Burial Insurance for Seniors Over 80

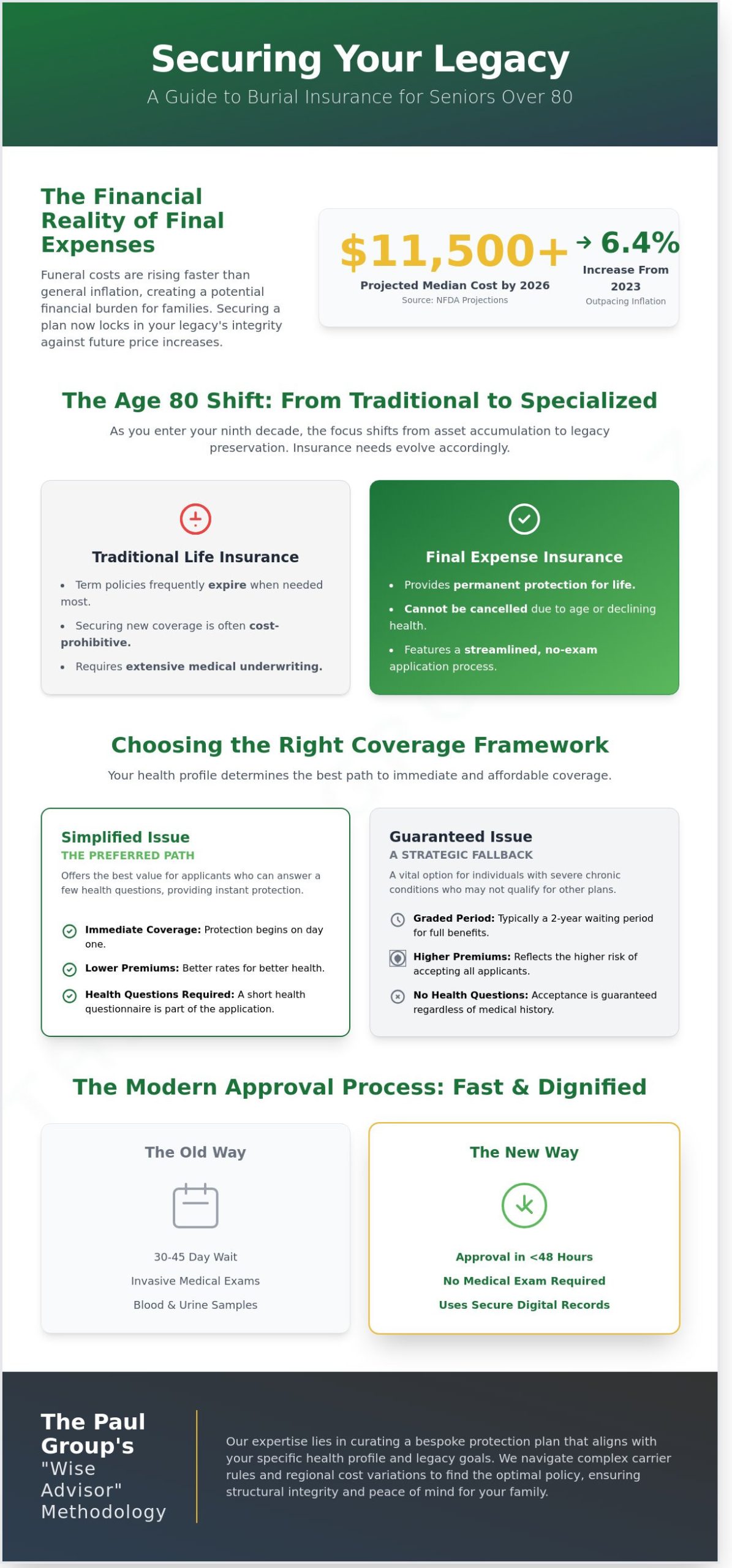

By 2026, the National Funeral Directors Association projects the median cost of a funeral will exceed $11,500, a 6.4% increase from 2023 data. This economic shift often creates a sense of urgency for families who value structural integrity in their long-term planning. You likely believe that your legacy should be a source of strength, not a financial complication for your heirs. At the Group, we understand that securing burial insurance for seniors over 80 requires a curated approach that prioritizes both speed and certainty.

