How to Pre-Plan My Funeral Financially in Florida, Illinois: A 2026 Strategic Guide

By 2026, the National Funeral Directors Association projects that funeral inflation will continue its 6.4% five-year upward trajectory, potentially transforming a standard service into a significant liability for unprepared estates. What if your final act of leadership wasn’t a burden, but a masterfully executed transition? You likely agree that protecting your family’s inheritance in Florida, Illinois requires more than just good intentions; it demands a disciplined approach to asset protection. Learning how to pre-plan my funeral financially isn’t merely about choosing a casket. It’s about the strategic alignment of your current resources against future market volatility.

The Paul Group provides a curated, step-by-step methodology designed to secure your final arrangements while shielding your loved ones from the complexities of rising 2026 market costs. We’ve developed a path that replaces anxiety with immediate coverage and transforms confusing insurance jargon into a clear, high-level executive summary. This guide details exactly how to optimize your estate through strategic asset allocation, ensuring your legacy remains intact and your family experiences the peace of mind they deserve.

The Strategic Value of Financial Pre-Planning in Florida, Illinois

Financial funeral pre-planning represents a sophisticated pivot from reactive mourning to proactive asset protection. While most families focus on the emotional aesthetics of a service, the strategic imperative for 2026 involves the disciplined management of capital. Residents of Florida, Illinois, understand that local logistical nuances require a curated approach to legacy. This isn’t merely a checklist of preferences; it’s a structural evolution of your estate plan that ensures your liquid assets remain preserved for your heirs rather than being consumed by immediate, unplanned expenses. We view this process as a high-level optimization of your final transition.

Our methodology treats end-of-life arrangements as a bespoke organizational challenge. By addressing the financial components now, you eliminate the volatility that typically accompanies these events. You’re not just choosing a casket or a service style. You’re establishing a strategic alignment between your current wealth and your future requirements. This level of foresight projects a sense of quiet confidence, reassuring your family that their most complex moments have been solved through disciplined intervention.

Pre-Planning vs. Pre-Paying: A Critical Distinction

Understanding how to pre-plan my funeral financially requires a clear separation between intent and execution. Many individuals mistakenly conflate pre-planning with pre-paying directly to a service provider. Locking funds into a single, localized contract carries inherent risks. Our mobile 2026 society demands agility. A rigid contract might not follow you if you relocate or if the provider undergoes a corporate restructuring. Strategic pre-planning focuses on creating a designated fund that you control, ensuring portability and structural integrity.

This approach prevents the common trap of emotional overspending. Grieving survivors often make high-cost decisions driven by urgency rather than logic. By defining the financial boundaries in advance, you provide a roadmap that bypasses unnecessary upgrades and focuses on your specific values. It’s a way to maintain intellectual order during a time of emotional complexity.

