How to Pre-Plan My Funeral Financially in Florida, Illinois: A Strategic 2026 Guide

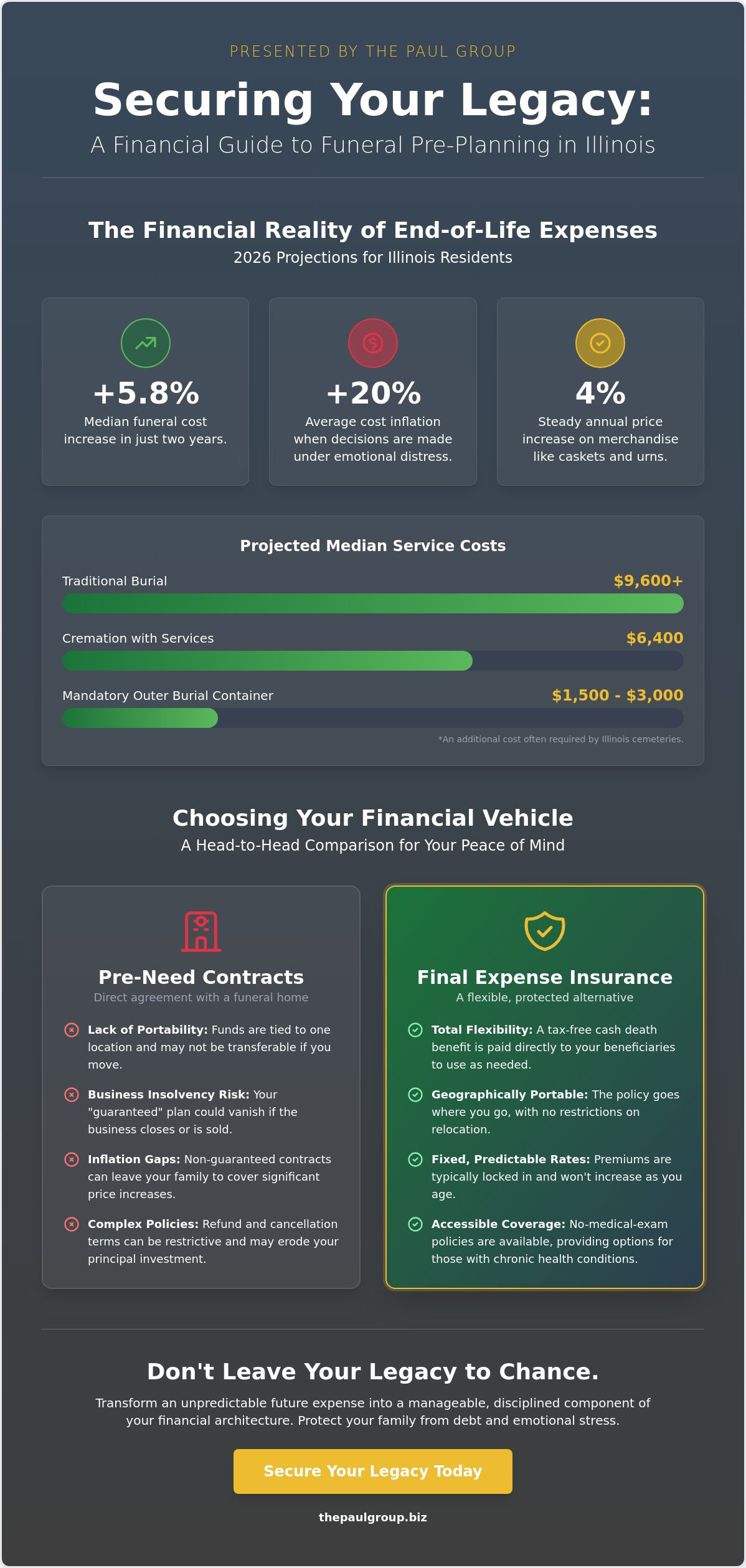

Legacy is often viewed as a collection of shared memories, yet for many families in the Illinois region, it’s the 2026 reality of unmanaged liabilities that defines the final inheritance. According to the National Funeral Directors Association 2023 report, median funeral costs have increased by approximately 5.8% over just two years. You likely recognize that your final wishes deserve a degree of precision that matches your life’s work. It’s a common concern that these rising costs and administrative ambiguity might overshadow the stability you’ve built for your loved ones. Understanding how to pre-plan my funeral financially is not merely a task of checking boxes; it’s a vital component of a comprehensive estate strategy.

