Low Cost Burial Insurance: Affordable Plans That Don’t Cut Corners

With the National Funeral Directors Association reporting that median funeral costs reached $8,300 in 2023, projections indicate these expenses will surpass $8,500 by the start of 2026. You likely recognize that leaving your loved ones with an unplanned financial burden is a risk that requires immediate mitigation. However, finding low cost burial insurance often feels like a choice between high premiums and restrictive health requirements that lead to rejection. At The Paul Group, we believe that end-of-life planning requires the same strategic rigor as any high-level financial transition. It’s about more than just a policy; it’s about securing a legacy through disciplined preparation.

You deserve a roadmap that eliminates the confusion between term and whole life insurance while ensuring your rates never increase. We’ve curated a professional checklist designed to help you master these complexities and achieve immediate peace of mind for your beneficiaries. This article details a holistic methodology for 2026 planning, guiding you from policy selection to final execution. We’ll show you how to optimize your coverage so your family is protected by a stable, high-quality plan that respects both your health history and your budget.

Key Takeaways

-

Analyze the macro-economic shifts of 2026 to proactively shield family assets from the rising trajectory of end-of-life expenses.

-

Utilize a curated inventory to align your final wishes with a precise assessment of estate liabilities, ensuring no financial burden is left behind.

-

Learn how to leverage Simplified Issue methodologies to secure low cost burial insurance that offers permanent, fixed-rate protection without a medical exam.

-

Navigate the nuances of regional cost drivers and localized regulations to optimize your coverage for specific state environments.

-

Adopt a disciplined, partnership-driven strategy to streamline the insurance application process and achieve long-term structural integrity for your estate.

Table of Contents

-

Strategic Selection: Finding Low-Cost Burial Insurance Without Compromise

-

Localized Cost Drivers: Navigating Insurance from Texas to Florida

The Financial Architecture of End-of-Life Planning

The fiscal landscape of 2026 presents a unique challenge for senior estate management. Rising costs for end-of-life services have reached a critical threshold, threatening to erode family savings that were intended for legacy rather than liability. A disciplined intervention is required. The Paul Group views final expense insurance as a precision instrument rather than a broad-market commodity. It’s about achieving strategic alignment between your current liquidity and your projected final obligations. Securing low cost burial insurance isn’t merely a defensive move; it’s an optimization of your financial architecture that ensures your assets remain intact for the next generation.

The psychological relief of a curated plan cannot be overstated. When a methodology is in place, the burden of uncertainty shifts from the family to the strategic partner. This transition allows for a focus on human leadership within the family unit, rather than the stress of transactional logistics during a period of grief. Our approach focuses on sustainable scaling of your protection, ensuring that the plan you implement today remains robust against the economic shifts of tomorrow.

