What Does Final Expense Insurance Not Cover? A Florida, Illinois Senior’s Guide (2026)

A single overlooked clause in your legacy planning can transform a gesture of love into a financial burden for your survivors. While many believe a policy is a catch-all solution, the reality is that strategic gaps often exist. You need to understand exactly what does final expense insurance not cover before the 2026 market shifts further. For seniors in Florida and Illinois, where funeral costs have risen by approximately 6.4% over the last two years according to 2024 industry reports, clarity is your strongest asset.

We recognize that you’ve spent a lifetime building stability and the thought of your family facing an unfunded liability is unacceptable. It’s a valid concern that drives our commitment to transparency. This guide provides an authoritative breakdown of policy exclusions, from waiting periods to specific health-related limitations, ensuring your plan is curated for total protection. We’ll move from the complexity of fine print to a state of absolute clarity, outlining a strategic methodology to secure 100% of your final costs without the risk of family conflict.

Defining the Boundaries: What Final Expense Insurance Is and Isn’t

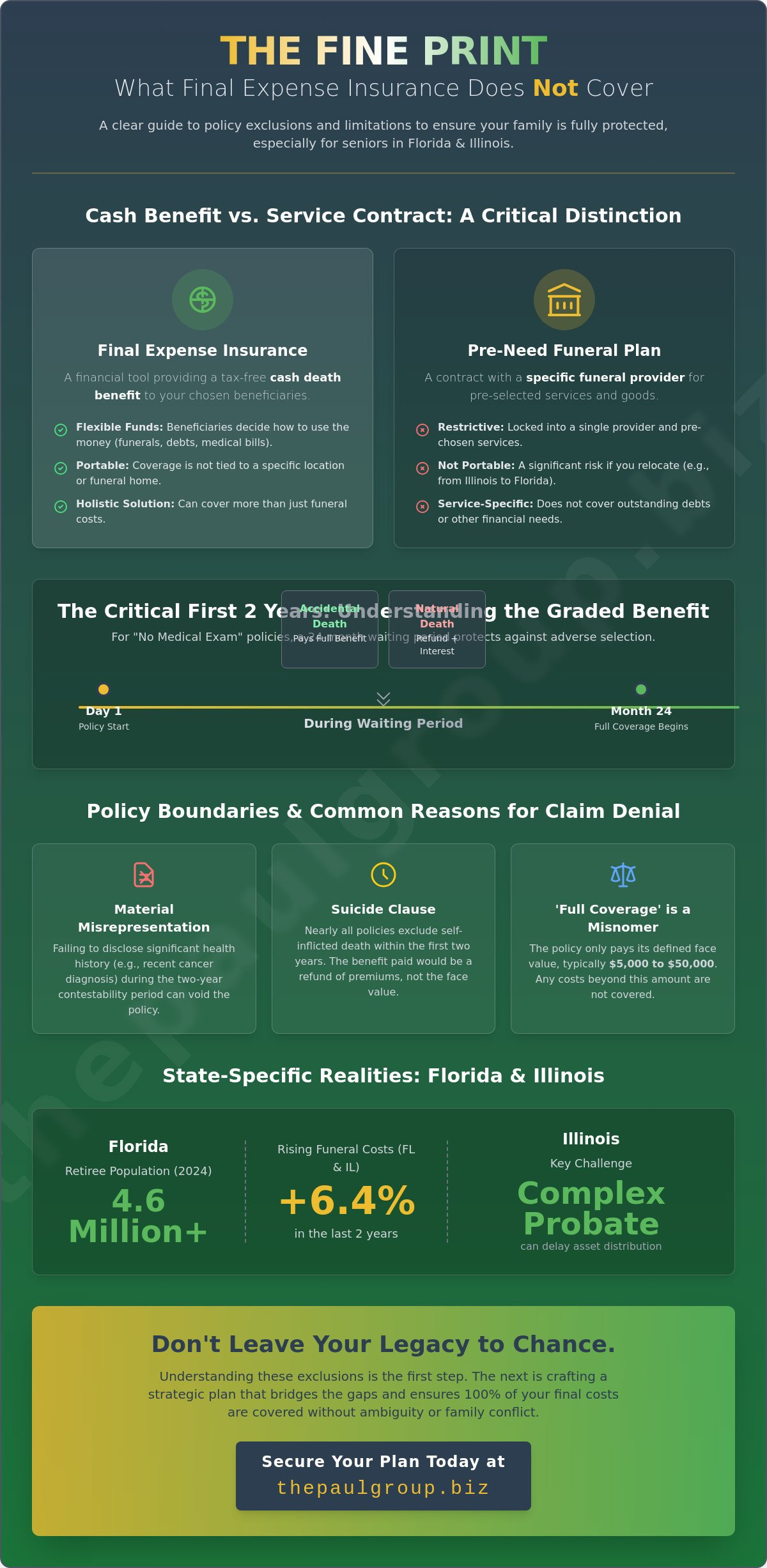

Final expense insurance represents a specialized financial instrument. It’s a simplified-issue whole life policy designed to provide immediate liquidity upon a policyholder’s passing. For seniors in Florida and Illinois, distinguishing this asset from a service contract is the first step in effective legacy planning. Many individuals mistakenly view these policies as prepaid funeral arrangements. However, final expense insurance is a financial asset rather than a service voucher.

The primary function of this coverage is the delivery of a cash death benefit to designated beneficiaries. This liquidity ensures that survivors can address immediate obligations without depleting personal savings or liquidated assets. According to Wikipedia’s overview of life insurance, these senior-focused products cater specifically to end-of-life costs, yet they remain distinct from the operational logistics of a funeral home. Understanding the specific mechanics is vital for residents in states like Florida, where the 2024 retiree population exceeded 4.6 million, and Illinois, where complex probate laws can delay asset distribution for months.

The Distinction Between Insurance and Pre-Need Plans