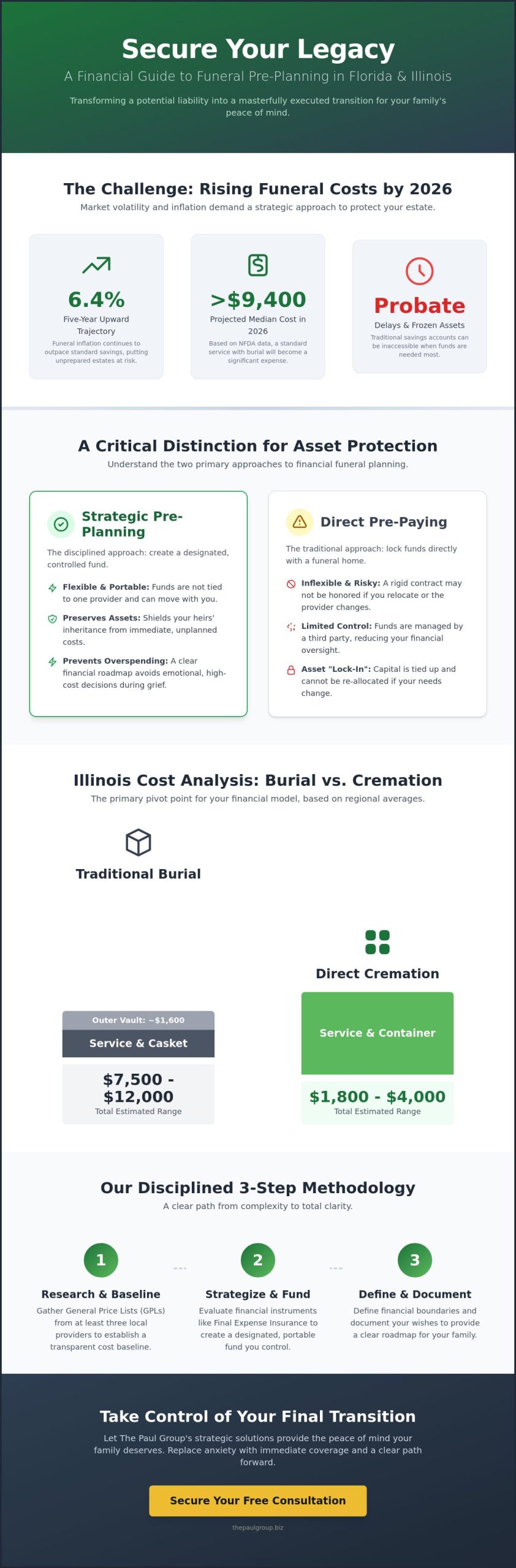

The Macro-Trend: Rising Funeral Costs in 2026

The death care industry has undergone a significant transformation in its cost structures. By 2026, inflationary pressures have rendered traditional savings accounts insufficient for covering end-of-life logistics. These standard accounts often trigger probate delays, leaving families without the immediate liquidity needed to settle accounts. To protect your interests, you should leverage protections like the FTC’s Funeral Rule, which mandates that providers offer itemized pricing. This transparency allows for a more holistic optimization of your budget.

For those seeking to align their resources with specific insurance vehicles, exploring the best final expense insurance for seniors can provide the necessary capital injection at the exact moment of need. We view this as a sustainable scaling of your legacy. It ensures that your final transition is handled with the intellectual rigor it deserves, moving you from a state of complexity to one of total clarity.

Navigating the Florida, Illinois Funeral Landscape and Local Costs

Understanding the fiscal landscape of Madison County and the broader Illinois region is the first step in a disciplined legacy strategy. Professional oversight of your end-of-life arrangements prevents emotional overspending during a period of acute vulnerability. Learning how to pre-plan my funeral financially requires more than just intent; it demands a forensic look at local market rates and the regulatory frameworks that govern them. In 2024, the National Funeral Directors Association reported that the median cost of a funeral with burial exceeded $8,300, yet in the Illinois corridor, these figures often fluctuate based on proximity to metropolitan centers. You must secure a General Price List (GPL) from at least three local providers to establish a comparative baseline. This document is your primary tool for transparency, as it itemizes every service from professional fees to transportation costs.

Regional Cost Drivers: Burial vs. Cremation in IL

The choice between traditional burial and modern cremation serves as the primary pivot point for your financial model. Traditional burial services in Illinois typically range from $7,500 to $12,000, driven largely by the cost of metal or wood caskets and the scarcity of cemetery plots in established districts. Conversely, direct cremation options in the region average between $1,800 and $4,000. You don’t need to visit every facility in person to conduct this research. Digital inquiries and phone consultations are effective methods for gathering data. Be sure to ask about outer burial container requirements, as most Illinois cemeteries mandate a concrete vault to prevent ground settling, adding an average of $1,600 to your total expenditure.

Legal Safeguards for Florida, Illinois Residents

Illinois law provides robust protections for consumers engaging in pre-need contracts. The Illinois Department of Financial and Professional Regulation (IDFPR) oversees the licensing of funeral directors, ensuring that ethical standards remain high across the state. One critical protection involves the handling of your funds. Under the Illinois Funeral or Burial Funds Act, providers must deposit 95% of the money received for services and 100% of the money for merchandise into a trust account or an insurance-funded policy. This structure ensures your capital remains protected even if the funeral home changes ownership or ceases operations. It’s also vital to consult the FTC guidance on funeral planning to understand your right to purchase caskets from third-party retailers without incurring “handling fees” from the funeral home.

