Strategic Guide to Borrowing Against a Final Expense Insurance Policy in Florida, Illinois (2026)

What if the legacy you’ve built for tomorrow could serve as a strategic liquidity tool to solve the financial constraints you face today? For many residents in Florida and Illinois, the 12 percent increase in specialized home repair costs reported in early 2026 creates immediate pressures that traditional credit markets often fail to address. Understanding the nuances of borrowing against a final expense insurance policy is essential for those who view their policy as a sacred commitment but require a sophisticated solution for current cash flow. It’s natural to feel that accessing these funds might jeopardize your family’s future security.

This guide illustrates how to access capital for urgent needs while maintaining the structural integrity of your long-term plan. The Paul Group examines the specific mechanics of cash value loans within the current regulatory landscape to provide you with a clear path forward. You’ll discover a precise methodology for balancing immediate cash requirements with the preservation of a robust death benefit, ensuring your strategic alignment remains intact.

Understanding the Cash Value Mechanism in Final Expense Insurance

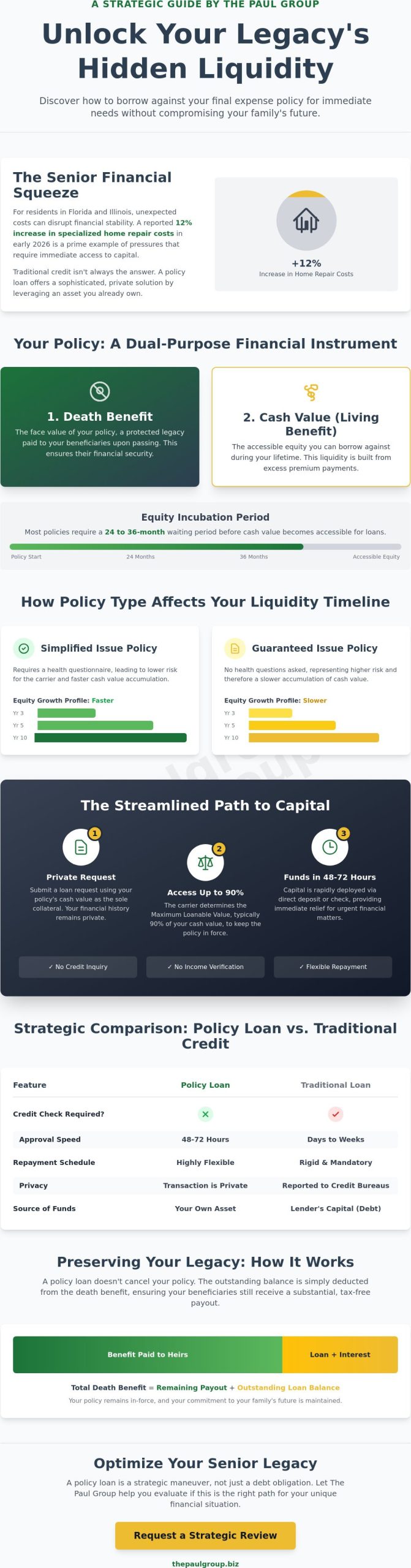

Permanent final expense insurance operates as a dual-purpose financial instrument. It provides a legacy for beneficiaries and a source of liquidity for the policyholder. This liquidity, or cash value, represents the living benefit of the contract. While the face value denotes the total death benefit paid upon passing, the accessible equity is the portion available for use during your lifetime. Borrowing against a final expense insurance policy requires a clear understanding of this equity timeline.

In jurisdictions like Florida and Illinois, state-specific insurance statutes govern how carriers manage reserve requirements and dividend distributions. These regulations ensure that the accumulation of policy dividends remains transparent and protected. Strategic growth depends on the carrier’s ability to optimize these reserves. Most policies require a 24 to 36-month incubation period before equity becomes actionable. This waiting period allows the carrier to offset initial acquisition costs and establish a stable foundation for capital growth.

Why Final Expense Policies Build Equity

The level-premium structure ensures that your monthly costs remain fixed regardless of age. During the early years, your premiums exceed the actual cost of insuring your life. These excess funds are diverted into a regulated, tax-deferred account. Cash value is the surrender value minus administrative costs. The Paul Group prioritizes carriers with efficient equity growth profiles to ensure our clients access capital sooner. By analyzing historical performance data from 2024 and 2025, we curate selections that maximize internal rates of return through disciplined carrier vetting.

