End of Life Insurance for Seniors: What to Know Before It’s Too Late

With the National Funeral Directors Association reporting that the median cost of a funeral with burial now frequently exceeds $10,000, the financial weight of a legacy shouldn’t become a burden for those you leave behind. You’ve worked hard to establish structural integrity in your financial life; it’s only natural to feel concerned about rising costs or the potential for health-based declines. Securing end of life insurance for seniors represents a strategic alignment between your current retirement budget and your long-term estate goals.

At The Paul Group, we believe that clarity is the foundation of peace of mind. This guide provides a curated methodology for identifying immediate coverage options that bypass traditional medical hurdles. You’ll discover how to transform a complex transition into a seamless, well-funded plan that protects your family’s stability. We’ll examine the specific insurance structures available in 2026, helping you choose a bespoke solution that honors your life’s work without compromising your current lifestyle. By focusing on sustainable scaling and holistic planning, we ensure your final expenses are handled with the same excellence you’ve applied to every other aspect of your life.

Key Takeaways

-

Identify how specialized permanent policies mitigate the rising $10,000+ burden of modern funeral costs through fixed premiums and guaranteed death benefits.

-

Navigate state-regulated frameworks to secure end of life insurance for seniors, utilizing specific mandates to protect your financial legacy from predatory market practices.

-

Evaluate the critical nuances between simplified and guaranteed issue underwriting to determine the most efficient path for your unique health profile and age.

-

Apply a curated strategic framework to compare insurance carriers and resolve eligibility concerns for those initiating coverage as late as age 80.

-

Discover why The Paul Group’s bespoke methodology offers superior structural integrity and partnership compared to the transactional approach of high-volume call centers.

Table of Contents

-

Understanding End of Life Insurance for Seniors: A Strategic Necessity

-

The Architecture of Final Expense Coverage: How These Plans Function

-

Navigating State Regulated Life Insurance Programs in California and Beyond

-

Evaluating Your Options: A Framework for Senior Financial Security

Understanding End of Life Insurance for Seniors: A Strategic Necessity

Final expense planning requires a shift from speculative investment to structural preservation. Specialized permanent life insurance, frequently categorized under the broader umbrella of Understanding End of Life Insurance, serves as the cornerstone of this methodology. Unlike traditional policies designed for income replacement during high-earning years, end of life insurance for seniors focuses on the immediate liquidity required to settle a decedent’s estate. The Paul Group views this not as a mere purchase, but as a structural optimization of an individual’s final footprint.