This guide provides the sophisticated financial frameworks required to secure your legacy and shield your family from end-of-life debt in Florida, Illinois. The Paul Group has curated a roadmap that offers protection against inflation and the legal certainty that your funds are utilized as intended. By examining the methodology behind inflation-protected contracts and the critical distinctions between life insurance and prepaid arrangements, we’ll transform a complex burden into a disciplined, forward-looking plan for your future.

The Strategic Imperative of Financial Pre-Planning for Seniors

Financial security in retirement requires more than wealth accumulation; it demands a proactive risk-mitigation strategy to address end-of-life costs. For residents in Florida, Illinois, understanding how to pre-plan my funeral financially is no longer a peripheral concern but a central pillar of estate liquidity. The Paul Group views this process as a sophisticated alignment of personal values and fiscal responsibility. Traditional estate planning often focuses on asset distribution, yet fails to account for the immediate cash flow requirements triggered by a death. Without a curated plan, the burden of these costs falls on survivors during their period of highest emotional vulnerability.

The Illinois funeral market reflects a broader economic shift. Since 2021, service fees have climbed by approximately 15 percent across the Midwest. Relying on hope as a strategy fails families during the immediate emotional turmoil of loss. It often forces survivors to liquidate assets at a loss or incur high-interest debt to cover immediate obligations. A holistic financial legacy plan distinguishes itself from simple arrangements by integrating funeral funding into the broader context of tax optimization and asset protection. This disciplined approach ensures that the transition of a legacy remains seamless and dignified.

Understanding the Emotional and Financial ROI

Quantifying the value of peace of mind requires looking at the hidden costs of reactive decision-making. When grief dictates purchasing, costs inflate by an average of 20 percent compared to pre-planned arrangements. Consumers who understand the FTC’s Funeral Rule gain the right to purchase only the goods and services they want, rather than accepting bundled packages that may include unnecessary fees. Financial pre-planning serves as a disciplined intervention against future debt, ensuring that the finality of life doesn’t trigger a cascade of fiscal instability for those left behind. By removing the financial guesswork, you provide your family the space to focus on remembrance rather than resource allocation. This strategic foresight is a final act of leadership within the family unit.

The 2026 Landscape of Funeral Costs in Illinois

The 2026 economic environment presents unique challenges for seniors in Florida, Illinois. Projections indicate the median cost of a traditional burial in the region will exceed $9,600, while cremation services are expected to average $6,400 when including professional service fees. Inflation continues to impact merchandise such as caskets and urns, which have seen a steady 4 percent annual price increase over the last decade. Residents must also account for local cemetery and vault requirements. Most Illinois cemeteries mandate an outer burial container to prevent ground settling, a cost that can add $1,500 to $3,000 to the total bill. Identifying how to pre-plan my funeral financially allows you to lock in current rates or allocate specific funds through tools like best final expense insurance for seniors. This methodology transforms an unpredictable future expense into a manageable, structured component of your long-term financial architecture.

Comparing Financial Vehicles: Prepaid Plans vs. Final Expense Insurance

Deciding how to pre-plan my funeral financially requires a rigorous evaluation of liquidity, risk, and structural integrity. You aren’t just buying a service; you’re engineering a legacy. Understanding the nuances of different financial vehicles is the first step in learning how to pre-plan my funeral financially with absolute certainty. Two primary models dominate this space: pre-need contracts and final expense insurance. Each offers a distinct methodology for sequestering funds, yet they carry vastly different implications for your survivors.

Pre-Need Contracts: The Risks of Lack of Portability

Pre-need contracts involve a direct agreement with a specific funeral home. While they offer the ability to lock in specific service details, they often lack geographical agility. If you relocate from Florida or Illinois after signing, your funds may not be easily transferable. According to the FTC guide to funeral planning, these contracts often come with complex refund policies that can erode your principal. Business insolvency is another critical variable. If a local home closes or changes ownership, your “guaranteed” price structure might vanish. Non-guaranteed contracts are even more volatile, as they leave survivors responsible for inflation-driven price gaps at the time of service, which can be substantial given that funeral costs have historically risen by 6.4% annually.

