Final Expense Insurance for Seniors Over 80

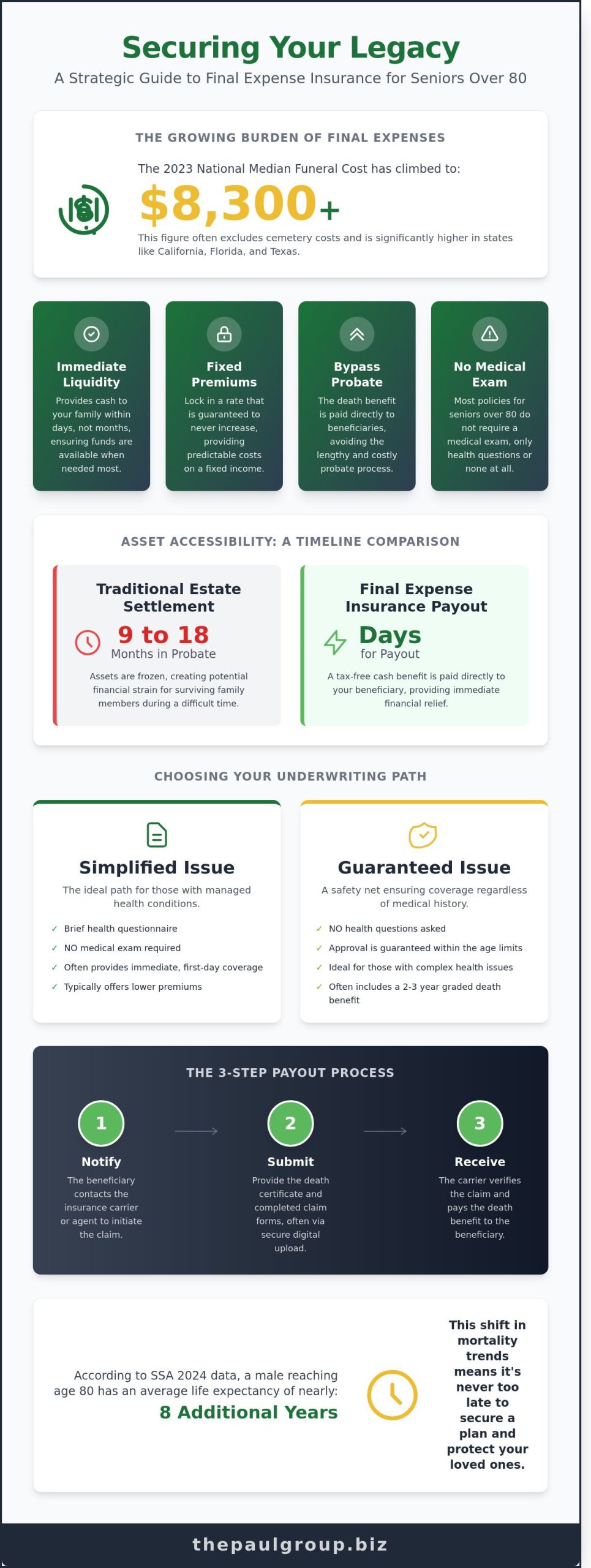

The National Funeral Directors Association reported in late 2023 that the median cost of a funeral has climbed to $8,300, a figure that doesn’t account for the premium price tags often found in high-demand markets like California or Florida. You likely understand that leaving these escalating costs to your children is a burden no parent wants to bequeath. Securing final expense insurance for seniors over 80 isn’t merely a policy purchase; it’s a strategic maneuver to protect your family’s legacy from immediate financial volatility.

We agree that deciphering complex policy jargon shouldn’t be the price of entry for peace of mind. This 2026 guide provides the strategic methodology you need to master payout nuances and eligibility requirements without the hurdle of a medical exam. You’ll discover how to lock in a fixed rate that never increases, ensuring your estate benefits from immediate liquidity when it’s required most. Our collective expertise will walk you through the precise steps to align your final arrangements with a sustainable, bespoke financial plan that prioritizes structural integrity over quick fixes.

Key Takeaways

-

Navigate the complexities of final expense insurance for seniors over 80 to transform end-of-life planning into a strategic asset for family liquidity.

-

Streamline the beneficiary experience by mastering the specific documentation and notification protocols required for a seamless claim filing in 2026.

