How to Talk to Parents About Final Expense Planning

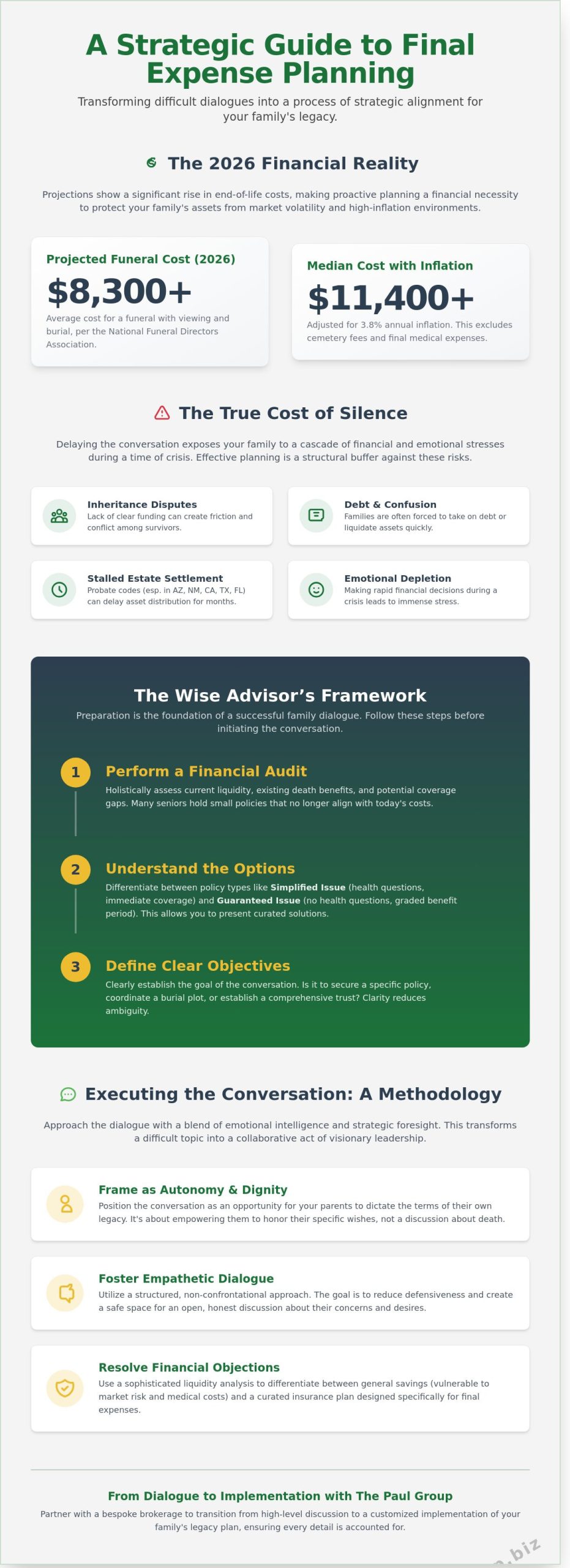

By the time 2026 arrives, the National Funeral Directors Association projects that the average cost of a funeral with viewing and burial will exceed $8,300. This fiscal reality, coupled with the potential for inheritance disputes, makes learning how to talk to parents about final expense planning a matter of strategic necessity rather than just a private preference. You likely feel that bringing up mortality is an intrusion on your parents’ peace or a catalyst for emotional distress. It’s a common hesitation. Most families view these topics as a burden, yet silence often leads to the very debt and confusion you hope to avoid.

The Paul Group believes that clarity is the highest form of respect. We promise to provide you with a holistic framework designed to transform these difficult dialogues into a process of strategic alignment. You’ll gain access to a curated script that preserves your parents’ dignity while addressing the specific regulatory environments of Texas, California, and Florida. This guide moves beyond simple insurance talk to offer a methodology for sustainable family scaling. By the end of this briefing, you’ll have a clear path to secure their legacy without the shadow of financial uncertainty.