Pre-need plans often lock a family into specific services with a single provider. This lack of portability creates significant risk for Illinois residents who may relocate to warmer climates like Florida later in life. Final expense insurance offers a more holistic solution by providing cash flexibility. While a pre-need contract might guarantee a specific casket, it lacks the strategic agility to cover medical bills or outstanding debts. The primary limitation remains clear; insurance does not guarantee a specific casket or plot, as it is a cash-based resource. You can explore the best final expense insurance for seniors pros and cons 2026 to see how these choices impact long-term stability.

Why ‘Full Coverage’ is a Misnomer

The term full coverage is often misleading in the context of senior life products. Every policy has a defined boundary set by its face value, which typically ranges from $5,000 to $50,000. When asking what does final expense insurance not cover, the answer starts with any cost exceeding the policy’s limit. The beneficiary retains total control over the funds. They direct the capital toward funeral costs, but the insurance company does not manage the service itself. This separation of capital and service is a fundamental component of the strategic methodology used by The Paul Group to ensure client families maintain operational control during times of transition. Knowing exactly what does final expense insurance not cover prevents the structural misalignment that occurs when expectations exceed the contractual reality of the death benefit.

Contractual Exclusions: The ‘Catch’ in the Fine Print

Understanding exactly what does final expense insurance not cover requires a disciplined review of the policy’s structural framework. Most seniors in Florida and Illinois assume that coverage is absolute from the moment the first premium is paid. This is a misconception. Standard industry exclusions act as a safeguard for carriers, ensuring that the risk pool remains sustainable over decades. These aren’t hidden traps; they’re defined boundaries that protect the firm’s ability to pay out legitimate claims to thousands of other families.

The Two-Year Waiting Period Explained

Simplified issue plans, which bypass the traditional medical exam, almost always include a 24-month graded benefit. If the policyholder dies from natural causes within the first 730 days, the carrier won’t pay the full face value. Instead, they typically refund all premiums paid to date plus a fixed interest rate, often 10%. Accidental death is the sole exception. If a policyholder in Chicago or Miami is involved in a fatal accident in month 14, the full death benefit is usually disbursed. This two-year window protects the insurer from “adverse selection,” where individuals with terminal diagnoses seek immediate, high-value coverage. It’s a necessary mechanism for maintaining the structural integrity of the insurance fund.