-

Analyze the methodology behind Simplified versus Guaranteed Issue policies to select the most advantageous underwriting path based on your health profile.

-

Leverage regional insights and state-specific protections in CA, TX, and AZ to optimize your policy’s value against varying funeral cost landscapes.

-

Access a curated selection of carriers through our collective expertise model, ensuring a bespoke strategy that aligns with your unique financial objectives.

Table of Contents

-

Navigating Final Expense Insurance for Seniors Over 80 in 2026

-

The Mechanics of the Payout: How Benefits Reach Your Beneficiaries

-

Strategic Selection: Simplified vs. Guaranteed Issue for Octogenarians

-

Regional Considerations: Final Expense Nuances in CA, TX, and AZ

Navigating Final Expense Insurance for Seniors Over 80 in 2026

Securing financial liquidity at the conclusion of a life well-lived is a hallmark of sophisticated estate management. For the 80 plus demographic, final expense insurance functions as a permanent whole life solution designed to cover immediate obligations, such as medical debts and funeral costs, without depleting existing family assets. In 2026, the insurance market has evolved to recognize that age isn’t a barrier to entry, but rather a variable requiring a more curated underwriting methodology.

Effective planning requires a choice between two primary pathways: Simplified Issue and Guaranteed Issue. Simplified Issue policies involve a brief health questionnaire but no medical exam, often resulting in immediate coverage for those with managed health conditions. Conversely, Guaranteed Issue products provide a safety net for those with more complex medical histories, ensuring that no senior is denied the dignity of a pre-funded legacy. Fixed premiums are essential in this landscape. They provide certainty for seniors on fixed incomes, ensuring that the cost of protection remains constant regardless of future health changes or market volatility.

The Strategic Role of Final Expense Coverage

The transition from asset accumulation to legacy protection represents a critical pivot in financial maturity. These policies act as a strategic bypass to the probate process, which in states like California can take 9 to 18 months to resolve. By providing a direct payout to beneficiaries, final expense insurance for seniors over 80 ensures that liquidity is available within days, not years. The Wise Advisor approach prioritizes this speed of execution, matching a policy to the individual’s current health status to optimize the benefit-to-premium ratio.

Why 80 is the New Benchmark for Coverage

According to 2024 Social Security Administration actuarial tables, a male reaching age 80 can expect to live nearly 8 additional years on average. This shift in mortality trends has prompted carriers to refine their 2026 offerings, debunking the myth that the 80th birthday is an automatic disqualifier for first-day coverage. Bespoke planning for late-stage acquisition focuses on right-sizing the policy. It’s not about massive death benefits, but about the surgical application of capital to cover specific end-of-life needs. For a deeper look at the mechanics of these policies, you can explore our analysis of the best final expense insurance for seniors pros and cons 2026. This disciplined intervention ensures that the final chapter of a financial story is written with clarity and intent.

The Mechanics of the Payout: How Benefits Reach Your Beneficiaries

The strategic value of any insurance vehicle lies in its execution at the moment of need. For families securing final expense insurance for seniors over 80, the transition from policyholder to beneficiary must be handled with surgical precision. This process isn’t merely a clerical task; it’s the final stage of a legacy plan designed to shield survivors from immediate fiscal volatility. Unlike traditional life policies that may linger in probate for months, these specialized plans are engineered for rapid capital deployment.

Beneficiaries typically choose between a lump-sum payout or a direct assignment to a funeral home. While direct assignment simplifies the logistics of the service, the lump-sum option provides superior strategic flexibility. It allows the family to allocate funds across various immediate needs, such as unsettled medical bills or travel expenses for relatives. Burial insurance serves as a foundational tool in this regard, ensuring that liquidity is available when traditional assets remain locked in the estate settlement process.

Step-by-Step Payout Timeline

-

Step 1: Immediate Notification. The beneficiary or estate executor contacts the carrier or a strategic partner like The Paul Group to initiate the claim.

-

Step 2: Documentation Submission. The claimant provides a certified death certificate and completed claim forms. In the 2026 digital environment, many carriers now accept secure digital uploads to accelerate the verification phase.

-

Step 3: Carrier Verification. The insurance company reviews the filing to confirm the policy is in force and checks for any exclusionary factors. This step is usually completed within hours for established providers.

