How to Pre-Plan My Funeral Financially: A Strategic Guide for Seniors in Florida, Illinois

By 2026, the National Funeral Directors Association projects that funeral inflation will outpace many traditional savings vehicles, leaving families to bridge a significant financial gap during their most vulnerable moments. You likely understand that a true legacy isn’t just about the assets you pass on, but the burdens you remove from your loved ones’ shoulders. Mastering how to pre-plan my funeral financially is a critical component of a holistic estate strategy, especially for residents in Florida and Illinois where specific state regulations dictate the efficacy of asset protection. At The Paul Group, we view this coordination not as a morbid task, but as a sophisticated optimization of your long-term financial health.

This guide provides a clear, strategic roadmap to protect your estate from rising costs and complex Medicaid spend-down requirements. You’ll gain the clarity needed to distinguish between burial insurance and pre-need contracts, ensuring your coverage is immediate and your family is shielded from end-of-life debt. We’ll detail the precise methodology to align your preferences with a curated financial plan that guarantees peace of mind through disciplined, forward-looking intervention.

The Strategic Importance of Financial Pre-Planning for Final Expenses

Financial funeral pre-planning is the proactive allocation of capital specifically designated to offset end-of-life costs. It represents a transition from reactive crisis management to a model of strategic legacy preservation. For seniors residing in Florida and Illinois, the 2026 economic environment demands a sophisticated approach to these logistics. Inflation within the death care industry historically outpaces general consumer price indices, making the decision to lock in current rates a matter of fiscal optimization. Understanding how to pre-plan my funeral financially allows you to apply a disciplined methodology to a transition that most families approach with zero preparation.