The Illinois Funeral Directors Association sets rigorous industry standards that further insulate you from predatory practices. These regulations allow you to decline embalming if you select certain types of arrangements, such as direct cremation or immediate burial, unless specific state health laws apply. As you refine your strategy, consider how a tailored final expense insurance policy can provide the liquidity needed to cover these costs without depleting your estate’s core assets. This approach transforms a complex logistical burden into a manageable, structured financial plan. By aligning your personal preferences with the legal protections available in Illinois, you create a sustainable roadmap that honors your legacy while protecting your survivors from unnecessary fiscal strain.

Evaluating Financial Instruments: Pre-Paid Plans vs. Final Expense Insurance

The 2026 economic environment demands a sophisticated approach to end-of-life logistics. When you research how to pre-plan my funeral financially, you’ll encounter two primary paths: pre-paid contracts and life insurance. Pre-paid plans involve paying a specific funeral home in advance for a set list of services. While this might seem secure, it tethers your legacy to the operational health of a single business entity. If that funeral home files for bankruptcy or ceases operations, your funds may be tied up in state-regulated trusts for years. Life insurance policies, conversely, represent a contract with a multi-billion dollar financial institution. These entities are subject to rigorous solvency requirements that far exceed those of a local mortuary.

Structural integrity is the primary differentiator here. As a superior funding vehicle, Final Expense Life Insurance offers a level of flexibility that traditional contracts cannot match. Beyond the safety of the principal, life insurance death benefits provide a strategic tax advantage. Under Internal Revenue Code Section 101(a), beneficiaries generally receive these funds free of federal income tax. This ensures that every dollar you’ve allocated for your final wishes is delivered at its full face value, providing immediate liquidity during a time of high emotional and financial stress.

The Portability Factor: Why Final Expense Wins

Florida and Illinois see some of the highest rates of senior relocation in the country. A pre-paid contract signed in Sarasota may not carry its full value to a facility in Chicago. Insurance policies offer universal portability; they follow the individual, not the institution. This control is essential for those seeking expert advice on pre-planning to avoid being locked into a specific region. Any remaining funds after the service can be utilized for outstanding medical debts or legal fees, ensuring a holistic settlement of your estate.

Risk Mitigation: Protecting Your Principal

Insurance payouts provide a level of certainty that pre-need trusts often lack. While trusts are susceptible to administrative fees and market volatility, insurance benefits are fixed and guaranteed. Most high-quality senior plans include an “Immediate Coverage” clause, which ensures that even if a policyholder passes away shortly after the first premium payment, the full benefit is disbursed. Final Expense Insurance is a curated solution for seniors aged 50-85. This instrument provides the structural integrity needed to ensure your final wishes don’t become a financial burden. Learning how to pre-plan my funeral financially requires this shift from localized service contracts to diversified financial assets.

A Step-by-Step Methodology for Financial Pre-Planning

Precision is paramount when securing your legacy. Learning how to pre-plan my funeral financially requires a structured approach that moves beyond simple savings; it demands a curated strategy designed to mitigate inflation while ensuring immediate liquidity. This methodology transforms a complex emotional burden into a manageable operational task through four disciplined stages.

- Stage 1: The Holistic Audit. Conduct a rigorous assessment of end-of-life wishes against current market rates. This includes a line-item review of professional services, facilities, and merchandise.

- Stage 2: Strategic Partnership. Research and select a financial partner that specializes in senior needs. Look for firms that prioritize long-term stability over high-volume, transactional models.

- Stage 3: Capital Optimization. Secure a Simplified Issue policy. These instruments provide immediate capital availability upon death, bypassing the lengthy probate cycles that often freeze traditional assets for 6 to 12 months.

