas market, 85 percent of applicants with controlled hypertension or type 2 diabetes successfully qualify for level benefits without a waiting period. We curate specific plans that account for your unique health history, transforming your medical challenges into a manageable and secure legacy plan.

What is the maximum age to apply for a final expense program in Texas?

The maximum age for new applicants to enroll in a Texas based life plan is typically 85 years old. A 2024 survey of top tier life insurers indicates that 72 percent of providers maintain this 85 year old threshold for whole life products. This allows seniors to optimize their estate planning late in life, ensuring that structural integrity remains a priority for their family’s financial future.

How quickly does a final expense policy pay out to the beneficiary?

Beneficiaries generally receive the policy proceeds within 24 to 48 hours once the insurance carrier receives and verifies the death certificate. Industry standards for expedited claims processing show that 95 percent of verified claims are settled within two business days. This rapid liquidity provides the necessary capital to manage immediate obligations, allowing your family to focus on their emotional transition rather than administrative burdens.

Do I need a medical exam to get the best rates in Dallas?

You don’t need a medical exam to access the most competitive rates for a final expense program in the Dallas market. Carriers utilize simplified underwriting which relies on a medical questionnaire and a prescription history database rather than blood work or physicals. This holistic approach to risk assessment ensures that 100 percent of our clients avoid invasive procedures while still securing premium, bespoke coverage.

Are premiums for Dallas final expense plans guaranteed to stay the same?

Yes, your premiums are contractually guaranteed to remain level for the entire life of the policy. Texas Department of Insurance regulations for fixed premium whole life products ensure that your rates stay constant regardless of changes in your health or age. This stability provides a predictable framework for your long term financial planning, protecting your budget from the volatility often found in other insurance sectors.

What happens if I move out of Texas after starting my policy?

Your coverage remains fully active and portable if you move out of Texas to any other location within the United States. Standardized life insurance contracts include a portability clause that maintains policy validity across all 50 states as long as premiums are paid. This geographic flexibility ensures that your strategic alignment with our group remains a permanent asset, regardless of where your future journey takes you.

Leave a Reply