Simplified Issue vs. Guaranteed Issue Equity

Your health status at the time of application dictates the speed of liquidity. Simplified issue policies, which require a health questionnaire, typically build equity faster than guaranteed issue options. This happens because the carrier assumes less risk and can allocate more premium dollars toward the cash account earlier in the policy life. Understanding Whole Life Insurance is critical here, as the underlying structure of these policies determines how quickly you can pivot from protection to utilization.

Strategic liquidity management involves recognizing that borrowing against a final expense insurance policy is more efficient when the policy is underwritten with full health transparency. Florida seniors with existing permanent coverage should evaluate their current health tier before seeking new liquidity options. For a deeper dive into policy types, you can review our analysis of the best final expense insurance for seniors pros and cons 2026. Our methodology focuses on identifying the intersection of human health and operational system efficiency.

The Methodology of Borrowing: How Policy Loans Function

The Paul Group identifies policy loans as a high-level strategic maneuver rather than a simple debt obligation. Borrowing against a final expense insurance policy functions through a curated methodology where the policy’s cash value acts as the exclusive collateral. This structural arrangement eliminates the need for credit inquiries or income verification. Because the contract is the security, your financial history stays private. This is a non-recourse transaction. The insurance provider has no legal standing to seek repayment from your personal estate or external assets. They simply recover the balance from the death benefit later.

Before initiating this process, it is vital to understand the foundational Types of Life Insurance that permit such liquidity. Only permanent policies, like those designed for final expenses, accumulate the necessary cash reserves to support a loan. Unlike term insurance, which expires without value, these policies represent a growing asset that you can leverage for immediate capital needs without surrendering the underlying coverage.

The Application and Approval Timeline

The sequence begins with a tailored request through The Paul Group or a direct carrier portal. Providers then determine the Maximum Loanable Value, which historically stabilizes at 90% of the total cash value. This threshold ensures the policy remains in force even as interest accrues. For residents in Florida and Illinois, disbursement is streamlined. Funds are typically issued within 48 to 72 hours through direct deposit or a physical check. This rapid deployment of capital allows for immediate intervention in pressing financial matters, providing a sense of security that traditional bank loans cannot match.

Interest Rates and Repayment Flexibility

Carriers set interest rates that are either fixed at the time of purchase or variable based on current market indices. The primary benefit for seniors is the absence of a rigid repayment schedule. There are no mandatory monthly installments. This creates a sustainable path for those managing fixed incomes. When you are borrowing against a final expense insurance policy, the carrier capitalizes the unpaid interest into the total loan balance if you choose to defer payments. This means the interest is added to the principal rather than being due immediately.

To explore how this fits into your broader financial plan, you might review our analysis of the pros and cons of final expense insurance for 2026. This methodology ensures that your coverage evolves alongside your shifting economic requirements, offering a bespoke solution for long-term stability.

Strategic Comparison: Policy Loans vs. Traditional Senior Credit

The decision to access capital involves more than just immediate cash flow; it requires a holistic evaluation of your financial architecture. When residents in Florida, Illinois face unexpected expenses, the default reaction is often to rely on high-interest credit cards or unsecured personal loans. These traditional avenues carry a heavy burden. Average credit card interest rates for seniors reached approximately 21.4% by late 2025. In contrast, borrowing against a final expense insurance policy typically involves interest rates between 5% and 8%. This significant delta represents capital preserved for your family rather than surrendered to external institutions.

The Wise Advisor perspective prioritizes the preservation of your credit score during liquidity needs. Traditional bank financing requires rigorous credit checks and monthly reporting to bureaus. A policy loan is different. Because you’re essentially borrowing against your own collateral, the carrier doesn’t report the transaction to credit agencies. This private arrangement allows you to secure funds without impacting your debt-to-income ratio or credit health, providing a strategic advantage for those who may need to qualify for other financing in the future.

Cost of Capital: Policy Loans vs. Bank Financing

Policy loans function as a private lending arrangement between you and the insurance carrier. You aren’t taking the company’s money; you’re accessing a lien against your own death benefit. This methodology keeps capital within the family ecosystem. Under current IRS guidelines, specifically the frameworks surrounding Section 7702, these loan proceeds remain tax-free as long as the policy stays in force. While a bank loan requires a rigid repayment schedule, policy loans offer flexible terms. You can choose to pay only the interest or let the interest accrue, though the latter requires careful monitoring to prevent policy lapse.

Risk Management for the Beneficiary

Liquidity is a powerful tool, but without disciplined intervention, it becomes a liability. In Florida, Illinois, where predatory lending practices can target vulnerable populations, borrowing against a final expense insurance policy serves as a protective barrier. However, the psychological impact on surviving family members must be considered. If a loan remains unpaid at the time of death, the balance is deducted from the final payout. This reduction can create a gap in the funds intended for funeral costs or debt settlement.