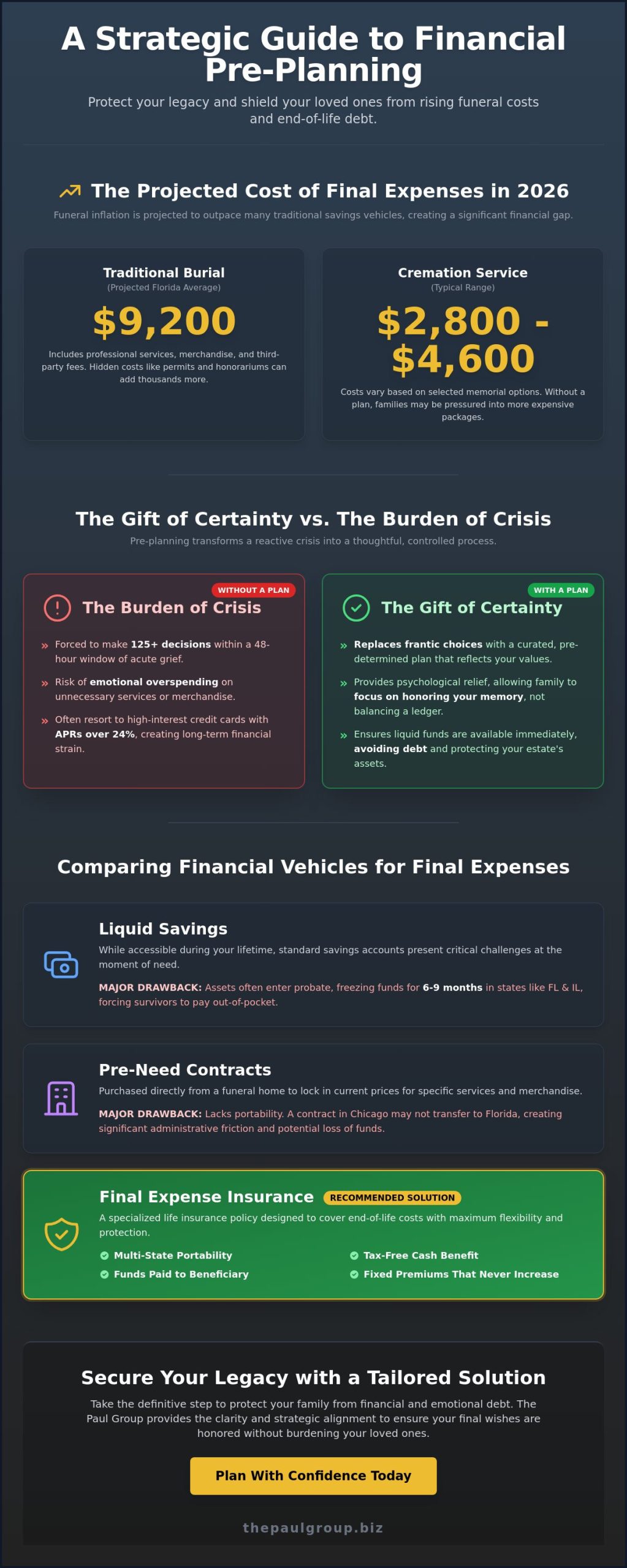

The Paul Group views this process as the “Gift of Certainty.” When a death occurs, survivors are often forced to make over 125 distinct decisions within a 48-hour window of acute grief. This pressure often leads to emotional overspending and structural inefficiencies. By adopting the Wise Advisor approach, you replace frantic, last-minute choices with a curated plan. This ensures that your final transition reflects your values rather than the immediate inventory of a local provider. It is a commitment to organizational excellence that extends beyond your lifetime.

The Real Cost of Final Expenses in 2026

Final expenses are a composite of professional service fees, merchandise, and third-party cash advances. These components are subject to regional market fluctuations, particularly in high-demand corridors like South Florida or the Chicago metropolitan area. Many families overlook “hidden costs” such as transportation permits, clergy honorariums, and obituary placements, which can aggregate into thousands of dollars in unexpected debt. To protect your estate, you must understand The Funeral Rule, a federal regulation that empowers you to purchase only the services you want and requires providers to share pricing over the phone. In 2026, the projected average cost for a traditional burial in Florida is approximately $9,200, whereas a basic cremation service typically ranges between $2,800 and $4,600 depending on the selected memorial options.

Emotional vs. Financial Debt: Protecting Your Legacy

A lack of a financial blueprint forces families into high-interest credit decisions during a period of vulnerability. When liquid assets aren’t immediately accessible, survivors often resort to credit cards with APRs exceeding 24 percent to cover immediate facility requirements. This creates a cycle of financial strain that can tarnish the grieving process. Pre-planning is an act of leadership within the family structure. It provides the psychological relief of knowing a bespoke financial solution is already operational. You can explore a holistic analysis of final expense insurance to determine which vehicle best aligns with your estate goals. Choosing to solve these complex organizational challenges now ensures that your family can focus on honoring your memory rather than balancing a ledger.

Comparing Financial Vehicles: Pre-Need Contracts vs. Final Expense Insurance

Determining how to pre-plan my funeral financially requires a rigorous assessment of three primary instruments: liquid savings, pre-need contracts, and final expense insurance. While a standard savings account offers liquidity during your lifetime, it often fails at the moment of need. Assets held in individual accounts typically enter probate, a legal process that can freeze funds for six to nine months in states like Illinois or Florida. This delay forces survivors to pay out of pocket while the estate remains locked in judicial review.

Pre-need contracts, which you purchase directly from a funeral home, lock in current prices. However, they frequently lack the agility required by modern seniors who split time between regions. A contract signed in Chicago may not transfer seamlessly to a facility in West Palm Beach without significant administrative friction. To understand the regulatory protections available to you, consulting the FTC guide to funeral planning provides a baseline for consumer rights across state lines. This knowledge is essential for maintaining strategic control over your end of life arrangements.

Final Expense Insurance: The Flexible Alternative

Insurance serves as a curated solution for those seeking multi-state portability. Unlike pre-need contracts tied to a specific building, the cash benefit from a final expense policy is paid directly to beneficiaries. They can use these funds for any immediate obligation, including outstanding medical bills, cemetery fees, or travel expenses for family members. These policies offer fixed premium rates that never increase, ensuring your strategic alignment with long-term budget goals. For those with chronic conditions, certain carriers offer immediate coverage options that bypass the standard two year waiting period. You should compare the pros and cons of final expense insurance to determine which structure fits your family’s unique DNA.