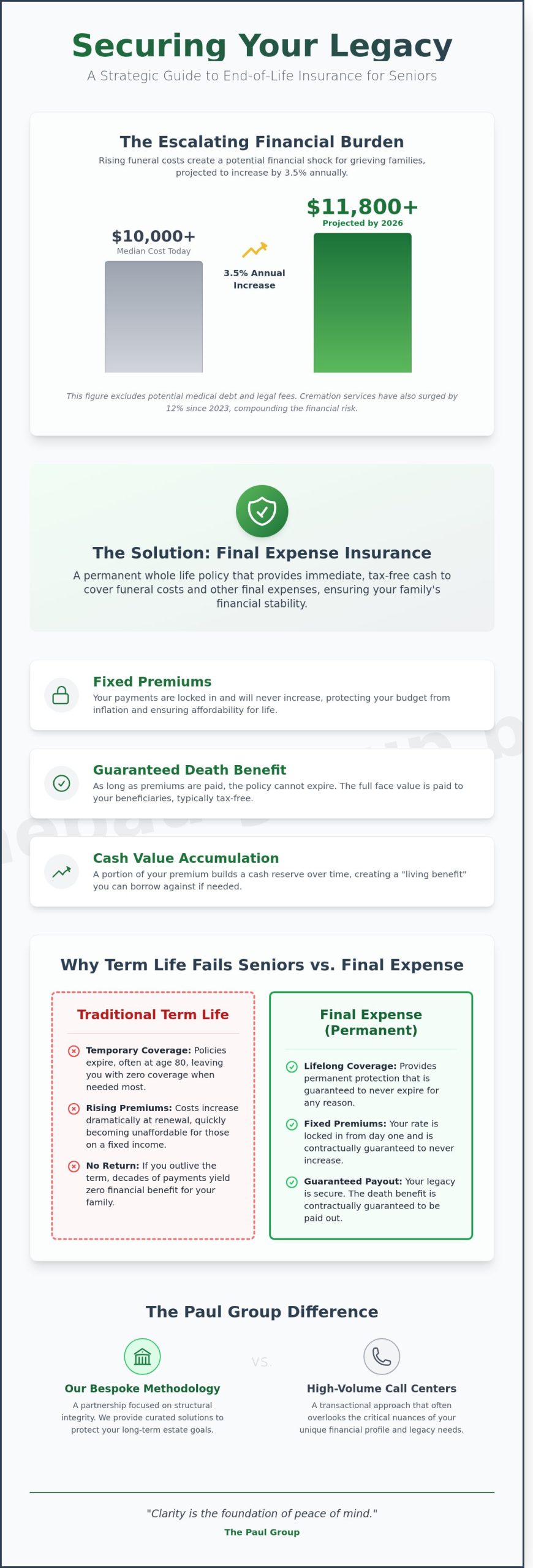

The objective is clear. We aim to mitigate the $10,000 to $15,000 financial shock often associated with modern funeral services. Traditional term life insurance frequently fails those over age 65 because these policies are built on temporary risk windows. These windows often expire before the need for a payout arises. When a policy lapses at age 80, the previous decades of premium payments yield zero return, creating a strategic gap in a family’s financial defense. Permanent coverage ensures that the intersection of human legacy and operational financial systems remains intact, regardless of when the transition occurs.

A sophisticated approach to end of life insurance for seniors recognizes that death is not just a personal event; it’s a complex financial transaction. This specialized coverage offers:

-

Fixed Premiums: Costs remain static, resisting the inflation that erodes other assets.

-

Cash Value Accumulation: A holistic benefit that provides a small, accessible reserve if needed.

-

Guaranteed Payouts: Assurance that the policy will remain active as long as premiums are met.

The Escalating Costs of Final Expenses in 2026

Data from the last two fiscal years indicates a steady 3.5% annual increase in funeral industry fees. By 2026, a standard burial with a viewing and vault frequently exceeds $11,800. This figure excludes the medical debt and legal settlement costs that often surface during probate. Cremation services have also seen a price surge of 12% since 2023. Final expense insurance serves as a strategic tool for debt prevention by insulating the estate from immediate, high-interest liabilities.

Why Seniors Prioritize This Coverage

Surviving spouses often face a sudden liquidity crisis when pension payments or Social Security checks are adjusted downward. This coverage provides a curated safety net, ensuring a dignified farewell without forcing the liquidation of long-term family savings. The psychological benefit of "Wise Advisor" planning transforms a period of grief into a period of orderly transition. Seniors who utilize the best final expense insurance for seniors methodology find peace in knowing their legacy is secure and their family is protected from unnecessary financial strain.

The Architecture of Final Expense Coverage: How These Plans Function

Effective end of life insurance for seniors operates as a permanent financial instrument, distinct from the temporary nature of term policies. These plans utilize a whole life chassis, ensuring that coverage remains in force for the duration of the policyholder’s life. This structural permanence is supported by fixed premiums and a guaranteed death benefit. Unlike other insurance models, these policies accumulate cash value over time. This internal reserve acts as a stabilizing force, providing a layer of liquidity that reinforces the policy’s long-term viability. It’s a system designed for endurance rather than short-term gain.

Strategic planning requires a look at the market’s leading options. When selecting a carrier, consulting a list of top-rated burial insurance providers allows for a comparison of financial strength ratings and claim-settlement histories. This data-driven approach ensures the selected vehicle can withstand market fluctuations over several decades, protecting the beneficiary’s interests against corporate insolvency.

Underwriting Without the Physical Exam

Modern underwriting has shifted toward efficiency. Simplified issue policies rely on comprehensive health questionnaires and real-time database queries rather than invasive physical exams. For the 70% of seniors who manage chronic but stable conditions, this methodology offers a strategic advantage: immediate full-benefit coverage. In contrast, those with more complex medical histories may utilize a graded death benefit. This structure typically provides a partial payout if the insured passes away within the first 24 months; it balances risk for the carrier while securing a path to full protection. Understanding the best final expense insurance for seniors pros and cons 2026 helps in determining which underwriting path aligns with your specific health profile.