You’ll discover how to obtain sophisticated, no-exam coverage that locks in fixed monthly rates for life. Protection shouldn’t be complicated. Our methodology focuses on identifying policies that offer immediate protection and rapid payouts to beneficiaries. We’ll examine the strategic alignment of final expense plans that eliminate the confusion of waiting periods, providing a clear, logical path forward for your estate.

Key Takeaways

-

Identify why age 80 represents a critical strategic inflection point in estate planning, necessitating a transition toward specialized final expense frameworks.

-

Master the distinction between Simplified and Guaranteed Issue underwriting to secure the most advantageous coverage class based on your health profile.

-

Analyze the premium economics of burial insurance for seniors over 80 to optimize the balance between immediate security and long-term value.

-

Navigate regional regulatory mandates and cost-of-living variables across 16 states to ensure your coverage aligns with local funeral industry trends.

-

Explore The Paul Group’s "Wise Advisor" methodology for curating a bespoke protection plan that prioritizes structural integrity and family legacy.

Table of Contents

-

The Strategic Significance of Burial Insurance for Seniors Over 80

-

Evaluating Coverage Frameworks: Simplified vs. Guaranteed Issue

-

The Economics of Final Expense: Rates and Value Optimization

-

The Paul Group Methodology: Curated Protection for Your Legacy

The Strategic Significance of Burial Insurance for Seniors Over 80

Age 80 marks a distinct transition in estate architecture. For many, the focus shifts from the aggressive accumulation of assets to the precision-based optimization of final liquidity. Burial insurance for seniors over 80 serves as a specialized financial instrument designed to address this specific need. It’s not a broad-market product; it’s a curated solution for final obligations that ensures the structural integrity of a legacy remains uncompromised by immediate costs.

These policies operate under a "Simplified Issue" framework. This methodology allows applicants to bypass the intrusive medical examinations that typically disqualify older individuals from standard coverage. By focusing on a series of health questions rather than lab work or physical exams, the application process aligns with the urgency often required at this stage of life. This shift represents a move toward certainty, providing a guaranteed payout that isn’t subject to the volatility of the market or the rigors of traditional underwriting.

Why Traditional Life Insurance Fails the 80+ Demographic

Traditional life insurance products often reach a forced conclusion just when they’re needed most. Term policies, which may have served a family for 20 or 30 years, frequently expire once the policyholder enters their ninth decade. Attempting to secure a new, medical-exam-based policy at 81 or 82 is often cost-prohibitive. This is where final expense insurance provides a necessary pivot. It offers permanent protection that can’t be cancelled due to age or declining health. For those seeking the best final expense insurance for seniors, the goal is to secure a policy that remains in force as long as premiums are paid, regardless of future medical diagnoses.

The Evolving Landscape of Funeral Costs in 2026

The economic environment of 2026 presents unique challenges for end-of-life planning. Data from the National Funeral Directors Association indicates that the median cost of a funeral has increased steadily, often outpacing general inflation by 2.5% to 3.2% annually over the last decade. Securing burial insurance for seniors over 80 provides the necessary liquidity to meet these rising expenses without liquidating other family assets. Burial insurance is a permanent contract with level premiums and a guaranteed death benefit.

Utilizing this tool ensures that the financial burden of a service doesn’t fall on surviving family members. It acts as a strategic hedge against future service cost increases. By locking in a premium today, the policyholder guarantees that their final arrangements are funded with yesterday’s dollars. This disciplined approach to final expense planning transforms a potential family crisis into a managed transition.

Evaluating Coverage Frameworks: Simplified vs. Guaranteed Issue

The Paul Group applies a rigorous methodology to secure burial insurance for seniors over 80. We prioritize the least restrictive underwriting class available to each individual. This strategic alignment ensures that clients don’t overpay for risk they don’t carry. Simplified Issue remains the gold standard. It offers immediate, first-day coverage for those who can navigate a brief health questionnaire. Conversely, Guaranteed Acceptance serves as a strategic fallback. It’s reserved for those with severe chronic conditions where traditional underwriting isn’t viable. Carriers have different intellectual philosophies regarding risk. Some view a minor heart event from January 2024 as a disqualifier, while others see it as a manageable historical data point.