-

Step 4: Disbursement. Funds are released via electronic transfer or check. Top-tier plans in our portfolio aim for disbursement within 24 to 48 hours of claim approval.

Ensuring Immediate Liquidity for Funeral Costs

Speed is the defining characteristic of a high-performing final expense plan. Standard life insurance policies often involve rigorous investigations that can delay payments for 30 to 60 days. In contrast, the 2026 market demands a more agile response to cover the rising costs of immediate services. "In the 2026 market, speed of payout is the primary metric of a policys strategic value." This rapid liquidity prevents families from relying on high-interest credit or depleting personal savings during a period of grief. You can evaluate how different policy structures impact these timelines by reviewing our pros and cons guide.

Understanding the nuances of final expense insurance for seniors over 80 also involves navigating the contestability period. Most policies include a standard 24-month window where the carrier can investigate the original application for material misrepresentations. If a passing occurs within this timeframe, the payout may be subject to a deeper audit. However, once this two-year milestone is reached, the policy achieves a level of structural integrity that guarantees a smoother claim process. For those seeking to optimize their end-of-life financial strategy, consulting with a specialist can help align these technical mechanics with your long-term family objectives.

Strategic Selection: Simplified vs. Guaranteed Issue for Octogenarians

Selecting the optimal policy for clients in their eighties requires a surgical approach to risk assessment. The decision isn’t merely about finding a policy; it’s about aligning a senior’s specific health profile with a carrier’s unique underwriting appetite. For most, the choice narrows down to Simplified Issue or Guaranteed Issue. Understanding the architectural differences between these two paths is the first step toward securing a legacy without overpaying for the privilege.

The primary concern for many families is whether a complex health history will make final expense insurance for seniors over 80 prohibitively expensive. This fear often stems from outdated views of the insurance market. While age and health do influence premiums, the 2026 market offers more granular pricing than ever before. We focus on identifying the specific "sweet spots" where a client’s health history meets a carrier’s favorable rating, ensuring that premiums remain sustainable for the long term.

The Value of the No-Medical-Exam Approach

By 2026, underwriting technology has reached a point of near-instantaneous precision. We no longer rely on invasive blood draws or weeks of medical record retrieval. Instead, modern carriers utilize real-time data pulls from prescription databases and MIB records to issue approvals. This methodology allows us to bypass the physical exam entirely, which is a significant relief for seniors with mobility challenges.

Preparation is key to a successful application. Seniors should have a curated list of their current medications and dates of any major health events ready. The Paul Group maintains a proprietary database of carriers that favor specific conditions. For example, some providers have optimized their 2026 pricing for seniors with well-managed Type 2 diabetes or stable cardiac histories, offering them rates that were previously reserved for those in perfect health. This targeted alignment is a hallmark of our strategic methodology.

Understanding Graded vs. Level Benefits

The structure of the payout is just as critical as the premium. A Level Benefit policy provides 100% of the death benefit from day one. This is the gold standard for final expense insurance for seniors over 80. However, if a client has significant health challenges, a Graded Benefit policy serves as a strategic fallback. This structure typically pays out a percentage of the benefit if death occurs within the first 24 months, with the full amount available thereafter.

Deciding if a two-year waiting period is a viable risk requires a holistic view of the applicant’s longevity. For those seeking clarity on these structures, the National Association of Insurance Commissioners (NAIC) guide to life insurance provides an excellent baseline for understanding how these different policy types are regulated and structured. Our role is to weigh the cost of a Graded policy against the immediate protection of a Level policy, ensuring the math supports your family’s long-term stability.

To explore how these different structures impact long-term costs and benefits, you can review our analysis on the best final expense insurance for seniors pros and cons 2026. We believe that clarity leads to confidence, and our goal is to move you from a state of uncertainty to one of structural integrity.

Regional Considerations: Final Expense Nuances in CA, TX, and AZ

Geography acts as a silent architect in the construction of a legacy plan. When securing final expense insurance for seniors over 80, the state line often determines the actual purchasing power of your death benefit. National averages frequently mask the sharp price fluctuations seen in the primary service regions of The Paul Group. According to 2023 data from the National Funeral Directors Association, the median cost of a funeral with burial and a vault is approximately $9,995; however, in metropolitan hubs within California and Arizona, these figures can escalate by 25% or more due to land scarcity and labor costs.