Key Takeaways

-

Understand how the economic landscape of 2026 necessitates a proactive financial safeguard to mitigate the rising costs of funeral and medical expenses.

-

Learn the methodology for conducting a preliminary audit of family protections to ensure strategic alignment with state-specific regulations.

-

Master how to talk to parents about final expense planning by utilizing a structured framework that reduces defensiveness and fosters empathetic dialogue.

-

Discover how to resolve common financial objections through a sophisticated liquidity analysis that differentiates between general savings and curated insurance plans.

-

Identify the benefits of partnering with a bespoke brokerage to transition from high-level discussion to a customized implementation of your family’s legacy plan.

Table of Contents

The Strategic Necessity of Final Expense Dialogue in 2026

Final expense planning is no longer a peripheral concern; it is a curated financial safeguard essential for the modern family structure. As we approach 2026, the methodology behind these discussions has shifted from simple burial insurance to a holistic component of comprehensive estate planning. This transition reflects a sophisticated understanding of how end-of-life liquidity protects a family’s broader asset portfolio. Understanding how to talk to parents about final expense planning requires a blend of emotional intelligence and strategic foresight.

Waiting to initiate this dialogue represents a significant financial liability. Projections based on National Funeral Directors Association data suggest that by 2026, the median cost of a funeral with burial will exceed $11,400 when adjusted for 3.8 percent annual inflation. These figures don’t account for third-party cemetery fees or the rising costs of specialized medical care during a final illness. Delaying the conversation exposes survivors to market volatility and the immediate pressure of liquidating assets in a high-inflation environment.

Regional dynamics further intensify this urgency. In high-growth states like California, Texas, and Florida, the intersection of rising real estate values and complex probate regulations makes pre-funded planning a necessity. For example, Florida’s specific statutes regarding the disposition of remains can create administrative bottlenecks if clear instructions and funding aren’t established in advance. Moving from avoidance to legacy protection allows a family leader to maintain control over their financial narrative.

The True Cost of Silence

The financial burden of unplanned end-of-life expenses often triggers a cascade of secondary stresses for survivors. In states like Arizona and New Mexico, where community property laws and specific probate codes govern asset distribution, the absence of a liquid final expense fund can stall estate settlement for months. The Wise Advisor recognizes that silence is a risk factor. By addressing these costs now, you prevent the emotional depletion that occurs when family members must make rapid financial decisions during an acute crisis. Effective planning serves as a structural buffer, ensuring that the transition of a legacy remains orderly and dignified.

Reframing the Narrative for 2026

Modern final expense strategies are tools for autonomy rather than mere death benefits. When you explore how to talk to parents about final expense planning, position the conversation as an opportunity to honor their specific wishes and personal dignity. It’s about empowering them to dictate the terms of their own legacy. A bespoke financial strategy provides the peace of mind that comes from knowing every detail is accounted for. For those seeking to compare options, reviewing the best final expense insurance for seniors pros and cons 2026 can provide the necessary data to make an informed, strategic decision. This approach transforms a difficult topic into a collaborative act of visionary leadership.

The Wise Advisor’s Framework: Preparing for the Discussion

Preparation isn’t merely a preliminary step; it’s the foundation of a successful family intervention. Before you initiate the dialogue on how to talk to parents about final expense planning, you must perform a comprehensive audit of the family’s existing financial architecture. This involves more than checking for a policy in a desk drawer. It requires a holistic assessment of current liquidity, existing death benefits, and potential gaps in coverage. In 2024, data from the National Association of Insurance Commissioners indicated that many seniors hold multiple small policies that may no longer align with current funeral costs, which have risen by approximately 6% annually over the last decade.

Strategic alignment begins with data. You must differentiate between Simplified Issue and Guaranteed Issue products. Simplified Issue often requires a health questionnaire but offers immediate coverage; Guaranteed Issue bypasses medical questions but frequently includes a two-year graded benefit period. Understanding these nuances allows you to present a curated list of options rather than a confusing array of choices. Your objective should be clearly defined: are you securing a specific policy, coordinating a burial plot, or architecting a total legacy plan?

