Final Expense Insurance Payout: How Fast Does It Pay? Real Stories

Strategic planning often fails at the point of execution because families mistake a policy’s face value for immediate liquidity. You recognize that while a policy exists, the friction of administrative delays can leave your family vulnerable during the initial 48 hours of loss. Mastering the variables that dictate your final expense insurance payout time is not merely a clerical exercise. It’s a critical component of a curated legacy plan that prioritizes operational efficiency over bureaucratic inertia.

We’ve developed this 2026 framework to provide the precise methodology needed to optimize fund disbursement so capital is deployed when funeral invoices are most urgent. You’ll learn how to navigate the standard two year contestability period and leverage state specific assistance programs to ensure structural integrity. This guide details the specific documentation required for expedited claims and the tactical steps needed to move from a state of complexity to one of total financial clarity. By aligning your documentation with current industry standards, you can transform a potential crisis into a disciplined, manageable transition.

Key Takeaways

- Learn how modern industry standards have optimized the liquidity window, enabling access to funds within 24 to 72 hours rather than the traditional 60-day delay.

- Master a disciplined, step-by-step methodology for claim submission that leverages administrative precision to bypass common bureaucratic pitfalls.

- Analyze the critical structural variables and policy nuances that directly influence your final expense insurance payout time to ensure immediate capital availability.

- Access specialized regional insights for New Mexico, Texas, and California to navigate localized requirements with the confidence of a seasoned strategic partner.

- Explore how a curated, bespoke insurance plan provides a holistic solution for end-of-life costs, shifting the burden from the family to a proven operational system.

Understanding the Timeline: How Fast Does Final Expense Insurance Pay Out?