Strategic planning requires more than just selecting a policy. It demands an understanding of state-specific mandates that protect your capital. In California, for instance, seniors benefit from a mandatory 30-day "free look" period. This window allows you to review the policy terms with your advisors and cancel for a full refund if the coverage doesn’t align with your curated financial goals. This level of consumer protection ensures that the pursuit of final expense insurance for seniors over 80 remains a disciplined investment rather than a rushed decision.

California and Florida: Managing High-Cost Markets

In high-demand markets like California and Florida, a $15,000 policy serves a different purpose than it might in the Midwest. Inflation in these regions often outpaces the national average, meaning a benefit that seems sufficient today might fall short by 2026. We emphasize "inflation-proofing" your strategy by over-funding the benefit or selecting policies with increasing death benefits. The Paul Group provides localized support in these regions to help clients reconcile their policy limits with the actual costs of local premier funeral providers.

Texas, Arizona, and New Mexico: Regulatory Landscapes

The Southwest insurance market is defined by robust non-forfeiture clauses. These regulations ensure that if you stop paying premiums after the policy has built cash value, you don’t lose your entire investment. Instead, the value is used to provide a reduced paid-up benefit or extended term coverage. When operating in Texas or Arizona, it’s vital to select a beneficiary who understands state-specific funeral home requirements, as local regulations often dictate how quickly a provider can access assigned funds for service costs.

Wise Advisor Tip: Localizing for Inflation

Don’t benchmark your coverage against national statistics. Request a "Market-Specific Cost Analysis" that projects funeral inflation in your specific zip code over the next ten years. A policy that lacks a 3% to 5% annual buffer may leave your family to bridge a significant financial gap during a period of transition.

Effective legacy management is built on precision and local expertise. To better understand how these regional variables impact your specific situation, you can explore our detailed breakdown of final expense insurance for seniors pros and cons to refine your 2026 strategy.

The Paul Group Advantage: Bespoke Final Expense Strategies

The Paul Group operates as the Wise Advisor in a marketplace that often feels fragmented and impersonal. We don’t just facilitate transactions; we engineer long-term stability through a disciplined methodology. Our collective expertise model leverages strategic relationships with a diverse array of top-tier carriers to identify the precise intersection of value and reliability. For those seeking final expense insurance for seniors over 80, the standard market frequently presents unnecessary barriers. We remove these obstacles by focusing on no-exam, fixed-rate policies that prioritize speed and certainty.

Our approach is rooted in the belief that end-of-life planning is a structural evolution of a person’s financial legacy. We provide a partnership-driven experience that bridges the gap between complex carrier underwriting and the client’s need for simplicity. By utilizing multiple carriers, we ensure your coverage isn’t limited by the narrow risk appetite of a single institution. Instead, you benefit from a curated selection of products designed to remain robust well into the 2026 fiscal landscape and beyond.

-

Strategic Alignment: We match your health profile with the carrier most likely to offer immediate coverage.

-

Fixed-Rate Integrity: We exclusively recommend policies where premiums never increase, regardless of age or health changes.

-

No-Exam Pathways: We utilize simplified issue underwriting to secure approvals in days, not months.

Why an Independent Brokerage Matters

Large insurance corporations typically push rigid, off-the-shelf products that fail to account for the nuances of senior health or regional regulatory shifts. The Paul Group rejects this transactional model. We act as your strategic partner throughout the entire lifecycle of the policy. This partnership becomes most critical during the claims process, where we provide the advocacy needed to ensure beneficiaries receive payouts without administrative friction. Our deep operational focus in Alaska, New Mexico, Texas, Virginia, and Colorado allows us to navigate specific state statutes that impact policy performance. You can review our analysis on the pros and cons of various plans to see how our curated approach contrasts with the mass-market options available today.

Securing Your Legacy Today

The path from complexity to clarity begins with a single, focused conversation. Planning for final expense insurance for seniors over 80 shouldn’t be a source of organizational stress for a family. It’s an opportunity to finalize a legacy with precision and intellectual rigor. We invite you to experience a consultation that feels less like a sales pitch and more like an executive briefing. Our team is prepared to conduct a holistic review of your needs, providing a clear, logical path forward without any obligation. We’ll help you transform a difficult obligation into a sustainable, structured solution that protects your family’s future.