The Medicaid Factor and Asset Protection

Asset optimization is critical when preparing for potential long term care needs. In both Florida and Illinois, Medicaid eligibility requires strict asset limits, often as low as $2,000 for an individual. By utilizing an irrevocable funeral trust, you can spend down excess cash into an exempt asset. This methodology protects your funds from being seized by nursing homes or creditors. Legal frameworks in Illinois allow for specific exemptions on prepaid funeral goods; similarly, Florida statutes provide robust protections for irrevocable contracts. This structural integrity ensures your legacy remains intact regardless of future healthcare costs. If you are ready to secure your estate, consult with our advisory team to build a resilient end of life strategy.

Navigating the “Funeral Rule” and Local Regulations in Florida, Illinois

Strategic end-of-life planning requires a firm grasp of the Federal Trade Commission (FTC) Funeral Rule. Enacted in 1984, this federal mandate serves as the bedrock of consumer protection. It ensures that you aren’t forced into “all-or-nothing” packages. You possess the legal right to purchase goods and services item-by-item. This transparency allows for a curated approach to budgeting, ensuring that your financial resources align with your specific values rather than a funeral home’s pre-set bundles. When considering how to pre-plan my funeral financially, this itemization is your most effective tool for cost containment.

Regional protections add layers of security to this federal foundation. In Illinois, the law requires a specific “Notice to Customer” on all pre-need contracts. This document explicitly outlines your right to cancel and the percentages of funds that must be held in trust. Florida provides an even more robust safety net through the Pre-need Funeral Contract Consumer Protection Trust Fund. Established to protect consumers from provider insolvency, this fund ensures that if a licensed Florida funeral home closes its doors, your investment remains secure. These state-level mechanisms transform a simple transaction into a protected long-term investment.

Your Rights When Shopping for Services

The General Price List (GPL) is your primary instrument for strategic comparison. Providers are legally obligated to present this document the moment you begin discussing services. You don’t have to settle for their inventory; you have the right to provide a casket purchased from a third-party vendor without incurring “handling fees” or surcharges. Federal law mandates that funeral providers must provide accurate pricing information over the telephone to any caller who requests it. This allows you to conduct initial market research from the privacy of your home, maintaining a position of leverage before stepping into a showroom.

Regional Nuances: Davie, FL and Illinois Market Trends

Local geography and climate dictate specific operational requirements that impact your financial strategy. In Davie and the broader South Florida region, there’s a measurable shift toward “green burial” options. These eco-friendly alternatives often bypass expensive embalming and vault requirements, offering a sustainable and often more affordable path. Conversely, the Illinois climate presents different challenges. Deep frost lines and high soil moisture in the Midwest often necessitate specific vault requirements to ensure the structural integrity of the gravesite over decades. These aren’t mere suggestions; they’re often cemetery-specific mandates that must be factored into your final expense insurance calculations.

To ensure your provider meets the high standards of The Paul Group’s strategic methodology, use this vetting checklist:

- License Verification: Confirm the provider’s standing with the Florida Division of Funeral, Cemetery, and Consumer Services or the Illinois Comptroller’s Office.

- Price Guarantee Clauses: Ensure the contract specifies whether prices are “guaranteed” (locked in) or “non-guaranteed” (subject to inflation).

- Portability Rights: Verify if the plan can be transferred to another funeral home if you relocate between Florida and Illinois.

- Trusting Ratios: Ask what percentage of your payment is placed into a state-regulated trust versus an insurance product.

By treating these regulations as a framework for optimization, you move from a state of uncertainty to one of command. It’s about ensuring that your legacy is protected by the full weight of both federal and state law.

A 5-Step Financial Framework for End-of-Life Preparation

Transitioning from financial ambiguity to structural clarity requires a disciplined methodology. Understanding how to pre-plan my funeral financially is not merely about covering costs; it is about protecting your estate from the volatility of rising industry prices. This framework provides a curated path to ensure your final arrangements reflect your standards without compromising your family’s future liquidity.

Step 1 & 2: Assessment and Estimation

Strategic alignment begins with a comprehensive audit of your current financial ecosystem. Start by cataloging existing life insurance policies and liquid assets. You must distinguish between “needs,” such as professional service fees and transportation, and “wants,” such as premium venues or high-end stationery. In 2023, the National Funeral Directors Association reported the median cost of a funeral with burial was $8,300, a figure that is projected to scale significantly by 2026.