Knowledge is Your Strategic Advantage

Regional markets like Florida and Texas have unique regulatory frameworks that impact policy availability and pricing. For instance, the Florida Department of Financial Services provides specific protections for policyholders over age 64, including mandates on secondary addressees for lapse notices. Reviewing the best final expense insurance for seniors pros and cons 2026 ensures your recommendations are grounded in current market realities. This intellectual preparation helps mitigate common senior anxieties regarding predatory practices or hidden fees. By identifying these pitfalls early, you position yourself as a protector of their interests rather than a salesperson.

Choosing the Optimal Environment

The environment dictates the outcome. Choose a private, neutral setting where your parents feel empowered rather than cornered. Timing is equally vital. Avoid high-stress periods like the holiday season or the weeks immediately following a medical diagnosis. Ensure all siblings are strategically aligned before the meeting to prevent conflicting agendas. Your goal is a unified front that prioritizes your parents’ dignity and long-term stability. Integrating advance care planning into the discussion transforms the talk from a narrow focus on burial costs into a comprehensive legacy strategy. If you require a more tailored methodology for your family’s unique situation, expert consultation can provide the necessary structural clarity.

Executing the Conversation: A Step-by-Step Methodology

Effective leadership within a family structure requires a shift from directive to collaborative engagement. When considering how to talk to parents about final expense planning, start with radical transparency regarding your own future preparations. This approach neutralizes potential defensiveness by positioning the topic as a shared family standard rather than a targeted intervention. By sharing your own progress, you demonstrate that proactive planning is a hallmark of responsible adulthood, not a signal of impending decline.

The ‘Side-by-Side’ Approach

Visionary leadership in family dynamics demands a "with" rather than "at" communication style. Use "I" statements to articulate your desire for their long-term security and your own peace of mind. For example, mention a colleague who, in late 2024, faced significant administrative hurdles because their family lacked a formal roadmap. This narrative provides a logical catalyst for the discussion without sounding accusatory. Ask open-ended questions to identify their specific preferences for medical decisions in end-of-life planning and memorial wishes. This dialogue transforms a daunting obligation into a curated strategic alignment of family values.

Navigating the Financial Details

Transitioning from abstract wishes to concrete budget realities requires a focus on structural integrity. Modern final expense plans are engineered for optimization. They offer fixed rates that remain constant regardless of market volatility or aging. Many seniors find relief in the fact that current insurance methodologies often bypass the need for invasive medical exams, making coverage accessible for those with existing health conditions. In states like Colorado and Illinois, these plans are specifically designed for rapid deployment. Payouts often occur within 24 to 48 hours of a claim, ensuring immediate costs are covered without depleting family liquid assets.

Document every detail in what The Paul Group calls a ‘Legacy Roadmap’. This document serves as a holistic reference point for all stakeholders, capturing the intersection of financial mechanics and personal legacy. It ensures that the transition from planning to execution is seamless when the time comes. This roadmap should include:

-

Beneficiary designations and contact protocols.

-

Policy numbers and carrier information.

-

Specific funeral or cremation preferences linked to the budget.

Conclude the session by proposing a collaborative consultation with a seasoned advisor to review the best final expense insurance for seniors. This next step moves the conversation from theory to a sustainable, professional solution tailored to your parents’ unique needs. It reinforces the idea that how to talk to parents about final expense planning is not just about the talk itself, but about the disciplined intervention that follows.

Overcoming Resistance and Strategic Objections

Understanding how to talk to parents about final expense planning requires a transition from emotional appeals to strategic analysis. Resistance often stems from a fundamental misunderstanding of asset liquidity. When parents claim they have sufficient savings, they’re typically overlooking the logistical hurdles of the probate process. National data indicates that settling an estate can take anywhere from 6 to 18 months. During this window, liquid cash is often inaccessible to beneficiaries. Final expense planning ensures that capital is deployed immediately, usually within 24 to 48 hours of a claim, bypassing the structural delays of traditional inheritance.