The Advantage of No-Medical-Exam Underwriting

Modern underwriting has undergone a digital transformation. We no longer rely on invasive blood draws or physical examinations that once delayed approvals for 30 to 45 days. Today, carriers utilize data-driven algorithms to analyze prescription histories and Medical Information Bureau records in real-time. This methodology accelerates the process. Many of our clients move from initial application to policy activation in under 48 hours. This efficiency maintains client dignity. It eliminates the stress of clinical visits, replacing them with a streamlined, non-invasive conversation.

Qualifying with Pre-Existing Conditions

Navigating health markers like high blood pressure or type 2 diabetes requires a Wise Advisor who understands carrier-specific nuances. For instance, a senior managed on Metformin for 10 years is viewed differently by a boutique carrier than by a mass-market conglomerate. When Comparing the Best Burial Insurance Companies, the distinction often lies in how they weight specific conditions like congestive heart failure or recent stroke history.

The Paul Group facilitates the application process by pre-screening these variables against a curated list of carriers. This structural approach minimizes the risk of decline. It ensures that burial insurance for seniors over 80 is placed with the most favorable provider. Our team views these health challenges as opportunities for structural evolution in a client’s financial plan. If you’re seeking a disciplined intervention for your final expense needs, our advisors can help you optimize your selection through a bespoke coverage strategy.

The Economics of Final Expense: Rates and Value Optimization

The actuarial math for applicants between ages 80 and 90 is precise. At this stage, premium structures reflect a compressed timeline, making the efficiency of every dollar paramount. Waiting even six months to secure a policy can result in a 12% to 15% increase in monthly costs due to the higher age bracket and potential health shifts. This "cost of waiting" isn’t merely a calculation of higher premiums; it’s the risk of losing access to level benefits entirely. Strategic alignment requires matching the face amount to realistic 2026 projections. With the median cost of a funeral expected to exceed $11,500 by 2026, a $15,000 policy provides the necessary liquidity to cover service fees, transport, and administrative costs without burdening the estate.

Immediate Coverage vs. Two-Year Waiting Periods

The first 24 months of a policy are the most strategically sensitive. For burial insurance for seniors over 80, the distinction between a level benefit and a graded benefit determines when the full protection is active. Securing first-day coverage at age 85 is possible if the applicant can attest to the absence of high-risk conditions like congestive heart failure or recent strokes. If a claim occurs during a graded period, carriers typically return all paid premiums plus an additional 10% interest. Regulatory oversight by the National Association of Insurance Commissioners ensures these contracts remain transparent, and tools like the Life Insurance Policy Locator help beneficiaries manage these assets effectively. The Paul Group prioritizes level benefits to ensure immediate peace of mind.

Maximizing Policy ROI for the Beneficiary

Maximizing the return on investment involves a cold analysis of total premiums paid against the guaranteed death benefit. For many seniors, the goal is to ensure that the payout significantly outweighs the cumulative cost of the policy. Fixed rates are essential here. Because most seniors live on a disciplined, fixed income, any fluctuation in premium costs could jeopardize the entire plan. A permanent whole life structure ensures the rate never increases and the policy never expires. It’s a stable anchor in a volatile economic climate. For a deeper look at how these structures compare, you can review our detailed analysis of the pros and cons of final expense insurance. This methodology ensures that burial insurance for seniors over 80 functions as a predictable financial tool rather than a speculative expense. We focus on structural integrity so the family receives the intended value without delay.

Regional Regulatory Landscapes: From California to Florida

Navigating the jurisdictional nuances of the American insurance market requires more than a cursory understanding of policy language. It demands a rigorous, state-by-state analytical framework. The Paul Group maintains a strategic presence across 16 states, ensuring that burial insurance for seniors over 80 is optimized for local regulatory environments. This multi-state methodology allows us to synchronize high-level strategy with the specific mandates of individual state insurance departments, providing a level of consistency that transactional agencies cannot replicate.

Regional economic factors significantly influence the efficacy of a final expense plan. Data from the 2023 National Funeral Directors Association (NFDA) report indicates the national median cost for a funeral with burial reached $8,300. However, in high-volume hubs like Dallas, Houston, and Los Angeles, these costs often escalate by 18% to 22% due to local real estate and labor markets. We don’t ignore these variances. Our advisors utilize localized data to ensure your coverage amount aligns with actual market conditions in the Southwest and the Sun Belt.