Why Traditional Life Insurance Often Fails Seniors

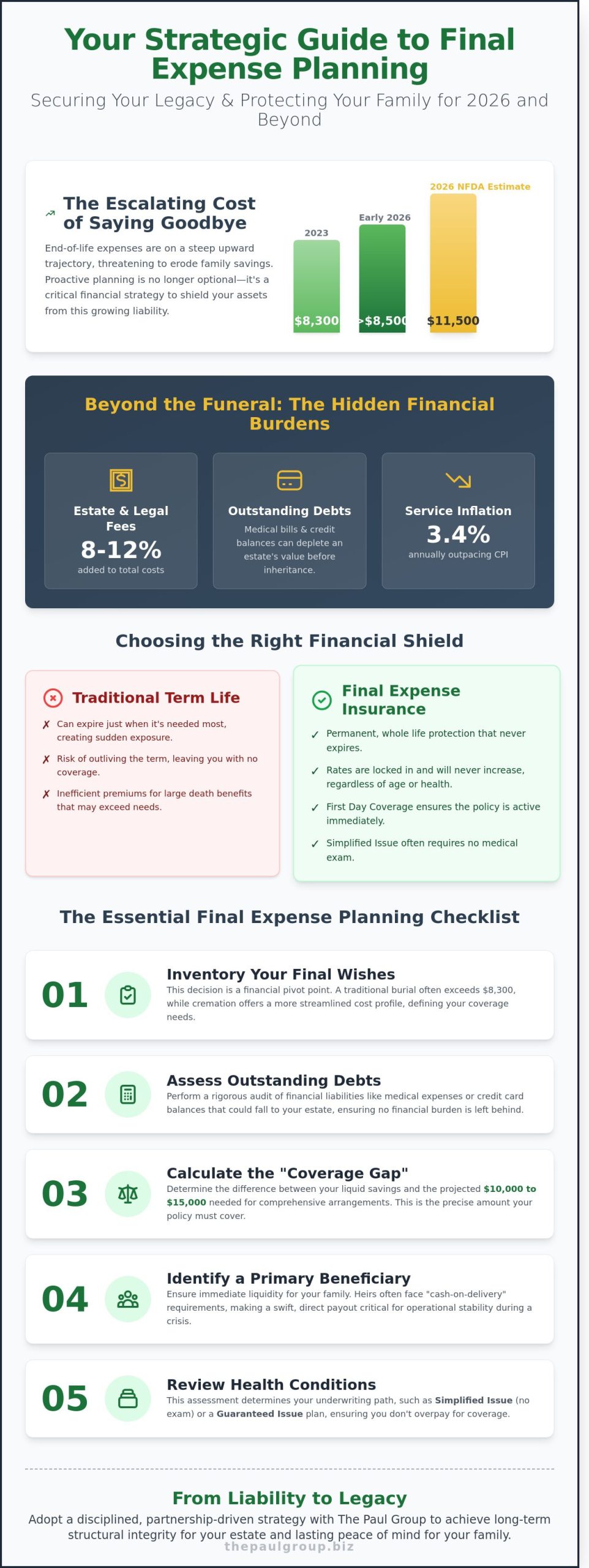

Traditional term policies often expire just when they’re needed most. For individuals over 65, the risk of outliving a 20-year term is a structural flaw that creates sudden, unmanaged exposure. Large death benefits often carry premiums that exceed the actual requirement, leading to capital inefficiency. First Day Coverage offers an efficient methodology for immediate protection, ensuring that the policy is active from the moment the first premium is paid. You can explore the best final expense insurance for seniors pros and cons 2026 to understand how these tailored solutions outperform bloated, traditional products. This level of certainty is essential for a holistic estate strategy.

The Real Cost of Final Expenses in 2026

According to the National Funeral Directors Association (NFDA), the median cost of a funeral with viewing and burial has reached $11,500 in 2026. This figure only represents the core service. Families frequently encounter hidden financial friction points that complicate the settlement process. Legal fees for estate distribution, outstanding medical debt, and probate expenses can add another 8% to 12% to the total financial burden. Inflation in the service sector has outpaced general consumer price indexes by 3.4% annually. Consequently, low cost burial insurance serves as a necessary hedge against future price volatility, locking in a solution before costs escalate further. Our firm prioritizes this type of forward-looking structural integrity to protect your family’s financial DNA.

The Essential Final Expense Planning Checklist for Seniors

Effective preparation requires more than a casual conversation; it demands a rigorous audit of financial liabilities and personal preferences. Seniors must begin by inventorying end-of-life wishes with clinical precision. Choosing between traditional burial and cremation isn’t merely a personal preference. It’s a financial pivot point. National averages for traditional funerals often exceed $8,300, while direct cremation provides a more streamlined cost profile. This distinction helps define the scope of your low cost burial insurance needs.

Strategic planning also involves assessing outstanding debts that might fall to the estate. Medical expenses or lingering credit card balances can deplete an estate’s value before heirs receive their intended inheritance. Calculating the "Coverage Gap" is the next logical step in this methodology. This gap is the difference between liquid savings and the projected $10,000 to $15,000 required for comprehensive final arrangements. Identifying a primary beneficiary ensures immediate liquidity during a crisis. Heirs often face "cash-on-delivery" requirements from funeral homes, making the speed of a policy payout critical for operational stability. Finally, a review of health conditions determines the underwriting path. Whether you qualify for simplified issue or require a guaranteed plan, this assessment ensures you don’t overpay for coverage.

Phase 1: Defining Your Objectives

Success starts with differentiating "needs" from "wants." A "need" is the core capital required for professional services. A "want" is a legacy gift or a curated memorial event. Involving family early reduces friction and ensures your directives are understood. Clear documentation prevents emotional overspending during periods of grief. According to this Forbes Advisor on burial insurance, understanding these distinctions is vital for selecting a policy that mirrors your specific goals. You can explore the best final expense insurance for seniors to see how these objectives align with current market offerings.

Phase 2: Financial Audit

A holistic audit must account for existing institutional resources. The Social Security Administration provides a one-time death payment of exactly $255 to eligible survivors, a figure that has remained stagnant since 1954. This is rarely sufficient for modern requirements. Veterans should verify eligibility for VA burial benefits, which may provide a plot in a national cemetery and a headstone. Once these are factored in, determine a sustainable monthly budget. Securing low cost burial insurance depends on finding a premium that fits within your fixed income without compromising your daily quality of life. If you require a more tailored analysis of your options, our team at The Paul Group can help you architect a sustainable financial plan.