The perception of high cost is another barrier we must dismantle through strategic alignment. Many seniors view insurance as a monthly drain rather than a risk management tool. By presenting curated, simplified issue plans, you shift the focus toward the sustainable scaling of their legacy. These plans are designed for efficiency. They focus on the specific capital required for end-of-life logistics rather than bloated, unnecessary coverage. This isn’t an expense; it’s a strategic allocation of resources to protect the family’s broader financial ecosystem.

If the conversation leads to an emotional shutdown, the Wise Advisor knows when to pause. Pushing through a defensive wall often yields diminishing returns. Instead, validate their concerns. Acknowledge that their desire for independence is a strength. By stepping back, you preserve the partnership. You can revisit the topic later with fresh data, ensuring the process remains a collaborative evolution rather than a confrontation.

Common Hurdles in Senior Financial Planning

The "I’m not going anywhere yet" response requires a shift in perspective. Focus on the "if" of sudden incidents rather than the "when" of natural progression. It is about structural integrity, not mortality. You should also clarify the distinction between traditional life insurance and final expense optimization. While traditional policies often require rigorous medical exams, final expense products utilize simplified underwriting to ensure coverage for those with existing health profiles. This distinction is vital when discussing the pros and cons of final expense insurance for seniors.

The Role of Professional Third Parties

A shift in the child-parent power dynamic often requires a neutral, expert voice. Bringing in a strategic partner from The Paul Group removes the emotional friction inherent in these family discussions. We act as the Wise Advisor, validating your parents’ concerns while maintaining a disciplined focus on the objective. For families in California or Nevada, preparing for a joint call with a licensed agent provides a professional framework that replaces tension with clarity. This collaborative methodology ensures that the final plan is not a demand from a child, but a professional recommendation for the family’s long-term stability. Mastering how to talk to parents about final expense planning is easier when you have a seasoned partner to mediate the technical nuances.

Contact The Paul Group today to schedule a strategic consultation and bridge the gap between hesitation and legacy security.

From Dialogue to Implementation with The Paul Group

Mastering how to talk to parents about final expense planning represents a significant shift from avoidance to proactive leadership. This transition from abstract discussion to operational reality requires a partner who understands the high stakes of legacy protection. The Paul Group functions as a bespoke, commission-based brokerage; this structure ensures our strategic alignment remains with the family rather than a single carrier. This independence allows us to curate solutions from a diverse portfolio, optimizing for both cost efficiency and long-term structural integrity.

Our reach extends from the Pacific shores of Hawaii to the Atlantic coast of Florida, covering a vast demographic spectrum. This national footprint allows our advisors to navigate the specific regulatory nuances found across 16+ states while maintaining a unified standard of excellence. Families in 2026 face unique economic pressures, making immediate coverage options vital for instant financial relief. By securing a policy that activates upon the first premium payment, you eliminate the "waiting period" risk that often plagues mass-market insurance products. This immediate protection serves as a critical buffer against the unexpected, providing the peace of mind necessary to focus on family bonds.

A Partnership-Driven Approach

We view every engagement as a long-term alliance rather than a simple transaction. The Paul Group has specialized in senior legacy protection since 2009, providing fixed-rate solutions that require no medical examination. This methodology removes the technical friction of physical assessments, allowing seniors with complex health profiles to obtain coverage with dignity. Our Wise Advisors serve as the bridge between your family’s emotional needs and the technical requirements of the insurance market, ensuring every decision is rooted in data and empathy.

Your Next Strategic Move

Securing 2026 rates now provides a hedge against future market volatility and age-related premium increases. Leading your family through this process ensures that when the inevitable occurs, the focus remains on celebration rather than administrative or financial chaos. Requesting a curated quote tailored to your parent’s unique health profile is the logical next step in this journey toward total clarity. Secure your parents’ legacy with a professional final expense consultation today.

Securing a Legacy Through Strategic Dialogue

Navigating the complexities of legacy management requires a shift from emotional hesitation to disciplined execution. By applying a structured framework, you transform a potentially volatile discussion into a moment of strategic alignment. The objective remains clear: protecting family stability through proactive preparation rather than reactive crisis management. Mastery of how to talk to parents about final expense planning ensures that your family’s financial architecture remains resilient against future volatility. It’s a vital step toward long-term structural integrity.