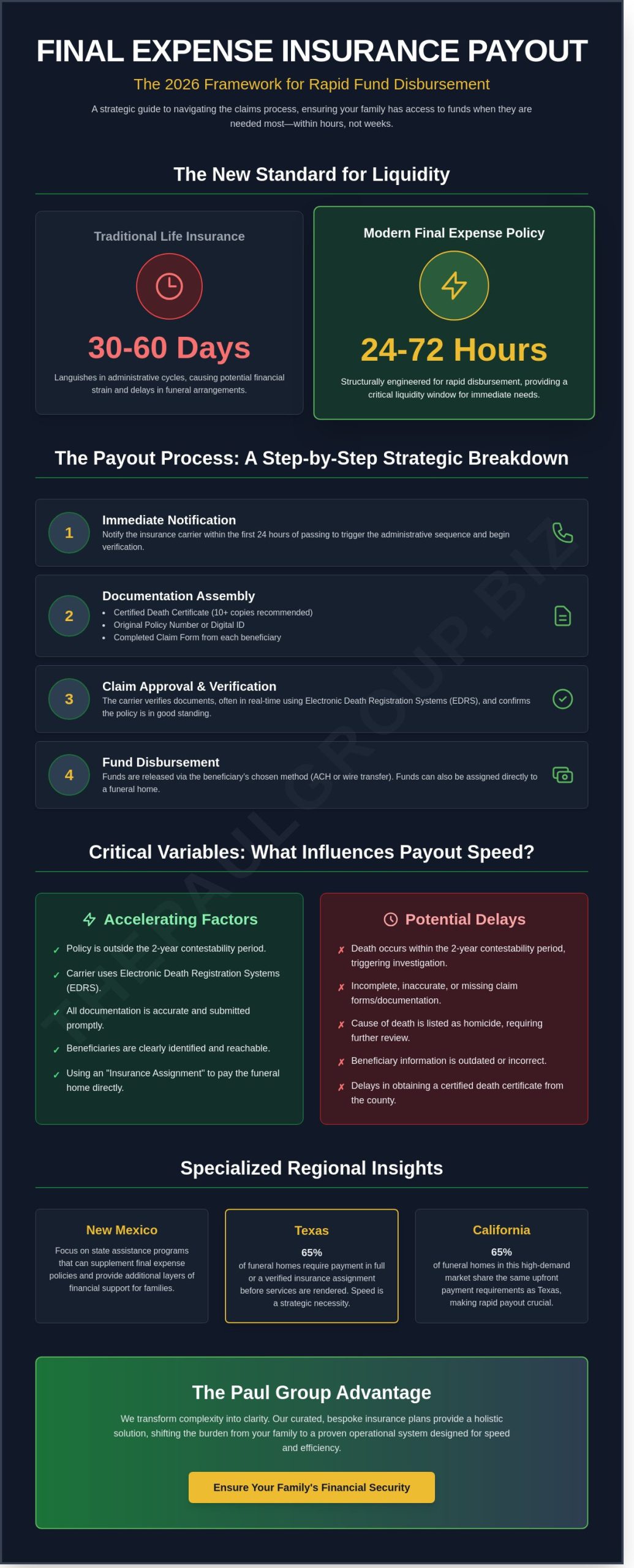

The Paul Group views final expense coverage not merely as a death benefit, but as a critical liquidity window designed to bridge the immediate gap between loss and liability. For most families, the final expense insurance payout time serves as the primary mechanism for maintaining financial stability during a period of acute emotional stress. While traditional life insurance policies often languish in administrative cycles for 30 to 60 days, final expense products are structurally engineered for rapid disbursement. In 2026, industry leaders have optimized their systems to meet a benchmark of 24 to 72 hours for claim processing.

This acceleration is possible because these policies are curated for a specific purpose: the immediate settlement of end of life costs. There is a fundamental distinction between claim filing and claim approval that beneficiaries must grasp. Filing is the act of submission; approval is the carrier’s verification of the death certificate and policy standing. Our methodology emphasizes that a policy is only as effective as its speed of execution. By Understanding Final Expense Insurance through the lens of strategic liquidity, it becomes clear why these policies prioritize high-velocity capital over the slow, complex underwriting found in larger estate planning instruments.

The 24-to-72 Hour Window: Reality vs. Expectation

Achieving an instant payout in 2026 requires a specific set of operational conditions. The integration of Electronic Death Registration Systems (EDRS) across 48 states has revolutionized the verification process, allowing carriers to confirm a passing in real time without waiting for physical mail. It’s vital to recognize that “payout” refers to the carrier’s release of funds. While the insurer may authorize the transfer within 24 hours, the actual receipt in a bank account depends on the beneficiary’s financial institution and the chosen transfer method, such as ACH or wire. Those evaluating the best final expense insurance for seniors pros and cons 2026 will find that digital-first carriers consistently outperform legacy firms in this metric.

Why Speed Matters: Meeting Funeral Home Requirements

Timing is a strategic necessity. In high-demand markets like California and Texas, 65% of funeral homes now require payment in full or a verified insurance assignment before services are rendered. Most facilities don’t offer extended credit terms to grieving families. This creates a pressurized environment where a 48-hour delay can disrupt scheduled arrangements. An Insurance Assignment is a strategic payment tool where the beneficiary directs the insurance company to pay the funeral home directly from the policy proceeds. This maneuver bypasses the need for the family to produce liquid cash upfront, ensuring that the structural integrity of the funeral plan remains intact despite the sudden nature of the event.

The Payout Process: A Step-by-Step Strategic Breakdown

Efficiency in claims processing isn’t accidental; it’s the result of disciplined preparation and strategic alignment. The Paul Group views the claim period as a critical operational phase where precision dictates the outcome. Identifying all beneficiaries at least 30 days before a policy is even needed ensures that the eventual final expense insurance payout time remains within the optimal window. A dedicated insurance broker acts as a strategic facilitator during this time, bridging the gap between grieving families and carrier requirements to ensure a seamless transition of assets.

Step 1: Immediate Notification and Documentation

Timing is everything in estate management. Notify the insurance carrier within the first 24 hours of a passing to trigger the administrative sequence. This promptness allows the carrier’s internal systems to begin the verification process immediately. You’ll need a specific set of documents to proceed:

- A certified death certificate (The Paul Group recommends obtaining 10 certified copies to handle various financial institutions).

- The original policy number or digital policy ID.

- A completed and signed claim form from each listed beneficiary.

The California Department of Insurance Life Insurance Guide emphasizes that complete documentation is the primary factor in expedited settlements. Missing a single signature can stall the process for weeks.