Final Expense Insurance: A Strategic Alternative

Final expense insurance operates through a cash death benefit paid directly to beneficiaries. It’s a curated solution for those seeking total flexibility. These policies typically feature fixed rates that won’t increase as you age. For seniors with chronic health conditions, no-medical-exam policies represent a streamlined path to coverage. This vehicle ensures that funds are available for more than just the casket; they can cover medical debts, utility bills, or travel for family. You should evaluate the pros and cons of final expense insurance for seniors to determine if this aligns with your broader estate goals. Unlike pre-need contracts, insurance follows you regardless of where you live, providing a portable safety net.

Strategic alignment also involves considering Medicaid and asset-limit regulations. In many states, including Illinois and Florida, an irrevocable funeral trust or a specifically designated life insurance policy can be structured as an exempt asset. This allows you to protect your eligibility for long-term care while securing your final wishes. We recommend a consultative review of your current assets to ensure your plan remains compliant with state regulations. Proper planning ensures that your transition doesn’t become a financial burden on those you lead.

- Fixed Rates: Premiums remain consistent throughout the life of the policy.

- Immediate Liquidity: Cash benefits are typically paid within 24 to 48 hours of a claim.

- Asset Protection: Strategic placement in irrevocable vehicles can shield funds from creditors.

Navigating Local Regulations and Rights in Florida, Illinois

Strategic financial planning requires a firm grasp of the legal architecture governing death care. In Florida, Illinois, located within the Madison County corridor, your financial security rests on state-mandated safeguards that prevent the mismanagement of pre-paid assets. Understanding how to pre-plan my funeral financially involves more than just selecting services; it requires auditing the regulatory framework that protects your capital from insolvency or fraud. The Illinois Comptroller’s office serves as the primary watchdog, overseeing thousands of pre-need trust funds to ensure providers maintain fiduciary integrity.

Illinois Consumer Protections for Burial Funds

The Illinois Funeral or Burial Funds Act provides the primary defense for your investment. Under this statute, funeral directors must deposit 95% of the funds received for services and 100% of the funds for certain merchandise into a third-party trust or a qualifying insurance policy. This sequestration ensures that your money remains available even if the local provider undergoes a change in ownership or business failure. When evaluating Illinois funeral planning basics, you’ll find that state law demands a rigorous separation of your investment from the funeral home’s operational accounts.

You possess a 30-day “cooling-off” period after signing a pre-need contract. During this window, you can cancel the agreement for a full refund. Beyond this period, Illinois law still allows for the transfer of these funds to a different provider, though certain administrative fees may apply. Always verify a provider’s standing through the Illinois Department of Financial and Professional Regulation (IDFPR) before committing capital. This verification confirms that the director holds a valid license and has no history of disciplinary actions in Madison County.

The FTC Funeral Rule in Practice

Federal oversight complements state law through the FTC Funeral Rule. This regulation prevents providers in the Florida and Edwardsville area from forcing you into bundled packages that include unnecessary services. You have the legal right to an itemized General Price List (GPL) the moment you begin discussing arrangements. This document allows for a granular analysis of costs, ensuring you only pay for the specific honors you desire. Precision in selection is the cornerstone of a disciplined financial strategy.

- Casket Rights: You can purchase a casket or urn from a third-party vendor. Local providers cannot charge a “handling fee” for accepting these items.

- No Forced Bundling: Providers must allow you to choose individual services rather than all-inclusive packages.

- Price Transparency: Directors must provide pricing over the telephone if requested, allowing for efficient market comparisons.

Regulatory safety in Illinois provides the foundation for your financial strategy. For those seeking to augment these protections with specialized financial instruments, analyzing the best final expense insurance for seniors can offer an additional layer of liquidity and tax-advantaged growth. By leveraging both state protections and private insurance, you create a robust shield for your estate’s legacy.

A Disciplined Step-by-Step Roadmap to Financial Pre-Planning

Strategic planning demands a departure from vague intentions. It requires a structured methodology to ensure your legacy remains a point of pride rather than a source of logistical friction for your family. Understanding how to pre-plan my funeral financially requires a transition from emotional reacting to disciplined execution. This roadmap provides the structural integrity needed to secure your future interests.

- Step 1: Conduct a holistic audit. Document your specific end-of-life wishes, ranging from the type of service to the final disposition. This audit serves as the blueprint for all subsequent financial allocations.

- Step 2: Research local service providers. Investigate funeral homes and cemeteries within the Florida, Illinois vicinity. Requesting General Price Lists (GPL) now establishes a baseline for 2026 market rates.