- Stage 4: Strategic Alignment. Document the plan and communicate the specifics to your inner circle. A plan that exists only in a vacuum is a liability, not an asset.

Inventory and Cost Estimation

Success begins with accurate data. Utilize a funeral cost calculator to identify your specific funding gap. According to 2023 data from the National Funeral Directors Association, the median cost of a funeral with a viewing and burial is $8,300. However, this figure often excludes “hidden” operational expenses. In Florida and Illinois, death certificates typically cost between $15 and $20 per copy; most estates require at least 10 copies for various financial institutions. You must account for obituaries, which can exceed $500 in major metropolitan newspapers, and transportation fees that fluctuate based on fuel surcharges. A truly holistic “Final Expense” strategy covers the casket and the logistical friction that follows.

Communication and Strategic Alignment

The Wise Advisor approach focuses on transparency. Initiate a conversation with your children or beneficiaries that frames this as a gift of clarity rather than a discussion of loss. Detail exactly where policy documents are stored; these must be accessible within 24 hours to be effective. The beneficiary’s role is not merely to receive funds, but to execute the financial plan you’ve engineered. By providing them with a clear roadmap, you ensure the strategy is implemented with the same intellectual rigor used to create it. This alignment prevents emotional overspending during a period of high stress.

To understand the specific advantages of different funding vehicles, explore our analysis of the best final expense insurance for seniors to determine which structure fits your unique financial DNA.

Securing Your Legacy with The Paul Group’s Strategic Solutions

The Paul Group operates as a seasoned strategic partner for residents in Florida, Illinois, who demand more than a generic insurance policy. We specialize in providing the structural integrity required to protect a family’s financial future. Our firm utilizes a “No Medical Exam” methodology, which simplifies the qualification process for immediate coverage. This approach removes the traditional barriers of clinical screenings, allowing for a seamless transition into a protected state. We believe in disciplined intervention. This means we identify potential fiscal gaps before they become liabilities for your heirs.

Understanding how to pre-plan my funeral financially involves looking beyond the immediate cost. It requires a holistic view of estate preservation. Our team brings an air of quiet confidence to every consultation, ensuring that your most complex organizational challenges are met with intellectual rigor. We don’t just facilitate transactions; we build sustainable frameworks for peace of mind.

Bespoke Quality: Tailoring Plans for Florida, Illinois Seniors

We don’t provide off-the-shelf solutions. The Paul Group curates policies from a select group of top-tier carriers to find the exact fit for your lifestyle. Our methodology focuses on the intersection of operational systems and human reassurance. We prioritize fixed rates that never increase, ensuring your premium remains stable regardless of your age or future health status. By securing a plan now, you insulate your estate from the projected 3.4% annual increase in funeral costs observed over the last decade. This strategic alignment ensures that the value of your coverage keeps pace with economic shifts.

Next Steps: Your Executive Briefing

The path to a secure legacy begins with a diagnostic evaluation of your current standing. We invite you to a no-obligation consultation designed to diagnose your specific financial needs. This executive briefing provides the clarity necessary to move from a state of complexity to one of order. You’ll learn exactly how to pre-plan my funeral financially using tools that offer long-term stability. A well-engineered plan is the ultimate gift of peace. It ensures your family experiences a structured, dignified transition rather than a financial crisis. Connect with a Wise Advisor at The Paul Group today to begin your transformation.

Securing Your Legacy Through Strategic Alignment

Navigating the Florida, Illinois funeral landscape in 2026 requires a disciplined approach to risk management and cost optimization. By establishing a clear methodology today, you eliminate the ambiguity that often surrounds end-of-life expenses. Understanding how to pre-plan my funeral financially isn’t merely a logistical task; it’s a profound act of stewardship that protects your family from future market volatility. The Paul Group has served seniors with sophisticated expertise since 2009, providing the intellectual rigor necessary to align your final wishes with sustainable financial structures.