Since 2009, The Paul Group has specialized exclusively in the senior market, providing the intellectual rigor necessary to navigate these sensitive transitions. We currently operate across 16 states, including Texas, California, and Florida, offering simplified issue plans that require no medical exams. This methodology removes the friction often associated with traditional insurance underwriting, allowing for a more streamlined optimization of your estate. Our group identity is built on delivering bespoke solutions that honor the unique DNA of every family we serve. Partner with The Paul Group to secure your family’s future today.

We’re ready to help you turn these complex challenges into a clear path forward. Let’s begin the work of building a more secure and predictable future together.

Frequently Asked Questions

Is it better to buy final expense insurance for my parents or have them buy it?

Ownership depends on who maintains the long-term financial obligation and legal control. While parents often own their policies, adult children can act as the policyholder if they demonstrate insurable interest under National Association of Insurance Commissioners guidelines. This strategy ensures the child maintains oversight of the premium schedule to prevent a lapse in coverage. Our methodology focuses on this structural alignment to protect the family’s legacy from administrative oversight.

What happens if my parents have pre-existing health conditions in 2026?

Parents with pre-existing conditions in 2026 still have access to coverage through guaranteed issue or graded benefit structures. These specialized instruments bypass traditional medical exams, though they typically include a 24-month waiting period for full benefit eligibility. The Paul Group utilizes a curated selection of carriers to ensure that even complex health histories don’t prevent a successful strategic alignment with your family’s needs.

Can I pay the premiums for my parents’ final expense policy?

You can certainly serve as the premium payer for your parents’ policy to ensure the plan remains in force. This arrangement is common when children initiate the process of how to talk to parents about final expense planning to stabilize the family’s future liabilities. Most carriers facilitate this through a third-party payer authorization, which provides a layer of financial security while keeping the parent as the insured individual.

How do funeral costs in California compare to states like Arizona?

Funeral costs in California are significantly higher than in Arizona, reflecting broader regional economic variances. According to 2023 National Funeral Directors Association reports, the median cost of a funeral with burial and viewing exceeded $8,300, while California metropolitan areas often see costs 15 percent higher than the national average. Arizona’s costs tend to align more closely with the national median, making geographic location a critical variable in your holistic planning.

What is the difference between burial insurance and a prepaid funeral plan?

Burial insurance provides a liquid cash benefit to beneficiaries, whereas a prepaid funeral plan locks in specific services with a single funeral home. Prepaid plans lack portability, which is a risk since 20 percent of retirees move to a different state after age 65 according to recent census data. Final expense insurance offers the flexibility to adapt to relocation or changing family preferences, providing a more resilient operational framework.

Is a medical exam required for the plans offered by The Paul Group?

The Paul Group specializes in simplified issue products that don’t require a physical medical exam or blood work. We employ an underwriting methodology that relies on a brief health questionnaire and digital pharmacy record checks to accelerate the approval process. This streamlined approach allows for rapid optimization of your coverage, often resulting in a policy decision within 24 hours of the initial application.

How quickly does a final expense policy pay out after a death?

Most final expense policies are engineered to pay out within 24 to 48 hours after the carrier receives and approves the death certificate. This rapid liquidity is essential for managing immediate obligations like transportation or cemetery fees that require prompt settlement. Our Group prioritizes carriers with a proven track record of claims efficiency to ensure that your strategic plan is executed without unnecessary delays.

Can final expense insurance be used for things other than a funeral?

Beneficiaries can use the tax-free death benefit for any purpose, including settling medical debts or covering outstanding utility bills. Understanding how to talk to parents about final expense planning involves recognizing that these funds provide a versatile safety net beyond the cemetery gates. In 2026, many families use these proceeds to clear credit card balances, which average over $6,000 for seniors according to recent Federal Reserve data.

Leave a Reply