-

Strategic alignment with state-specific insurance codes prevents administrative friction during the claims process.

-

Bespoke policy riders, such as accelerated death benefits, are curated based on the legislative allowances of your home state.

-

Consolidated oversight across 16 states ensures that families moving between regions maintain seamless service and structural integrity in their planning.

Focus on Texas and California: High-Volume Strategic Markets

The regulatory environments in Texas and California offer robust consumer protections that require expert interpretation. California’s Insurance Code 10113.71, for instance, mandates a 60-day grace period for policy lapses, a critical safeguard for senior policyholders. In Texas, the market’s scale demands a partner who understands the pricing bifurcations between metroplexes like DFW and rural counties. We leverage our deep Western and Southwestern roots to navigate these complexities, ensuring your plan remains compliant and competitive.

Florida and Arizona: Tailored Solutions for Retirement Communities

Florida and Arizona present unique demographic challenges, with Florida’s senior population exceeding 21% according to 2020 Census data. In these active retirement corridors, the availability of simplified issue policies often hinges on state-specific underwriting thresholds. Our methodology focuses on these retirement hubs, identifying carriers that offer the most favorable terms for burial insurance for seniors over 80. We prioritize a partner-driven approach, transforming complex state regulations into clear, actionable financial security.

Analyze your options with precision. Explore our comprehensive guide to final expense insurance pros and cons to determine which regional strategy fits your family’s needs.

The Paul Group Methodology: Curated Protection for Your Legacy

Securing a legacy for individuals in their ninth decade isn’t a task for generalists. It requires a partner-driven approach that prioritizes long-term stability over short-term sales targets. At The Paul Group, we’ve spent the last 15 years refining a methodology that treats final expense planning as a disciplined executive function. We don’t view burial insurance for seniors over 80 as a mere product; it’s a strategic alignment of resources designed to provide structural clarity for your family’s future.

Our "Wise Advisor" model applies intellectual rigor to the complexities of the insurance market. Since 2009, we’ve successfully guided thousands of families through the nuances of risk assessment and carrier selection. This extensive tenure allows us to bypass the trial-and-error phase common with less experienced brokers. We know which carriers have the underwriting appetite for specific age-related health profiles, ensuring your application moves from submission to approval with minimal friction. Before you commit to a plan, it’s helpful to weigh the pros and cons of final expense insurance to understand how it fits into your broader financial architecture.

A Collective of Diverse Insurance Experts

We function as a collective of specialists rather than a siloed agency. This group identity provides our clients with a distinct strategic advantage. By representing multiple top-tier carriers, we maintain the independence necessary to offer truly bespoke solutions. Our consultants focus on the intersection of human empathy and operational excellence. We recognize the emotional weight of these decisions, yet we address them with the calm, focused presence of a boardroom briefing. This balance ensures your concerns are heard while your organizational challenges are solved through precise, data-backed intervention. Our group identity means you aren’t just getting an agent; you’re gaining access to a deep repository of industry intelligence.

-

Strategic Independence: Access to a curated portfolio of top-rated insurers rather than a single-carrier bias.

-

Proven Tenure: Over 15 years of specialized market data and placement experience since our founding in 2009.

-

Holistic Methodology: A review process that prioritizes your unique health profile to ensure sustainable scaling of your coverage.

Securing Your Consultation

Moving from complexity to clarity begins with a single, streamlined interaction. Our process is designed to be frictionless, respecting both your time and your objectives. During your initial strategic briefing, an agent will conduct a thorough diagnosis of your needs. We’ll identify the most robust options for burial insurance for seniors over 80, tailoring each recommendation to your unique health profile and estate goals. You won’t find high-pressure tactics here; instead, you’ll find a logical path forward built on substance and transparency. We take the time to diagnose before we prescribe, ensuring that the final solution provides the structural integrity your legacy deserves.

Schedule your legacy protection review with The Paul Group today.