Fixed Rates and Permanent Protection

Predictability is the cornerstone of senior financial security. Most end of life insurance for seniors features level premiums that never increase, regardless of age or health changes. This is vital for the 15% of retirees who rely solely on Social Security for their monthly income. These non-cancelable clauses prevent the policy from being revoked as long as premiums are paid. To maintain the policy’s efficacy, face values should be strategically aligned with projected inflation. With the Consumer Price Index for elderly consumers often outpacing general inflation, a policy purchased today must account for the rising costs of services expected in 2030 or beyond.

Core Pillars of Policy Stability:

-

Non-Cancelable Clauses: Protection against carrier-initiated termination.

-

Level Premiums: Shielding fixed budgets from rising insurance costs.

-

Cash Value Growth: Building a tax-deferred asset within the policy.

-

Immediate Vesting: Access to full death benefits from day one for qualified applicants.

The Paul Group provides the strategic framework necessary to ensure your legacy remains structurally sound and operationally efficient.

Navigating State Regulated Life Insurance Programs in California and Beyond

The regulatory landscape for end of life insurance for seniors is defined by its lack of uniformity. Each state operates as a sovereign domain of consumer protection, creating a patchwork of mandates that require sophisticated navigation. The Paul Group views these regional variations not as administrative hurdles, but as a framework for building secure, localized financial structures. Our methodology prioritizes a holistic understanding of state-specific statutes to ensure that every policy remains compliant and protective of the policyholder’s interests.

Effective planning requires an acknowledgment that a strategy successful in one jurisdiction may falter in another due to varying oversight levels. We believe that clarity is the foundation of confidence. By aligning individual needs with the specific legal requirements of their home state, we transform a complex procurement process into a disciplined strategic alignment.

California-Specific Protections for Seniors

California maintains one of the most robust regulatory environments in the United States. The California Department of Insurance (CDI) provides rigorous oversight for the more than 1,400 insurance companies licensed to operate within the state. This oversight is vital for maintaining the integrity of state regulated life insurance programs in California. These programs serve as a critical consumer safety net, ensuring that products marketed to older adults meet high standards of transparency and fairness.

A cornerstone of CA protection is the mandatory 30-day "Free Look" period for residents aged 60 and older. This provision, established under California Insurance Code Section 10127.10, allows seniors to review their policy documents and cancel for a full refund within the first month. It’s a mechanism that prevents high-pressure sales tactics from creating long-term financial burdens. Our advisors utilize this window to conduct a secondary audit of the policy’s fit within the client’s broader estate plan.

Cross-State Strategic Planning

The modern senior often maintains a multi-state footprint, perhaps splitting the year between Arizona and New Mexico. This mobility introduces complexity into end of life insurance for seniors, as the cost of final services varies significantly by geography. For instance, while the average cost of a traditional funeral in Texas centers around $7,500, urban centers in Florida often see these expenses climb toward $9,000. As individuals assess their specific financial trajectories, determining is burial insurance right for you? remains a foundational step in the planning process.

The Paul Group addresses these regional nuances through a multi-state methodology. We maintain licensing across 15+ states, allowing us to curate coverage that accounts for local inflation rates and funeral cost volatility. When evaluating the best final expense insurance for seniors, we consider the logistical reality of where the policy will eventually be executed. This level of detail ensures that the death benefit isn’t just a number, but a precisely engineered solution for the specific costs of a chosen region. Our approach provides a seamless transition of protection, regardless of where our clients choose to call home.

Evaluating Your Options: A Framework for Senior Financial Security

Selecting end of life insurance for seniors requires a shift from emotional decision-making to disciplined financial analysis. This isn’t merely an expense; it’s a strategic asset designed to insulate your family from sudden liquidity needs. A robust evaluation framework ensures that your choice aligns with your long-term estate goals rather than short-term marketing promises. Precision in selection prevents the common pitfall of overpaying for restrictive coverage.

When vetting carriers, use this curated checklist to maintain high standards of structural integrity:

-

Credit Rating: Only consider carriers with an A.M. Best rating of ‘A’ or higher to ensure long-term solvency.

-

Premium Stability: Verify that premiums are contractually guaranteed to remain level for the life of the policy.