Our firm prioritizes your peace of mind through a curated selection of instruments tailored to your unique needs. We offer immediate coverage options and fixed rates that ensure your plan remains resilient against inflation. For qualified applicants, our process is streamlined and requires no medical exams, reflecting our commitment to efficient, high-level service. You’ve spent years building your foundation, and you deserve a partner who values structural integrity. Take the first step toward organizational clarity and financial peace. Request Your Strategic Final Expense Briefing today. It’s your time to lead with confidence and provide your loved ones with a future defined by certainty.

Frequently Asked Questions

Is it better to pre-pay a funeral home or buy life insurance in Florida, Illinois?

Opting for life insurance generally offers superior financial flexibility compared to pre-paying a specific facility. While pre-paying locks in current service rates, it often creates a rigid arrangement that lacks portability if you relocate. A curated life insurance policy provides a liquid death benefit that your beneficiaries can deploy according to your exact directives. This methodology ensures your capital remains accessible while providing the necessary coverage for your final arrangements.

How much does the average funeral cost in Florida, Illinois in 2026?

The National Funeral Directors Association projected average cost for a funeral with burial and viewing is approximately $8,300, excluding vault and cemetery fees. In regions like Florida and Illinois, these costs often escalate by 3% to 5% annually due to inflationary pressures. Understanding how to pre-plan my funeral financially requires accounting for these macro-economic trends to ensure your coverage remains sufficient. Strategic planning involves analyzing these data points to build a sustainable financial shield.

Can I pre-plan my funeral if I have existing health conditions?

You can absolutely pre-plan your funeral regardless of your current medical status. Guaranteed issue policies and simplified issue products are specifically engineered for individuals with chronic conditions or historical health challenges. These instruments eliminate the barrier of medical underwriting, ensuring that 100% of applicants can secure a baseline of protection. Our group specializes in identifying the specific carriers that offer the most robust terms for your unique health profile and long-term stability.

What is the FTC Funeral Rule and how does it protect me in Florida, Illinois?

The FTC Funeral Rule mandates that providers give you an itemized General Price List before you see any merchandise. This federal regulation empowers you to purchase only the specific services you desire, rather than being forced into bundled packages. In Florida and Illinois, this transparency is a critical component of your consumer rights. It allows for the optimization of your budget by ensuring every dollar spent aligns with your personal values and strategic goals.

What happens to my pre-paid funeral plan if the funeral home closes?

State laws in Florida and Illinois require funeral homes to place pre-paid funds into a regulated trust or insurance policy. This structural safeguard ensures that your assets are protected even if the business ceases operations or undergoes a corporate transformation. Your contract typically includes a portability clause, allowing the transition of the plan to a different provider. We recommend verifying that your funds are held in an arms-length financial institution to maintain the highest security.

How does Final Expense Insurance differ from traditional Term Life Insurance?

Final Expense insurance is a permanent whole life policy designed for smaller face amounts, whereas Term Life provides temporary coverage for a specific duration. Final Expense policies build cash value and remain active as long as premiums are paid, providing a permanent solution for end-of-life costs. Term life is often used for income replacement during peak earning years and eventually expires. Selecting the right instrument requires a holistic view of your long-term financial architecture.

Can my family use the insurance money for things other than the funeral?

Yes, beneficiaries receive the death benefit as a tax-free lump sum and can use the funds for any financial obligation. While the primary intent is often funeral costs, the money can settle outstanding medical bills, legal fees, or credit card debt. This versatility is a core reason why learning how to pre-plan my funeral financially through insurance is a superior strategy. It provides a multi-purpose safety net that stabilizes your family’s position during a transition.

Is a medical exam required for burial insurance with The Paul Group?

No medical exam is required for the burial insurance programs we curate for our clients. Our methodology focuses on simplified underwriting that relies on a series of health questions rather than invasive physical examinations or blood work. This streamlined approach accelerates the approval process, often providing coverage within 24 to 48 hours. We prioritize efficiency and accessibility, ensuring your strategic plan is implemented without the friction of traditional insurance bureaucracy.

Leave a Reply