Strategic Selection: Finding Low-Cost Burial Insurance Without Compromise

Securing a legacy requires more than a simple policy purchase; it demands a disciplined assessment of the policy’s structural integrity. According to the Insurance Information Institute, these plans are specifically engineered to manage end-of-life expenses, yet the underlying architecture determines the total cost of ownership. Finding low cost burial insurance isn’t about chasing the lowest introductory rate. It’s about identifying a "Simplified Issue" methodology that aligns with your specific health profile. This approach utilizes data-driven underwriting rather than invasive physical exams, leveraging prescription databases to assess risk instantly.

Simplified Issue policies aren’t inherently more expensive than fully underwritten ones. By removing the need for medical technicians and lab work, carriers reduce their administrative overhead. This efficiency often translates into a 24 to 48-hour approval window. It allows healthy seniors to secure permanent protection without the premium spikes usually associated with high-risk pools. Strategic planning requires a focus on "Whole Life" structures. Unlike term plans that may expire or see price hikes every five years, a whole life structure provides a permanent, non-expiring solution with a guaranteed death benefit.

Avoid plans that feature increasing premiums. These structures are often marketed as budget-friendly options but become prohibitively expensive as you age. A strategic advisor looks for "Immediate Coverage" plans where the full death benefit is available from the first day the policy is active. If a plan is labeled as "Graded" or "Modified," it typically means the full benefit won’t pay out if death occurs within the first 24 months. These are secondary options, only to be utilized when health history precludes immediate coverage.

Simplified Issue vs. Guaranteed Issue

Simplified Issue is the preferred route for seniors with manageable health conditions, such as controlled hypertension or type 2 diabetes. It offers the most competitive rates because the applicant answers a few basic health questions. Guaranteed Issue acts as a strategic last resort, designed for individuals with severe chronic illnesses or terminal diagnoses. While it bypasses all health inquiries, it carries higher premiums and a mandatory two-year waiting period. Simplified underwriting accelerates the approval process by eliminating the traditional 30-day medical review cycle.

Optimizing Your Premium

Achieving a sustainable rate requires a curated selection process. Working with an independent broker provides a holistic view of the market, ensuring you aren’t limited to a single carrier’s rigid criteria. You can analyze the best final expense insurance for seniors pros and cons 2026 to see how different providers treat specific health niches. The primary goal is to secure a "locked-in" rate. This ensures your low cost burial insurance premium remains fixed for life, regardless of future health changes or economic inflation. This price stability creates the long-term structural integrity necessary for a sound estate plan.

Localized Cost Drivers: Navigating Insurance from Texas to Florida

Geography dictates the financial architecture of your final arrangements. While the national median cost for a funeral with viewing and burial reached $8,300 in 2023 according to NFDA data, state-level variables create significant deviations. The Paul Group analyzes these regional fluctuations to ensure your policy remains robust against localized inflation. Selecting low cost burial insurance requires more than a simple premium comparison. It demands a sophisticated understanding of how your physical location influences your beneficiary’s eventual payout. Strategic alignment between your policy and local market realities prevents the structural failure of a legacy plan. It doesn’t just cover costs; it preserves a legacy through disciplined financial engineering.

The Texas and Arizona Landscape

In the Southwest, funeral costs often mirror the rapid population growth observed between 2021 and 2025. Texas presents a specific challenge. Urban burial plot availability in high-growth corridors like Austin or Dallas has decreased by approximately 12% over the last three years, a shift that naturally drives up land costs. Arizona seniors face a different but equally complex dynamic. With a high concentration of retirement communities, the state maintains a saturated insurance market. Our methodology involves navigating these dense markets to find providers that respect Arizona’s strict consumer disclosure laws. This ensures your coverage stays ahead of the 4.5% annual inflation rate typical of Southwestern funeral services.

Coastal Considerations: California and Florida

California and Florida represent the highest levels of complexity for senior planning. In California, cremation rates exceeded 70% in 2022 according to CANA statistics, a trend that allows for more flexible, lower-face-value policies. However, the high cost of living in metro areas like San Francisco or Miami necessitates immediate liquidity for families. For "Snowbirds" who split their time between the Northeast and Florida, policy portability is a critical requirement. Your low cost burial insurance must function seamlessly across state lines. It should account for the 15% price variance often found between different regions. We focus on curated solutions that provide stability, regardless of where the policy is eventually executed.

Expertise is the bridge between complexity and clarity. You can evaluate the strategic advantages of different policy structures by reviewing our analysis of the best final expense insurance for seniors to determine which fits your multi-state lifestyle.

Implementing Your Strategy with The Paul Group

Securing a legacy requires more than a simple transaction; it demands a partnership built on strategic foresight. At The Paul Group, we don’t view final expense planning as a checklist item. We see it as a critical component of your financial structural integrity as you enter 2026. Our Wise Advisor methodology is engineered to dismantle the barriers that often make insurance applications feel like an insurmountable hurdle. We replace that friction with a disciplined, high-level approach that aligns your coverage with your specific health and financial DNA.