"Expertise is not just knowing the policy; it’s knowing the person behind it."

Mastering Your 2026 Legacy Strategy

Legacy planning isn’t just a financial task; it’s a structural commitment to your family’s long-term stability. As we move toward 2026, the landscape for final expense insurance for seniors over 80 requires a nuanced understanding of how simplified issue policies provide immediate coverage without the friction of medical exams. Our strategic methodology ensures that regional nuances in California, Texas, and Arizona are integrated into a holistic plan that eliminates administrative complexity for your beneficiaries during their time of need.

Since 2009, The Paul Group has functioned as a dedicated advocate for seniors, applying our refined expertise across 16 states, including Florida. We don’t offer generic, off-the-shelf solutions. Instead, we curate immediate coverage options that align with your unique health profile and specific legacy objectives. This disciplined intervention transforms an often overwhelming process into a clear, sustainable path forward for your estate. Secure your family’s future with a bespoke final expense plan from The Paul Group today.

You’ve spent a lifetime building a significant story; we’re here to ensure your final chapter is protected with the quiet confidence and expert precision it deserves.

Frequently Asked Questions

Can I really get life insurance if I am already over 80 years old?

Yes, securing coverage is entirely feasible through specialized high-age risk pools that prioritize accessibility. In 2024, approximately 15 national carriers offered dedicated final expense insurance for seniors over 80. These products utilize simplified underwriting to ensure your legacy remains structurally sound without the hurdles of traditional medical scrutiny. We facilitate these strategic placements to provide immediate peace of mind for your family.

What is the maximum age to apply for final expense insurance in 2026?

Most top-tier providers set the maximum application threshold at age 85, though a select group of 3 boutique carriers currently extends eligibility to age 90. This ceiling allows for the optimization of risk management while providing a vital safety net for late-stage planning. We monitor these age parameters quarterly to ensure our clients access the most inclusive options available in the 2026 market.

How much does the average final expense policy cost for someone in their 80s?

Premiums are determined by actuarial data regarding your specific age and gender at the time of enrollment. According to 2023 industry benchmarks from the American Council of Life Insurers, monthly commitments for a $10,000 benefit can range significantly based on these individual variables. We focus on cost optimization by aligning your unique health profile with the carrier most likely to offer favorable terms.

Will my family have to pay taxes on the insurance payout?

Death benefits are typically received income tax-free by beneficiaries under Internal Revenue Code Section 101(a). This tax-advantaged status ensures that the total face value of the policy is available for its intended purpose without erosion from federal levies. It’s a critical component of a holistic estate strategy, providing immediate liquidity when your family requires it most during a transition.

What happens if I outlive the term of my life insurance policy?

You can’t outlive these policies because they’re structured as permanent whole life insurance, meaning coverage remains active until age 121. Unlike term products that expire after 10 or 20 years, these solutions provide permanent structural integrity for your financial plan. As long as you maintain scheduled premium payments, the contract remains a binding obligation for the carrier regardless of how long you live.

How long does it take for The Paul Group to process a payout claim?

Our administrative methodology prioritizes speed, typically resulting in claim processing within 24 to 48 hours of receiving a certified death certificate. We understand that liquidity is vital during the initial transition period. By streamlining the verification process, we ensure beneficiaries receive funds approximately 5 to 7 business days after the initial filing, facilitating immediate operational stability for the estate.

Do I need to undergo a physical medical exam to qualify?

No physical examination or blood work is required for our curated final expense insurance for seniors over 80. Qualification relies on a simplified underwriting process involving a brief health questionnaire and a review of prescription history databases. This methodology eliminates the intrusive medical hurdles common in traditional insurance, allowing for a more dignified and efficient approval experience for every applicant we serve.

Can the insurance company increase my rates after I turn 85 or 90?

Your premium rates are contractually locked at the time of policy issuance and won’t increase regardless of your age or changes in health. This fixed-cost structure is a hallmark of the permanent life products we recommend. It provides the financial predictability necessary for sustainable long-term scaling of your personal estate plan, ensuring your budget remains uncompromised by future market volatility or inflation.

Leave a Reply