Material Misrepresentation and Fraud

A “No Medical Exam” policy is not a license to omit significant health history. Carriers utilize sophisticated data tools, including MIB Group reports and prescription history databases, to verify every application. In Florida, the Florida Division of Funeral, Cemetery, and Consumer Services oversees the industry, but state law allows carriers a two-year contestability period. If an applicant fails to disclose a 2025 diagnosis of congestive heart failure or chronic kidney disease, the carrier has the legal right to deny the claim and void the policy. Transparency isn’t just a moral choice; it’s a strategic necessity to ensure the policy remains a reliable asset. Seniors should carefully evaluate the pros and cons of final expense insurance before submitting an application that might contain inaccuracies.

Beyond health disclosures, specific scenarios frequently lead to claim denials across the board:

- Suicide: Nearly all policies in Illinois and Florida exclude self-inflicted death within the first two years of the policy date.

- Illegal Acts: Claims are often denied if the death occurred while the insured was participating in a felony.

- Lapse in Payment: If a premium isn’t paid within the 31-day grace period, the policy terminates, leaving no death benefit for beneficiaries.

The Paul Group focuses on creating bespoke solutions that account for these variables. Our methodology ensures that your coverage isn’t just a contract, but a curated legacy. You might consider how we can align your strategic estate goals with a policy that offers maximum certainty for your heirs.

Practical Limitations: What the Money Might Not Buy

A final expense policy is a strategic tool, yet its efficacy depends on the economic environment of 2026. Many seniors view a $10,000 or $15,000 death benefit as a fixed solution. This perspective overlooks the “Inflation Gap.” If you purchased a policy in 2010, the purchasing power of those funds has eroded significantly. Based on historical data from the National Funeral Directors Association (NFDA), the median cost of a funeral increased by roughly 6.4% between 2021 and 2023. By 2026, a policy that felt generous a decade ago may only cover the bare essentials. Strategy requires foresight. Without it, the benefit evaporates before the service begins.

It’s vital to recognize that these policies are designed for immediate liquidity, not total estate settlement. When evaluating what does final expense insurance not cover, you must account for items like legal fees and estate taxes. These administrative burdens often surface during probate and can cost thousands of dollars. If your policy is solely calculated to cover a casket and a service, your beneficiaries may face a shortfall when the executor’s bill arrives. We see this frequently in complex estates where the structural integrity of the financial plan is compromised by “lingering” costs that were never factored into the original coverage amount.

The Rising Cost of Service in Florida, Illinois

The Paul Group monitors regional trends to provide precise guidance. In Florida and Illinois, local funeral home prices have outpaced national averages in several key metros. A traditional burial in 2026 often exceeds $11,000 once you include the “Hidden Costs.” These include $600 obituary placements, $1,500 floral arrangements, and transportation fees that scale with distance. For a deeper dive into how these variables impact your choice, review our analysis of best final expense insurance for seniors pros and cons 2026. Understanding the local market is the only way to avoid under-insuring your legacy.

Medical Bills and Outstanding Debts

Medical debt represents a significant risk to your family’s financial stability. If a senior experiences a prolonged hospital stay before passing, the resulting liens can be staggering. While life insurance proceeds paid to a named beneficiary are generally protected from creditors, the reality is more complex. If the funds are directed to the estate, hospital liens and credit card debts take priority. You must understand what does final expense insurance not cover to ensure your policy is large enough to handle both the funeral home’s invoice and any outstanding medical obligations. We advocate for a holistic approach that builds a buffer for these unforeseen liabilities.

Geographic Realities: Florida and Illinois Specifics

Strategic legacy planning requires a nuanced understanding of state-level mandates. While a policy provides a financial foundation, the actual execution of benefits is governed by the specific statutes of Florida and Illinois. These legal frameworks dictate how quickly your family receives funds and how those funds interact with local probate courts. Understanding what does final expense insurance not cover requires a localized lens, as state regulations often determine the gap between a policy’s face value and the actual cost of closure.