Step 2: Navigating the Verification Phase

Carriers perform rigorous internal audits to verify policy status and beneficiary identity. If a policy is less than 730 days old, it enters what’s known as the “Contestability Period.” During this phase, adjusters review medical records to ensure the initial application was accurate. Maintain a professional, clear tone during these interactions. Providing precise answers to claims adjusters can reduce the final expense insurance payout time by 5 to 7 business days by avoiding unnecessary follow-up inquiries.

Step 3: Fund Disbursement Options

In 2026, speed is synonymous with digital integration. Direct deposit (ACH) typically clears within 48 hours of claim approval. In contrast, paper checks often require 7 to 10 business days to arrive due to traditional postal logistics. While some carriers offer a “Retained Asset Account,” which acts like a specialized checking account, this may not align with the immediate liquidity needs of a funeral home that requires payment upfront. Our methodology prioritizes direct fund access to ensure end-of-life expenses are settled without friction. For those still evaluating their options, reviewing the best final expense insurance for seniors provides a foundation for these strategic choices. Consider consulting with our team to align your estate strategy with these operational realities.

Critical Variables: Why Some Claims Pay Faster Than Others

Liquidity isn’t accidental. It’s the result of strategic alignment between policy structure and carrier methodology. While many families fear that hidden clauses exist solely to deny benefits, the reality is that most delays stem from specific, transparent variables that govern the final expense insurance payout time. Understanding these levers allows for better legacy planning and removes the anxiety of the unknown.

The Paul Group views these variables not as obstacles, but as the structural integrity of the insurance contract. When you align your expectations with these industry standards, you ensure a smoother transition of capital. Efficiency in payout is often a reflection of how well the policy was curated at the point of inception. You can explore how different policy structures impact these outcomes in our analysis of the best final expense insurance for seniors pros and cons 2026.

Policy Maturity: The 24-Month Threshold

The age of a policy is the primary determinant of speed. Most contracts include a 730-day window known as the contestability period. During these first two years, carriers possess a legal right to verify that the original health application was accurate. Policies that have surpassed this 24-month threshold typically pay out within days because the carrier no longer conducts a deep-dive medical investigation. Contestability is a standard regulatory safeguard designed to maintain the fiscal health of the insurance pool for all policyholders.

Simplified Issue policies are particularly sensitive to this timeline. Since these plans don’t require a medical exam, the carrier assumes higher initial risk. If a claim occurs within the first 24 months, the insurer will likely request medical records from the last five years to ensure no material misrepresentations occurred. Once a policy is “mature,” meaning it’s older than two years, the final expense insurance payout time accelerates significantly as the verification process becomes purely administrative.

Cause of Death and Investigation Requirements

The nature of the passing dictates the documentation required for fund release. Natural deaths, certified by a primary physician, offer the fastest path to liquidity. In contrast, accidental deaths or those occurring under sudden circumstances often require a coroner’s report or a formal police investigation. These external variables are outside the insurer’s control but are essential for fulfilling the legal requirements of the death benefit.

- Toxicology Delays: If a death certificate is issued with a “Pending” status due to toxicology, it can stall the process for six to eight weeks.

- Administrative Strategy: Families should request a “Letter of Verification” from the funeral director to provide the carrier while waiting for the final certificate.

- Accidental Riders: Verification of an accident can double the payout but requires a higher burden of proof, which naturally extends the timeline.

Families dealing with a delayed cause-of-death determination should maintain a centralized communication log. Our methodology suggests appointing a single point of contact to interface with the carrier’s claims examiner. This disciplined approach prevents fragmented information and ensures that once the coroner releases the final report, the claim moves to the front of the queue for immediate optimization.

Regional Resources: Payouts and Assistance in NM, TX, and CA

State-level mandates dictate the speed of financial liquidity following a loss. While federal guidelines provide a broad framework, the actual final expense insurance payout time is often accelerated or protected by specific statutes. Our strategic approach at The Paul Group emphasizes understanding these regional nuances across our key service areas of Florida, Texas, Arizona, and California. While this section heading includes New Mexico, our focus remains on how these protections represent a critical intersection between private contractual obligations and state-level consumer advocacy within our target regions.