Architecting a Legacy of Stability and Precision

Navigating the complexities of final expense planning requires a disciplined methodology rather than a reactive approach. Securing burial insurance for seniors over 80 isn’t merely a financial transaction; it’s a strategic alignment of your legacy with long-term structural integrity. By evaluating simplified versus guaranteed issue frameworks, you ensure that your coverage is specifically engineered for your health profile. It’s about transforming a period of uncertainty into a state of absolute clarity for your loved ones.

The Paul Group has refined this process since 2009, bringing a specialized focus to senior final expense across 16 states including California, Texas, Florida, and Arizona. Our curated methodology offers high-level protection without the requirement of a medical exam, ensuring that your transition into a secured plan is both efficient and dignified. We prioritize holistic solutions that respect the unique DNA of your family’s needs while adhering to rigorous regional regulatory standards. You don’t have to manage these intricate organizational challenges alone when a seasoned strategic partner is ready to assist.

Secure your family’s future with a bespoke burial insurance plan from The Paul Group.

We look forward to helping you build a foundation of lasting peace and institutional order for the next generation.

Frequently Asked Questions

Is it possible to get burial insurance at age 85?

Yes, securing burial insurance for seniors over 80 remains a viable strategic option through age 85 with several specialized carriers. While the market narrows at this advanced stage, our methodology identifies specific providers that maintain eligibility for individuals until their 90th birthday. These policies prioritize accessibility, ensuring that legacy protection remains a curated reality rather than a structural impossibility for your family.

What is the maximum coverage amount for seniors over 80?

Most carriers cap the maximum death benefit between $25,000 and $40,000 for applicants in this demographic. This upper limit is designed to align with the National Funeral Directors Association 2023 report showing median funeral costs around $8,300. By selecting a bespoke coverage level within these parameters, you ensure a holistic solution that covers both immediate final expenses and residual administrative debts without overextending your monthly budget.

How much does burial insurance cost for an 80-year-old in 2026?

Pricing for burial insurance for seniors over 80 is determined by actuarial risk assessments rather than a flat fee structure. Industry benchmarks from 2024 suggest that a healthy 80-year-old male might anticipate monthly premiums ranging from $150 to $250 for a $10,000 policy. These figures reflect the increased mortality risk associated with advanced age and the necessity for carriers to maintain long-term solvency while providing guaranteed liquidity to your beneficiaries.

Do I need a physical exam to qualify for burial insurance?

You don’t need to undergo a physical medical examination to qualify for most final expense policies. Carriers utilize a simplified underwriting process that relies on a brief health questionnaire and a digital review of your prescription history. This methodology accelerates the approval timeline, often resulting in a policy offer within 24 to 48 hours of your initial application submission. It’s a streamlined approach designed for efficiency and respect for your time.

What is the difference between burial insurance and a pre-paid funeral plan?

Burial insurance provides a tax-free cash benefit directly to your beneficiaries, whereas a pre-paid plan is a contractual agreement with a specific funeral home. The insurance model offers superior financial flexibility, as the funds aren’t locked into a single service provider. This strategic distinction allows your family to optimize the payout for any urgent need, including medical bills or travel expenses, rather than being restricted to a pre-defined list of funeral goods.

Can my children pay the premiums for my burial insurance policy?

Your children or other family members can absolutely serve as the primary payers for your policy premiums. This arrangement is a common component of a collaborative family legacy strategy, allowing the next generation to secure their own financial stability by funding the protection today. Most carriers require the insured individual to provide consent, but the technical execution of payments can be handled by any authorized third party through automated bank drafts.

How quickly does the death benefit pay out to my family?

Beneficiaries typically receive the death benefit within 24 to 72 hours once the carrier approves the completed claim and death certificate. This rapid liquidity is a core value proposition of final expense planning, as it prevents the need for families to deplete their personal savings or high-interest credit lines. Our group prioritizes carriers with a proven track record of operational efficiency to ensure this transition is handled with professional urgency and care.

Are the monthly rates guaranteed to stay the same for life?

Your monthly premiums are contractually guaranteed to remain level for the entire duration of the policy. Unlike term insurance which expires or increases in cost, these whole life structures provide permanent price stability regardless of changes in your health or the broader economic environment. This predictability is essential for seniors on fixed incomes, ensuring that your strategic financial alignment isn’t disrupted by future market volatility or inflationary pressures.

Leave a Reply