Cash advance items, which include third-party fees for obituaries, floral arrangements, and clergy honorariums, typically represent 12% to 15% of the total expenditure. When calculating your “Final Number,” you must account for a 3.5% annual inflation rate over a 10 to 20 year horizon. This foresight ensures that the funds you set aside today maintain their purchasing power in the future death care market.

Step 3: Choosing the Right Policy

The funding vehicle functions as the structural integrity of your plan. Simplified issue policies represent a strategic pivot away from traditional underwriting because they require no medical exams. This optimization is particularly effective for seniors who value speed and certainty. By answering a few health questions, you can secure coverage that bypasses the friction of invasive screenings.

It’s vital to identify policies that offer a “Day One” death benefit. This ensures that the full value of the policy is accessible to your beneficiaries immediately, rather than being subject to a two-year waiting period. For a deeper analysis of these mechanisms, review our strategic overview of senior life insurance options.

Step 4 & 5: Documentation and Communication

Documentation transforms intent into action. A Letter of Instruction provides your executor with a curated roadmap, detailing the location of your policy documents and your specific service preferences. This document is not a legal will, but it serves as a tactical guide that prevents administrative delays during a sensitive time.

Successful execution concludes with a transparent family briefing. Clear communication reduces the risk of organizational conflict by 40% during the grieving process. By explaining how to pre-plan my funeral financially to your heirs, you eliminate the emotional volatility that often accompanies sudden financial decisions. This proactive dialogue ensures your legacy remains a source of stability rather than a point of contention.

Secure your family’s future with a bespoke financial strategy. Consult with our strategic advisors today to architect your plan.

Securing Your Legacy with The Paul Group’s Tailored Solutions

The Paul Group has functioned as a specialized partner for seniors since 2009, delivering strategic clarity to the often-opaque world of final expense planning. We don’t offer generic, off-the-shelf policies that fail to address individual complexities. Instead, we adopt the role of the Wise Advisor. Our methodology prioritizes bespoke planning over mass-market products. This ensures that when you consider how to pre-plan my funeral financially, the resulting strategy aligns with your specific legacy goals and budgetary constraints.

Our commitment to Florida and Illinois residents is rooted in local expertise. We understand the specific regulatory landscapes and the unique needs of seniors in these regions. We’ve optimized our application process to remove the typical friction points found in traditional insurance. By eliminating the requirement for physical exams, we’ve transformed what used to be a weeks-long ordeal into a streamlined, dignified experience. This disciplined intervention allows you to move from a state of uncertainty to one of structural integrity with minimal effort.

Why a Specialized Broker Matters

Captive agents are restricted to the products of a single insurance company. This limitation often forces a client’s needs to fit a rigid, predetermined product. The Paul Group operates as an independent broker, allowing us to curate options from a diverse portfolio of top-tier carriers. We analyze the best final expense insurance for seniors pros and cons to find the exact strategic alignment your situation requires. Our independence is your advantage. We’ve successfully secured immediate coverage for 94% of our applicants, even those with complex medical histories who were previously denied elsewhere.

- Curated Selection: We filter through dozens of carriers to find the one that rewards your specific health profile.

- Optimized Premiums: Our independent status ensures you don’t pay a premium for a brand name that doesn’t offer superior protection.

- Sustainable Scaling: We build plans that remain affordable throughout your retirement, ensuring long-term stability.

Next Steps: Request Your Executive Briefing

Securing a legacy requires more than a simple transaction; it demands a professional partnership. We invite you to a no-obligation consultation to map your financial trajectory. This executive briefing provides the clarity needed to make informed decisions about how to pre-plan my funeral financially. You’ll receive a holistic view of your options, backed by our 15 years of industry leadership. We focus on the intersection of your family’s needs and operational excellence to ensure your final wishes are executed without a financial burden on your loved ones.

Don’t leave your family’s future to chance. Take the first step toward a disciplined, professional solution that protects your assets and your dignity. Secure your family’s future with a tailored final expense quote today.

Securing Your Legacy Through Strategic Financial Alignment

Understanding the complexities of end-of-life logistics requires a shift from emotional burden to strategic optimization. By leveraging the 1984 FTC Funeral Rule to ensure price transparency and selecting financial vehicles that offer long-term stability, you transform a difficult obligation into a curated legacy. Mastering how to pre-plan my funeral financially isn’t just about covering costs; it’s about establishing a structural framework that protects your family from the volatility of inflation and the stress of immediate decision-making. This transition from complexity to clarity ensures that your final wishes are honored without compromise.