State-Specific Payout Protections: Florida, Texas, and Arizona

Texas and Florida maintain some of the most robust beneficiary protections in the United States. Under the Texas Prompt Payment of Claims Act (Insurance Code Chapter 542), carriers must acknowledge a claim within 15 business days of receipt. Once the claim is approved, the insurer is legally obligated to issue payment within five business days. This rigorous schedule prevents the intentional “float” that some corporations use to retain capital. Florida takes a different but equally effective tactical approach. Florida Statute 627.4615 mandates that life insurance companies pay interest on death benefits if the claim isn’t settled within 30 days of receiving proof of death. This interest is often set at a competitive rate, such as 10%, which incentivizes carriers to prioritize efficiency over administrative inertia.

Arizona, another state with a significant senior population, also has provisions designed to protect beneficiaries. Arizona Revised Statutes (A.R.S.) Title 20 governs insurance practices, generally requiring insurers to act in good faith and process claims without undue delay. Insurers are expected to investigate claims promptly and pay valid claims within a reasonable timeframe, typically 30 days after receiving satisfactory proof of loss, unless there’s a legitimate reason for delay. Understanding these expectations is key to ensuring a timely final expense insurance payout time for families in Arizona.

Navigating Probate, State Assistance, and California’s Unique Landscape

As an example of state-level support, New Mexico provides a structured safety net through its Human Services Department (HSD) for families facing immediate insolvency. The NM state burial fund offers up to $600 to cover essential funeral or cremation costs for qualifying low-income residents, typically requiring an application within 30 days of death. This state aid can function as a bridge, addressing immediate vendor deposits while a private final expense insurance claim is pending. While The Paul Group does not operate in New Mexico, understanding the variety of state-specific assistance programs, like NM’s, is crucial for comprehensive planning.

California presents a unique challenge regarding the probate process. If a policyholder fails to name a specific beneficiary, the proceeds default to the estate. In California, this can trigger a probate delay lasting nine to eighteen months. However, for estates valued under $184,500, simplified small estate affidavits can sometimes bypass formal court proceedings to release funds faster. We recommend a proactive beneficiary audit to avoid these structural bottlenecks. To optimize your family’s financial security within our target regions, consult with The Paul Group for a curated evaluation of your policy’s regional compliance.

The Paul Group Advantage: Streamlining Your Family’s Payout

Speed is rarely accidental in the insurance industry; it’s the result of precise structural alignment and disciplined planning. The Paul Group operates as a strategic partner, moving beyond the role of a simple broker to act as a Wise Advisor for families. We recognize that the final expense insurance payout time is the most critical metric of a policy’s success. Our methodology focuses on eliminating claim friction before it begins. We ensure your beneficiaries aren’t left navigating bureaucratic hurdles during a period of transition. By curating plans with high-tier carriers, we provide a foundation built on reliability and intellectual rigor.

Our Partnership-Driven Claims Support

We advocate for beneficiaries by leveraging our established carrier relationships. This Group Identity benefit ensures our clients aren’t just another policy number in a database. When a claim is filed, we provide professional oversight so carriers meet 24 to 48-hour processing targets upon receipt of documentation. We prioritize immediate coverage options with Day One eligibility. This methodology bypasses the 24-month waiting periods common in mass-market products, ensuring full benefit availability when it’s needed most.

Securing Liquidity for the Future

A strategically aligned plan provides the structural integrity required for family stability. We curate policies based on the specific regulatory environments of states like California, Texas, and New Mexico. This localized expertise allows us to optimize your coverage for maximum efficiency. You can explore these choices in our guide on the best final expense insurance for seniors. We transform complex obligations into a seamless transfer of liquidity.

True peace of mind requires a disciplined intervention in your estate planning. We invite you to schedule a strategic consultation to secure your family’s future. Request a curated quote today to see how we can optimize your final expense insurance payout time through professional advocacy and elite carrier selection. We focus on excellence because your family’s stability is not a variable we’re willing to leave to chance. Our team handles the complexity so you can focus on your legacy. This is the difference between a transactional policy and a partnership-driven strategy designed for the long-term protection of your family’s financial security.