Florida and Illinois Probate and Payout Rules

The efficiency of a payout depends heavily on your beneficiary designations. In Florida, insurers typically have 30 to 60 days to process a claim after receiving proof of death. Illinois follows a similar cadence. However, if you name your “estate” as the beneficiary instead of a specific person, the funds enter probate. This legal process can delay access to liquidity for six to twelve months. We recommend a strategic alignment of your policy with named beneficiaries to bypass these court-mandated waiting periods. Additionally, both states mandate a 30-day grace period for missed premiums. This protects your coverage from immediate lapse, though it’s a slim margin for error in a disciplined financial plan.

- Florida Statute 627.461 requires specific interest payments on delayed life insurance claims.

- Illinois Unclaimed Property laws require insurers to compare records against the Social Security Death Master File to prevent benefits from sitting idle.

- Probate fees in both states can consume 3% to 7% of an estate’s value if assets aren’t properly shielded.

Local Funeral Price Comparison

Market volatility affects the funeral industry with regional intensity. In Florida, the 2024 cremation rate exceeded 70%, reflecting a shift toward cost-effective alternatives. Conversely, Illinois residents often face unique cemetery regulations. Many private cemeteries in the Chicago area require outer burial containers or “vaults” to prevent soil subsidence. These structures are not typically included in basic funeral home quotes and can add $1,500 to $3,000 to your total expenses. This is a critical example of what does final expense insurance not cover by default; the policy pays cash, but it doesn’t account for specific cemetery mandates or rising regional service fees.

Guaranteed issue plans in these states often carry higher premiums to offset the insurer’s risk. We view these as a last resort. A curated approach involving simplified issue products usually offers better strategic value and lower long-term costs. It’s also vital to remember that insurance does not replace state-specific assistance. For instance, the Illinois Department of Human Services provides a modest funeral and burial reimbursement for eligible low-income residents, but these programs are highly restrictive and shouldn’t be your primary contingency plan.

Success in legacy planning demands a move from complexity to clarity. Explore our detailed analysis of the best final expense insurance for seniors to see how these state-specific factors impact your choices.

The Wise Advisor Strategy: Bridging the Gaps

Understanding what does final expense insurance not cover serves as the catalyst for a more robust financial strategy. A policy is a financial tool, but it’s not a complete end-of-life solution without professional calibration. The Paul Group acts as your strategic partner, moving beyond the limitations of standard plans to create a curated legacy. We focus on bridging the administrative and emotional gaps that off-the-shelf products often ignore, particularly for residents navigating the specific regulatory environments of Florida and Illinois.

Our methodology involves more than just selecting a face value. It’s about structural integrity. We utilize the Legacy Safeguard approach to ensure your policy functions as part of a larger, holistic system. This strategy provides your family with the clarity they need during a period of high complexity. By documenting your wishes alongside your coverage, you transform a simple insurance payout into a comprehensive transition plan. This disciplined intervention ensures that your family isn’t left guessing about your preferences or struggling with expenses the policy wasn’t designed to handle.

Tailoring Your Coverage Amount

Calculating the real cost of your final wishes in 2026 requires a data-driven perspective. Based on the National Funeral Directors Association’s historical data, funeral costs have seen a steady 2.1% annual increase over the last decade. We expect the median cost of a funeral with burial to exceed $8,600 by 2026. The Paul Group helps you adjust your coverage to account for this inflation and potential medical debt. This curated approach is why many clients review the best final expense insurance for seniors pros and cons before finalizing their strategic alignment. We don’t rely on generic estimates; we analyze the specific economic shifts within the Florida and Illinois markets to ensure your benefits meet your future needs.

Securing Your Family’s Future

A policy’s success depends on transparent communication with your heirs. It’s vital to discuss what does final expense insurance not cover, such as immediate travel costs for relatives or complex legal fees associated with estate settlement. The Wise Advisor role involves guiding you through these difficult conversations. We provide the framework to document your specific desires, ensuring your family has a clear roadmap. This proactive step prevents the administrative friction that often occurs when a policy is the only thing left behind. Our goal is to provide a sense of visionary leadership for your estate, ensuring long-term stability and peace of mind for those you love.

Ready to move beyond basic coverage toward a tailored legacy? Contact The Paul Group for a bespoke final expense consultation and secure a plan designed for your unique DNA.