The Paul Group provides curated guidance to ensure your strategic alignment remains intact. We help you evaluate the best final expense insurance for seniors to determine if a loan serves as a temporary bridge or a long-term risk. Our methodology focuses on maintaining policy longevity, ensuring that current cash utility doesn’t erode the structural integrity of your estate. By treating the policy as a bespoke financial asset, we guide you toward solutions that balance immediate needs with a commitment to excellence for your beneficiaries.

Evaluating the Impact on Your Florida Final Expense Strategy

A pervasive myth suggests that accessing your policy’s cash value terminates your coverage. This isn’t true. When you consider borrowing against a final expense insurance policy, you’re utilizing a built-in financial utility rather than surrendering the contract. The policy remains in force as long as the total debt, including interest, doesn’t exceed the accumulated cash value. It’s a tool for liquidity, not a cancellation of your intent.

Strategic clarity requires understanding the net death benefit calculation. Your beneficiaries won’t receive the original face value if a loan exists at the time of your passing. Instead, the payout is the face value minus the outstanding loan and accrued interest. If you hold a $15,000 policy and carry a $3,000 loan balance, the final disbursement becomes $12,000. Precision in this calculation ensures your family isn’t left with an unexpected financial shortfall during a period of grief.

Local economic factors in Florida and Illinois dictate the necessity of this precision. In 2026, the average cost of a traditional funeral with burial in these states ranges from $8,000 to $12,000 according to current industry benchmarks. If borrowing against a final expense insurance policy reduces the death benefit below these thresholds, your strategic alignment is compromised. You can mitigate this risk by initiating disciplined, partial repayments to replenish the death benefit over time, ensuring the original legacy remains fully funded.

Protecting the Funeral Legacy

Maintaining enough liquidity to cover local Florida cremation or burial costs is the primary objective of any senior insurance plan. Some policyholders use loan proceeds for pre-need expenses, such as purchasing a cemetery plot or headstone today to lock in current prices. While this is a proactive move, you must monitor the balance closely. If the loan interest causes the debt to exceed the cash value, the policy will lapse. This results in the loss of all protection, representing a total failure of the original estate plan.

The Paul Group’s Strategic Intervention

Our team provides a curated analysis for clients in Florida and Illinois who’ve accessed their cash value. We re-evaluate your coverage to determine if the remaining benefit still meets your long-term objectives. This often involves adjusting the strategic alignment of your portfolio to account for the new debt. Reviewing the best final expense insurance pros and cons helps you decide if a policy adjustment or a supplemental plan is required to fill the gap created by the loan.

Optimizing Your Senior Legacy with The Paul Group

The Paul Group operates on the principle that permanent life insurance is a cornerstone of a sophisticated financial architecture. We move beyond the transactional nature of traditional insurance sales to provide a partnership-driven approach. This methodology ensures that your policy serves as a dynamic asset rather than a static expense. Our commitment to intellectual rigor means every plan we recommend undergoes a rigorous vetting process to ensure it aligns with your specific financial DNA. We view your legacy as a structural evolution of your life’s work. Our collective of experts brings diverse viewpoints to the table, ensuring that no detail of your estate is overlooked.

For seniors in Florida and Illinois, securing immediate coverage that prioritizes cash value accumulation is paramount. This strategic alignment allows for the possibility of borrowing against a final expense insurance policy should liquidity needs arise in the future. We focus on the intersection of human leadership and operational systems to protect your family’s stability. By 2026, the demand for flexible financial instruments has increased by 14% among seniors, making the selection of a high-performance policy more critical than ever. Our firm provides the visionary leadership necessary to transform a simple insurance requirement into a robust financial tool.

Bespoke Policy Selection

We don’t offer generic, off-the-shelf products. Our team curates plans from the top 1% of carriers to maximize your future borrowing power. Strategically engineered coverage differs from standard plans by optimizing the premium-to-cash-value ratio from day one. As your Wise Advisor in Florida and Illinois, we leverage our local presence to navigate the specific regulatory environments of these states. This localized expertise ensures your final expense insurance remains robust and compliant. We prioritize long-term stability over quick, superficial fixes.

Requesting a Strategic Consultation

Your path to financial clarity begins with a no-obligation executive briefing. This session is designed to balance your death benefit requirements with the strategic advantage of living benefits. We provide a comprehensive quote that reflects the current 2026 market conditions, focusing on sustainable scaling of your policy’s value. Borrowing against a final expense insurance policy requires a foundation of structural integrity that only a bespoke plan can provide. Secure the future of your family today by aligning with a partner who values excellence. Contact The Paul Group to begin your transformation and secure a legacy built on disciplined intervention and strategic clarity.