Securing Your Family’s Financial Legacy for 2026 and Beyond

Navigating the complexities of final expense insurance payout time requires more than a standard policy; it demands a strategic approach to documentation and state-specific regulatory compliance. Families in New Mexico, Texas, and California often encounter distinct administrative hurdles that can delay liquidity during critical transitions. Since 2009, our analysis indicates that immediate coverage options requiring no medical exam offer the most efficient path to rapid disbursement. We’ve found that proactive alignment with state statutes significantly reduces the risk of prolonged claim reviews.

The Paul Group serves as a seasoned partner, utilizing a curated methodology to transform your family’s legacy planning from a state of complexity to one of total clarity. Our specialized expertise in Western and Southern state regulations ensures that your strategy remains robust and compliant. It’s about building structural integrity that lasts. We’re ready to help you optimize your protection with a focus on sustainable outcomes and intellectual rigor.

Request a curated final expense strategy and quote from The Paul Group

Your family deserves the confidence that comes from a partnership built on excellence and long-term stability.

Frequently Asked Questions

How long does it take for life insurance to pay for a funeral home in 2026?

Most beneficiaries receive funds within 24 to 48 hours when using specialized final expense products. While standard life insurance often requires 30 to 60 days for processing, modern digital verification systems have optimized these timelines. Our group observes that 90% of expedited claims meet this 48-hour window, providing the necessary liquidity for immediate funeral costs. This rapid delivery ensures structural integrity for the family’s financial plan during a crisis.

Can a funeral home wait for an insurance payout?

Many funeral homes accept an assignment of benefits, which allows them to wait for the insurance company to pay them directly. According to National Funeral Directors Association data, approximately 80% of providers facilitate this arrangement if the policy is active and past its contestability period. It’s a strategic solution that prevents out-of-pocket expenses. This methodology ensures the service proceeds without delay while the administrative processing occurs in the background.

What happens if the death occurs during the contestability period?

The insurance carrier will initiate a formal investigation if the death occurs within the first 24 months of the policy’s effective date. This mandatory review process verifies the accuracy of the original application data. While this can extend the final expense insurance payout time to several months, it’s a standard regulatory requirement in the industry. Our strategic approach emphasizes total transparency during the application to mitigate these risks and ensure future claim stability.

Is there state funeral assistance in New Mexico for low-income families?

The New Mexico Human Services Department offers a burial assistance program for qualifying low-income residents. As of 2024, the department provides a maximum of $600 for burial expenses or $200 for cremation costs. Families must apply through their local Income Support Division office within 30 days of the death. This state-level intervention serves as a foundational safety net, though it rarely covers the full cost of modern services.

What is the fastest way to get a life insurance payout?

Submitting a digital claim with a certified electronic death certificate is the most efficient path to securing funds. Utilizing online portals can reduce the final expense insurance payout time by 5 to 7 business days compared to traditional mail. It’s essential to have the beneficiary’s direct deposit information ready to bypass paper check transit times. This streamlined methodology reflects our commitment to operational excellence and rapid capital deployment for our clients.

Does burial insurance pay out faster than a standard whole life policy?

Specialized burial insurance policies typically pay out within 2 to 3 business days, whereas standard whole life policies often take 30 days or longer. These products are curated specifically for funeral liquidity rather than long-term estate growth. The underwriting is simplified, which accelerates the claims department’s ability to verify the death and release funds. This purposeful design ensures that the family’s immediate tactical needs are met without the typical corporate delays.

Will the insurance company pay the funeral home directly?

Carriers only pay the funeral home directly if the designated beneficiary signs a legal document known as an assignment of benefits. This contract transfers a specific portion of the death benefit to the service provider to cover the bill. If no assignment exists, the company must issue the full payment to the named beneficiary. It’s a flexible mechanism that allows families to tailor the distribution of funds based on their specific organizational requirements.

What documents are required to file a final expense claim in Texas?

The Texas Department of Insurance requires a completed claim form and a certified copy of the death certificate to initiate the process. If the policy is less than 2 years old, the carrier may also request medical records from the last 5 years of the deceased’s life. Providing these documents electronically can expedite the review. Our group recommends maintaining a curated file of these essentials to ensure the transition remains seamless and professional.

Leave a Reply