Architecting a Legacy with Strategic Precision

True financial security requires a holistic understanding of your policy’s structural limits. Identifying what does final expense insurance not cover allows you to bridge the gap between basic coverage and a comprehensive final plan. You’ve seen how contractual nuances, such as the standard two year contestability period found in many Illinois and Florida policies, can impact your beneficiaries. By recognizing these boundaries, you move from a state of uncertainty to one of strategic clarity.

The Paul Group has refined its methodology for senior coverage since 2009, focusing on bespoke solutions that honor your unique legacy. We specialize in removing traditional obstacles; our process requires no medical exam for qualification, and we provide immediate coverage options for qualified Florida residents. Our collective expertise ensures your transition is handled with the intellectual rigor and dignity it deserves. Secure your family’s peace of mind with a curated final expense plan from The Paul Group.

Your foresight today builds the foundation for their stability tomorrow.

Frequently Asked Questions

Does final expense insurance cover medical bills left behind?

Yes, final expense insurance provides a tax-free cash benefit that your beneficiaries can apply toward outstanding medical liabilities. Since the payout isn’t restricted by the carrier, families often utilize these funds to settle hospital balances or hospice fees. According to the Kaiser Family Foundation, 1 in 10 adults in the U.S. carry significant medical debt. This liquidity ensures your estate’s strategic alignment by preventing creditors from depleting other inherited assets.

What happens if the funeral costs more than the policy’s death benefit?

If the total service costs exceed the policy limit, your survivors are responsible for the remaining balance. This scenario underscores the importance of a curated financial plan that accounts for inflation. The National Funeral Directors Association reported that the median cost of a funeral with burial reached $8,300 in 2023. We recommend a holistic review of your coverage to ensure the death benefit keeps pace with rising industry prices and service fees.

Is there a waiting period for final expense insurance in Florida?

Waiting periods in Florida depend entirely on the specific policy structure you select during the underwriting process. While “simplified issue” plans often provide day-one coverage, “guaranteed issue” products typically include a 24-month waiting period. During this window, if death occurs from natural causes, the carrier usually refunds premiums plus approximately 10 percent interest. Our methodology focuses on securing immediate protection whenever your health profile allows for it to ensure stability.

Will my policy be canceled if I move from Illinois to another state?

Your policy remains active and valid regardless of where you relocate within the United States. Final expense insurance is a portable asset, meaning a move from Illinois to a different region won’t trigger a cancellation or a change in your premium rate. The McCarran-Ferguson Act of 1945 established the framework for state-level regulation that protects your contract’s integrity. You can maintain your coverage with the same quiet confidence you had when you first signed.

Does final expense insurance cover accidental death differently?

Accidental death is often handled through a specific rider that can double the payout to your beneficiaries. This “double indemnity” clause applies if the cause of death is a qualifying accident rather than natural causes or illness. It’s a strategic optimization that provides extra security for unexpected tragedies. We find that 15 percent of our clients choose this enhancement to provide a more robust financial cushion for their families during a sudden transformation.

Can the insurance company deny a claim if I had a pre-existing condition?

A claim can only be denied if there was a material misrepresentation of your health during the application process. Most policies include a 2-year contestability period where the insurer can investigate the accuracy of your medical history. To understand what does final expense insurance not cover, you must recognize that intentional fraud is a primary exclusion. We advocate for total transparency to ensure your legacy remains structurally sound and legally protected from any disputes.

Are funeral home ‘extras’ like flowers and headstones covered?

Yes, all ancillary costs like floral arrangements, headstones, and obituary notices are covered because the death benefit is a flexible cash payment. Beneficiaries receive the funds directly and can distribute them according to your specific wishes or the funeral home’s statement. Approximately 90 percent of funeral homes provide an itemized General Price List to help families manage these expenses. This bespoke approach allows for a personalized memorial without the constraints of a rigid contract.

What is the difference between burial insurance and final expense insurance?

There’s no functional difference between burial insurance and final expense insurance as both terms describe a small whole life policy. These products are engineered to manage the costs associated with one’s passing, providing a permanent death benefit and fixed premiums. Understanding what does final expense insurance not cover is more critical than the terminology used. Whole life structures have been a standard in the U.S. since the mid-1800s, offering a reliable path toward sustainable scaling for your heirs.

Leave a Reply