-

Benefit Structure: Distinguish between day-one coverage and graded benefit periods, which often last 24 months.

A frequent objection we encounter is whether age 80 is a terminal threshold for new policies. It isn’t. According to 2023 Social Security Administration actuarial tables, an 80-year-old male has an average life expectancy of over 8 years. This window provides ample time for a policy to mature, provided you understand the trade-off. At this stage, premium costs are higher, yet the immediate death benefit offers a certainty that self-funding cannot match. You can learn about the best final expense insurance for seniors pros and cons 2026 to see how these timelines impact your specific strategy.

Comparing Simplified Issue to Traditional Whole Life

Simplified issue policies prioritize speed. They often bypass medical exams and rely on a health questionnaire. This efficiency comes at a cost, typically reflected in premium loading for high-risk individuals. Traditional whole life offers deeper medical investigation which can result in lower costs for those who qualify. Avoid "burial schemes" that lead with low-cost teasers; these often hide aggressive "step-up" clauses that increase premiums as you age.

Overcoming Common Obstacles to Coverage

Chronic conditions like Diabetes or Heart Disease don’t stop the planning process. They simply require a more nuanced carrier selection. Rather than paying from monthly cash flow, many seniors fund these premiums through strategic asset reallocation. Moving funds from a low-interest 1.5% savings account into a permanent policy converts a taxable asset into a tax-free benefit. This Wise Advisor approach ensures your end of life insurance for seniors functions as a holistic part of your financial DNA. It’s about optimization, not just protection.

Connect with our expert team to build your bespoke final expense strategy today.

The Paul Group Methodology: Curated Final Expense Solutions

Policy selection is an exercise in strategic precision. At The Paul Group, we reject the transactional nature of high-volume call centers, opting instead for a methodology rooted in bespoke quality and intellectual rigor. Our structural integrity is supported by a robust network of carriers across 15 states, ensuring that every recommendation aligns with long-term stability rather than short-term convenience. We understand that end of life insurance for seniors is not a commodity; it’s a fundamental pillar of a legacy plan that requires careful execution. Our commitment to excellence ensures that your most complex planning challenges are met with disciplined intervention and visionary leadership.

The Paul Group Advantage for Seniors

Our firm brings over 20 years of specialized focus to the final expense sector. We employ a Wise Advisor process that mandates a thorough diagnosis of your financial and health profile before any solution is prescribed. This disciplined intervention allows us to facilitate applications with a focus on maximum approval rates, effectively navigating the complexities of medical underwriting. We don’t just provide a policy; we engineer a sustainable outcome that protects your family’s future. Our methodology focuses on the intersection of human needs and operational systems, framing your planning as an opportunity for structural evolution within your estate.

-

Holistic Diagnostics: We evaluate the intersection of health history and budgetary constraints to find the optimal fit.

-

Carrier Optimization: Our 15-state network allows us to match your profile with the most favorable actuarial tables available in 2026.

-

Operational Excellence: We manage the bureaucratic friction of the application process to ensure immediate peace of mind for your beneficiaries.

Next Steps: Securing Your Strategic Alignment

Achieving clarity in your estate planning requires a partner who values substance over hyperbole. You can secure your family’s future with a curated final expense plan from The Paul Group. Our agents are motivated by your long-term stability, providing the professional guidance necessary to transform a complex organizational challenge into a solved problem. By requesting a bespoke quote tailored to your specific health profile, you initiate a process of strategic alignment that guarantees results. We take the necessary time to diagnose your specific needs before prescribing a path forward, ensuring the rhythm of your planning is never rushed.

The path to securing end of life insurance for seniors is simplified through our structured briefing style. We guide you from initial complexity to ultimate clarity, providing a grounded, substance-heavy presence that feels like a conversation held in a boardroom. For more detailed insights on how these plans function, you may explore the best final expense insurance for seniors pros and cons 2026 to understand how our methodology outperforms standard market offerings. Your legacy deserves the precision of a seasoned strategic partner who values excellence above all else.