- Step 3: Select the optimal financial vehicle. Determine whether a life insurance policy, a specialized funeral trust, or a Payable on Death (POD) bank account offers the most strategic alignment with your liquidity needs.

- Step 4: Formalize the plan. Work with a legal advisor or a specialized insurance partner to document the arrangement. This step ensures the funds are protected and accessible at the precise moment of need.

- Step 5: Communicate the strategic alignment. Brief your beneficiaries on the plan’s structure. Clarity at this stage prevents future disputes and ensures your executors can act with confidence.

Determining Your “Final Number”

Precision is paramount when calculating your total financial commitment. You must account for hidden costs that many families overlook, such as newspaper obituaries, certified copies of death certificates, and clergy honorariums. These items can add $500 to $1,500 to the total invoice. Distinguish between “at-need” pricing, which reflects current market rates, and “pre-need” pricing, which often allows you to lock in today’s costs. We recommend factoring in a 10-15% buffer to account for regional price fluctuations and unforeseen administrative adjustments. This margin of safety ensures the plan remains robust regardless of economic shifts.

Selecting the Right Partner

The efficacy of your plan depends on the caliber of your financial partner. Seek companies with a proven track record of high-level industry expertise rather than generalist firms. A broker-led approach is inherently superior to a single-carrier agent because it provides a curated selection of products tailored to your unique profile. For seniors, prioritizing immediate coverage options is vital. You don’t want a plan with a two-year waiting period if your goal is immediate peace of mind. Intellectual rigor in the selection process leads to a more sustainable and secure outcome.

To evaluate the specific advantages of different funding strategies, explore our analysis of the best final expense insurance for seniors.

Curating Your Legacy with The Paul Group’s Strategic Intervention

Deciding how to pre-plan my funeral financially requires more than a simple policy selection; it demands a disciplined intervention that aligns your final wishes with structural fiscal integrity. The Paul Group facilitates this transition by distilling the noise of the insurance market into a clear, actionable roadmap. Our methodology relies on a rigorous vetting process to identify the most stable and efficient insurance carriers, ensuring that your legacy is backed by institutional strength. We don’t settle for off-the-shelf products. Instead, we focus on strategic alignment between your current assets and your future obligations. This high-level oversight removes the friction often associated with end-of-life logistics, allowing you to focus on the human elements of your legacy.

When you engage with our team to learn how to pre-plan my funeral financially, you are choosing a path of structural integrity. Our Wise Advisors bring a sense of quiet confidence to every discussion, offering insights that go beyond basic coverage. We view funeral planning as a critical component of a holistic financial strategy, one that requires the same level of intellectual rigor as any other major investment. This results-oriented approach ensures that your plan is not just a document, but a living strategy designed to withstand economic shifts and personal changes. Our goal is to move you from a state of organizational complexity to one of absolute financial clarity.

Bespoke Solutions for Florida, Illinois Seniors

Seniors in the Florida, Illinois area face a unique set of market conditions that require localized expertise. Our commitment to fixed rates ensures that your premiums never increase, providing a level of predictability that is essential for fixed-income households. We prioritize no-medical-exam qualifications, which allows 95% of applicants to secure coverage regardless of their health history. This collective expertise within our agent network provides the sustainable scaling your legacy needs. You can initiate a consultation for a personalized financial audit today. During this session, we diagnose your unique challenges before prescribing a tailored solution that fits your specific needs.

The Paul Group Advantage: Beyond the Transaction

Our partnership-driven approach ensures your plan remains relevant as your life evolves. This isn’t a simple transaction; it’s a long-term commitment to excellence. We provide the reassurance of immediate coverage for peace of mind, protecting your family from the moment the policy is enacted. By working with a Wise Advisor who understands the nuances of the local market, you gain access to curated insights that protect your beneficiaries from administrative burdens. This progression from complexity to clarity is the hallmark of our firm. It’s time to secure your family’s future through disciplined planning and visionary leadership. Schedule your strategic consultation with The Paul Group today to begin your transformation.

Architecting Your Strategic Legacy

Mastering the complexities of end-of-life logistics requires more than simple intent; it demands a curated financial methodology. You’ve now navigated the critical distinctions between restrictive prepaid contracts and the flexibility of final expense insurance while identifying the specific regulatory nuances governing Florida and Illinois. Since 2009, The Paul Group has specialized in this high-level strategic alignment, providing seniors with a roadmap that prioritizes structural integrity over superficial fixes.