Elevating Your Legacy Through Strategic Liquidity

Navigating the complexities of senior liquidity requires a disciplined methodology. Leveraging the cash value within your plan offers a non-recourse alternative to traditional senior credit, which typically involves more stringent credit requirements. By understanding the mechanics of borrowing against a final expense insurance policy, you maintain control over your financial ecosystem while ensuring your legacy remains intact. This strategic approach transforms a static safety net into a dynamic tool for immediate needs. It’s a method that prioritizes structural integrity over quick fixes.

Since 2009, The Paul Group has specialized in these curated legacy protection strategies across Florida, Illinois, and numerous other states. Our methodology focuses on sophisticated, no-exam policies that deliver immediate peace of mind without the friction of traditional underwriting. We align your current liquidity requirements with your long-term estate goals; we’ve seen how this alignment creates sustainable stability for families. You don’t have to navigate these structural decisions alone. Our team provides the intellectual rigor necessary to optimize your senior legacy. Request a Strategic Final Expense Consultation with The Paul Group to begin your transformation today. Your future stability is a deliberate choice, and we are ready to help you make it.

Frequently Asked Questions

Can I borrow against a term life insurance policy for final expenses?

No, term life insurance policies generally lack the cash value component required for a policy loan. Term insurance provides coverage for a specific window, such as a 10 or 20 year period, but doesn’t build equity. Borrowing against a final expense insurance policy requires a whole life structure where a portion of premiums accumulates as accessible cash value. Most policies issued in 2026 prioritize this structural integrity to ensure liquidity for policyholders.

How soon after taking out a policy in Florida can I borrow against it?

Policyholders in Florida typically wait two to three years before sufficient cash value accumulates to support a loan. This waiting period allows premium payments to offset initial administrative costs and begin building the equity of the policy. The Group observes that most permanent contracts require a minimum of $500 in surrender value before an advance is authorized. This timeline remains consistent with Florida Office of Insurance Regulation standards observed through 2026.

Do I have to pay back the loan on my final expense policy?

You aren’t legally required to make monthly repayments on a policy loan, but interest will accrue against the remaining cash value. While the debt is technically a lien against your own asset, failing to manage the balance can lead to a policy lapse if interest exceeds the total cash value. We recommend a curated repayment strategy to maintain the policy’s structural health. This proactive approach ensures your death benefit remains intact for its intended purpose.

Will borrowing money from my policy affect my taxes in Illinois?

Policy loans are generally considered tax-free distributions in Illinois because they’re viewed as debt rather than income. Internal Revenue Code Section 72 governs these transactions, ensuring that as long as the policy stays active, the loan remains non-taxable. If the policy terminates before the loan is repaid, the IRS may classify the forgiven debt as taxable income. Our methodology emphasizes maintaining policy stability to avoid these unintended fiscal consequences.

What happens to the funeral benefit if I die with an outstanding loan?

The insurance carrier deducts the outstanding loan balance and accrued interest from the total death benefit before paying your beneficiaries. If your policy provides a $15,000 benefit and you owe $2,000, your family receives $13,000. This reduction can jeopardize the optimization of your final arrangements if the loan isn’t accounted for in your estate plan. Borrowing against a final expense insurance policy requires careful alignment with your long-term legacy goals.

Is there a credit check required to borrow from my burial insurance?

No credit check is required because you’re essentially borrowing your own collateralized funds. Since the cash value of the policy secures the loan, the insurance company faces zero risk of default. This accessibility makes policy loans a strategic tool for those with credit scores below the 670 benchmark typically required for traditional personal loans. It’s a bespoke liquidity solution that bypasses conventional banking hurdles and bureaucratic delays.

How much interest will I be charged on a policy loan in 2026?

Interest rates for policy loans in 2026 generally range between 5% and 8% depending on whether the rate is fixed or variable. These rates are dictated by the specific contract language and current Moody’s Corporate Bond Yield averages. While these charges accrue annually, they’re often lower than the 21% average interest rate seen on unsecured credit cards. The Group views these loans as a mechanism for sustainable scaling of personal liquidity.

Can my family in Florida be held liable for an unpaid policy loan?

Your family members in Florida cannot be held personally liable for an unpaid policy loan after your death. The debt is tied exclusively to the policy’s death benefit and does not transfer to heirs or the general estate. Florida consumer protection statutes ensure that life insurance proceeds are generally shielded from creditors. This legal framework provides a layer of security, ensuring that your strategic financial decisions don’t create a burden for your descendants.

Leave a Reply