Securing Your Legacy Through Strategic Financial Alignment

Strategic alignment between your current financial posture and future legacy requirements demands more than a generic policy; it requires a methodology rooted in intellectual rigor. Since 2009, The Paul Group has facilitated this transformation for families across 15+ states, including California, Texas, and Florida. By leveraging partnerships with A+ rated carriers, we move beyond transactional coverage to create curated solutions that ensure long-term stability. Navigating the nuances of end of life insurance for seniors shouldn’t be a solitary endeavor. It’s a complex organizational challenge for any household, yet it’s entirely solvable through disciplined intervention and expert guidance. Your family’s structural integrity depends on the decisions you make today. We invite you to move from complexity to clarity with a partner who values excellence as much as you do. It’s time to replace uncertainty with a definitive roadmap.

Request Your Bespoke Final Expense Consultation with The Paul Group

You’ve worked hard to build your life, and we’re here to help you protect it with the dignity it deserves.

Frequently Asked Questions

What exactly does "state regulated" mean for life insurance in California?

State regulated means the policy strictly adheres to the California Insurance Code, which is overseen by the California Department of Insurance (CDI). This regulatory framework ensures that carriers maintain high solvency standards and follow ethical claims practices. The CDI manages over 1,400 insurance entities to protect consumers, providing the structural integrity required for your end of life insurance for seniors. It’s a layer of security that guarantees the firm’s ability to meet its long term obligations.

Can I get end-of-life insurance if I have a chronic health condition?

You can secure coverage despite chronic conditions by utilizing guaranteed issue or simplified issue policies. These products bypass traditional medical exams, focusing instead on a streamlined health questionnaire. Since 85% of adults aged 65 and older manage at least one chronic condition according to the CDC, the industry has developed specific risk-assessment models to accommodate these health profiles. This approach ensures that health history isn’t a barrier to strategic final expense planning.

Is there a waiting period before the full death benefit is active?

A waiting period, often spanning 24 months, applies specifically to guaranteed issue policies where medical underwriting is absent. If the insured passes away during this initial two year window from non-accidental causes, the carrier typically returns the paid premiums plus 10% interest. For those who qualify for level benefit plans through health screening, the full death benefit is active from the first day the policy is in force. It’s a transparent trade-off between medical disclosure and immediate coverage.

How much end-of-life insurance does a typical senior actually need?

Most seniors require between $10,000 and $25,000 to cover comprehensive final obligations. The National Funeral Directors Association (NFDA) reported in 2023 that the median cost of a funeral with viewing and burial reached $8,122. Strategic planning should also account for an additional $3,000 to $5,000 for ancillary costs like headstones, flowers, and outstanding medical bills. This ensures a debt-free transition for the family, preventing the burden of unexpected financial liabilities during a time of grief.

What is the difference between burial insurance and final expense insurance?

Burial insurance and final expense insurance are synonymous terms used to describe small whole life insurance policies tailored for end of life insurance for seniors. While the terminology varies, the structural mechanism remains the same. Both provide a cash payout to beneficiaries, who then have the autonomy to allocate funds for cremation, burial, or legal fees as they see fit. The distinction is purely a matter of marketing nomenclature rather than a difference in the underlying contract’s utility.

Will my monthly premiums increase as I get older?

Your monthly premiums won’t increase because these policies are structured as permanent whole life insurance. Once the carrier issues the contract, your rate is locked in for the duration of your life. This fixed-cost model provides the fiscal stability necessary for long-term retirement planning, ensuring that your coverage remains affordable even as inflation impacts other sectors of the economy. It’s a predictable expense that allows for precise budgetary optimization over several decades.

Do I need a lawyer to set up a final expense insurance policy?

You don’t need a lawyer to establish a final expense policy, as the application process is managed directly through licensed insurance advisors. The policy acts as a private contract that bypasses probate, delivering funds directly to your named beneficiaries. While a lawyer is essential for drafting a formal will or trust, the insurance mechanism itself is designed for rapid, administrative efficiency. It’s a streamlined tool for wealth transfer that functions independently of complex legal proceedings.

How does the insurance company pay out the benefit to my family?

The insurance company issues the death benefit as a tax-free lump sum payment directly to your designated beneficiaries. Most carriers prioritize these claims, often releasing funds within 24 to 72 hours of receiving a certified death certificate. This liquidity allows families to manage immediate expenses without liquidating other assets or waiting for the lengthy probate process to conclude. It’s a strategic intervention that provides immediate financial clarity during a complex organizational transition for the estate.

Leave a Reply