Understanding how to pre-plan my funeral financially isn’t just about cost mitigation. It’s about ensuring your legacy remains unburdened by administrative or fiscal friction. Our methodology removes the barriers of traditional underwriting, offering immediate coverage with no medical exam required. As a firm licensed across Illinois and Florida, we bring a disciplined, expert perspective to your estate’s final requirements, ensuring every detail aligns with your long-term vision.

True optimization of your future starts with a single, decisive action. Secure your legacy with a strategic final expense plan from The Paul Group. We’re ready to help you transform uncertainty into a lasting, orderly vision for the years ahead.

Frequently Asked Questions

Is it better to prepay a funeral home or buy life insurance for my funeral?

Choosing between prepaying a funeral home and purchasing life insurance depends on your priority for price certainty versus financial liquidity. Prepaying a contract directly with a provider in Florida, Illinois, often locks in current service rates based on 2024 industry standards, protecting against future inflation. Conversely, final expense life insurance provides a tax-free death benefit that your beneficiaries can use flexibly for any immediate needs. This strategic choice requires a curated approach to ensure your legacy remains structurally sound.

How much does the average funeral cost in Illinois in 2026?

The projected median cost for a funeral with a viewing and burial in Illinois is approximately $9,070 for 2026. This figure stems from the National Funeral Directors Association 2023 report, which established a median cost of $8,300 before accounting for an average annual inflation rate of 3 percent. These calculations exclude cemetery fees, which can add $2,000 to $4,000 to the total expenditure. Understanding these benchmarks allows for precise financial optimization of your estate.

Can I move my prepaid funeral plan if I leave Florida, Illinois?

Portability of your prepaid funeral plan depends entirely on whether the contract is “guaranteed” or “non-guaranteed” under the Illinois Funeral or Burial Funds Act. While many Florida, Illinois providers offer transferable policies, the new funeral home isn’t legally obligated to honor the original price lock. You’ll likely receive the principal and interest from the trust to apply toward new arrangements. Reviewing the specific transferability clause in your agreement ensures your strategic alignment remains intact across state lines.

What is an Irrevocable Burial Trust and how does it protect my assets?

An Irrevocable Burial Trust is a specialized financial vehicle that excludes funeral funds from your countable assets during Medicaid eligibility assessments. By transferring up to $15,000 into a trust that cannot be cancelled, you protect these funds from being consumed by long-term care costs. This methodology provides a dual benefit of securing your final wishes while facilitating sustainable scaling of your healthcare strategy. It’s a cornerstone of sophisticated estate transformation that values long-term stability.

Does Social Security provide any financial assistance for funeral costs?

Social Security provides a one-time lump-sum death payment of exactly $255 to eligible surviving spouses or children. This amount hasn’t changed since 1954 and represents only a fractional portion of modern service costs. Because this benefit is minimal, learning how to pre-plan my funeral financially through private instruments is essential for total cost coverage. Relying on federal subsidies alone creates a significant deficit in your organizational legacy planning and fails to address the nuances of modern funeral expenses.

What happens to my funeral insurance if the insurance company goes out of business?

Your policy is protected by the Illinois Life and Health Insurance Guaranty Association if a licensed insurer faces insolvency. This state-mandated safety net typically covers death benefit claims up to $300,000 per individual. We recommend verifying that your provider is a member of this association to ensure long-term structural integrity. This layer of systemic protection offers the reassurance needed when committing to high-level financial commitments, ensuring your investment remains secure regardless of market shifts.

Do I need a medical exam to qualify for final expense insurance in Illinois?

Most final expense insurance policies in Illinois don’t require a physical medical examination for approval. Instead, providers use simplified issue applications with health questionnaires or guaranteed issue options that ignore medical history entirely. While these products provide immediate accessibility, they often carry higher premiums than traditional life insurance. Selecting the right tier requires a holistic view of your current health status and long-term capital preservation goals to avoid unnecessary expenditure.

How can I ensure my family knows about my financial pre-planning?

Effective communication of your financial strategy involves centralizing your documentation and conducting a formal family briefing. Provide your beneficiaries with copies of the Statement of Funeral Goods and Services Selected and the contact details for your chosen Florida, Illinois provider. Since only 19 percent of adults have shared their final plans according to 2021 industry surveys, proactive disclosure is vital. This clarity prevents operational confusion and ensures your curated legacy is executed with the precision you intended.

Leave a Reply