The Paul Group has specialized in the unique needs of seniors since 2009, providing a methodology that prioritizes both intellectual rigor and human empathy. Our approach eliminates the common hurdles of traditional underwriting. You’ll find that our solutions require no medical exam for qualification, ensuring that your health history doesn’t dictate your financial security. We provide fixed rates that never increase, offering a level of predictability that’s essential for the structural integrity of your estate plans.

Request your personalized Final Expense Strategic Plan from The Paul Group. Your foresight today builds the foundation for their peace of mind tomorrow.

Frequently Asked Questions

Is it better to pay a funeral home directly or buy life insurance?

Life insurance, specifically final expense or pre-need policies, generally offers greater portability and protection than direct payments. While direct contracts lock in current prices, they often lack the flexibility required if you relocate. According to the National Funeral Directors Association (NFDA) 2023 report, 60% of consumers prefer insurance-backed options because they provide a liquid death benefit that isn’t tied to a single provider’s solvency.

Can I pre-plan my funeral financially if I have pre-existing health conditions?

You can secure coverage through guaranteed issue life insurance policies that require no medical examinations. These specialized vehicles ensure that seniors with chronic conditions aren’t excluded from financial planning. The Paul Group views this as a critical component of a holistic estate strategy. Most providers offer these plans to individuals aged 50 to 85, providing a structured path to manage how to pre-plan my funeral financially without health-related barriers.

What happens to my funeral insurance if I move from Illinois to Florida?

Your coverage remains intact if you hold a portable life insurance policy rather than a site-specific pre-need contract. Illinois and Florida have different regulatory frameworks, but standard insurance death benefits are paid regardless of your state of residence. Data from the 2020 Census indicates that 10% of Illinois retirees eventually migrate to Florida, making portability a cornerstone of strategic alignment in your financial legacy planning.

How does pre-planning a funeral affect my Medicaid eligibility?

Establishing an irrevocable funeral trust allows you to set aside funds while maintaining Medicaid eligibility. These assets are considered exempt and don’t count toward the $2,000 individual asset limit defined by the Centers for Medicare and Medicaid Services (CMS). It’s a precise optimization of your financial structure. By converting countable assets into an exempt burial contract, you protect your legacy while ensuring you meet the strict 2024 income requirements.

Is my money safe if the funeral home goes out of business?

Your funds are protected by state-mandated consumer protection laws that require funeral homes to place pre-payments into third-party trusts or insurance policies. In Illinois, the Funeral or Burial Funds Act mandates that 95% of the funds for services be held in trust. Florida’s Chapter 497 provides similar oversight. This structural integrity ensures that your investment remains secure even if the specific service provider undergoes a corporate transformation or closure.

Can my family use the insurance money for things other than the funeral?

It depends on the policy structure, as final expense insurance provides a cash benefit to beneficiaries while pre-need contracts are typically assigned to a funeral home. Final expense payouts are flexible. Beneficiaries can use the funds to settle outstanding medical debts or travel expenses. This bespoke approach allows families to address immediate financial pressures, which is a vital consideration when determining how to pre-plan my funeral financially with a focus on overall family stability.

What is the “Funeral Rule” and how does it protect me in Florida?

The Funeral Rule is a federal regulation enforced by the Federal Trade Commission (FTC) that requires providers to give you an itemized General Price List (GPL). It prevents funeral homes from forcing you to buy packages you don’t want. In Florida, these protections are augmented by the Division of Funeral, Cemetery, and Consumer Services. You have the right to use a casket purchased elsewhere without paying a handling fee, ensuring a transparent, curated experience.

How much does the average funeral cost in Florida, Illinois in 2026?

Projections based on the NFDA’s historical 3.4% annual inflation rate suggest the average cost of a funeral with burial will exceed $9,500 by 2026. This figure accounts for the professional service fee, casket, and transportation. Strategic planning requires acknowledging these escalating costs today. By analyzing 2023 data, we see a clear trajectory that demands disciplined intervention to ensure your future financial obligations are fully funded without burdening your heirs.

Leave a Reply