Our identity as a collective of experts ensures that you aren’t receiving a one-size-fits-all product. Instead, you benefit from a curated selection process where our team analyzes your unique circumstances to find the optimal fit. This methodology shifts the focus from mere survival to sustainable scaling of your family’s protection. By choosing a partner that values intellectual rigor and bespoke quality, you ensure that your 2026 goals are met with precision and clarity.

Our Commitment to Excellence Since 2009

Since 2009, our firm has maintained a singular focus on the senior final expense market. This 15-year history of stability allows us to operate with a level of authority that younger firms cannot replicate. We curate options across more than 15 different carriers, identifying the specific "low cost" sweet spot that balances affordability with robust benefit structures. This deep industry access is what allows us to secure low cost burial insurance for clients who may have been declined elsewhere.

The application process we’ve developed is designed for executive-level efficiency. We emphasize a no-exam, simplified methodology that respects your time and your privacy. By removing the need for invasive medical tests, we accelerate the timeline from consultation to coverage. You can explore the best final expense insurance for seniors through our lens of transparency, ensuring you understand the mechanics of your policy before you commit.

Taking Control of Your Legacy

Waiting to plan is a strategic risk that carries a 100% probability of increased costs over time. As we approach 2026, the opportunity to lock in rates based on your current age is a diminishing asset. We invite you to move from a state of complexity to one of absolute clarity. Our team is ready to guide you through a bespoke consultation that transforms your concerns into a concrete, actionable roadmap for your family’s future security.

The transition from uncertainty to confidence begins with a single, disciplined step. Don’t leave your family to manage the fallout of an unoptimized estate. It’s time to implement a strategy that reflects your commitment to excellence and your desire for long-term stability.

Next Step: Request a curated final expense briefing from The Paul Group to secure your low cost burial insurance strategy today.

Architect Your 2026 Legacy with Precision

Securing your legacy requires more than a casual glance at final expenses; it demands a disciplined approach to financial architecture. By prioritizing localized cost drivers and utilizing a rigorous planning checklist, you’ve established a foundation for 2026 that protects your family from market volatility. Finding low cost burial insurance is a strategic optimization of your assets, ensuring that your transition doesn’t become a structural burden for those you love. It’s about achieving clarity through disciplined intervention rather than settling for off-the-shelf products that fail to address your specific goals.

The Paul Group has refined this bespoke policy curation since 2009, applying a holistic methodology to the unique needs of seniors. We’ve expanded our local expertise to serve families across 15+ states, providing immediate coverage options that require no medical exam. This level of strategic alignment transforms a complex organizational challenge into a clear, sustainable path forward. You’ll find that our partnership-driven approach offers the reassurance you need to navigate these high-level decisions with quiet confidence and intellectual rigor.

Secure your family’s future with a bespoke insurance strategy from The Paul Group.

It’s time to move from complexity to certainty with a partner who values your long-term stability and structural integrity.

Strategic Planning for 2026: Frequently Asked Questions

Is burial insurance actually cheaper than traditional life insurance?

It’s typically more cost-effective for seniors because the face value is tailored to specific end-of-life expenses rather than broad income replacement. Traditional term policies often require $100,000 minimums, whereas low cost burial insurance focuses on the $5,000 to $25,000 range. This targeted approach prevents you from paying premiums for unnecessary coverage. According to the NFDA 2023 report, the median funeral cost is $8,300, making these smaller policies a precise financial instrument.

Can I get low-cost burial insurance if I have a pre-existing medical condition?

You can secure coverage despite chronic health issues through our specialized underwriting methodology. Most providers offer simplified issue or guaranteed acceptance plans that bypass the rigorous scrutiny of standard medical exams. Statistics indicate that 95% of applicants over age 50 find a viable plan regardless of their health history. We focus on strategic alignment between your specific profile and the carrier’s risk appetite to ensure approval.

What happens if I move from Texas to another state like Florida?

Your policy remains fully portable and valid across all 50 states. The Paul Group ensures that your strategic planning isn’t tethered to a single geographic location. Whether you reside in Texas or Florida, the contractual obligations of the insurance carrier remain unchanged. This flexibility is a standard component in 100% of our curated life insurance portfolios, providing stability during life transitions.

How quickly does the payout occur after a death certificate is issued?

Beneficiaries typically receive the cash payout within 24 to 48 hours after the carrier receives the validated death certificate. This rapid liquidity is vital for managing immediate 2026 funeral costs and preventing family debt. While some complex claims might take up to 30 days, our Group prioritizes carriers with optimized claims processing systems. Speed is a core metric we use to evaluate the excellence of a provider.

Do I need a medical exam to qualify for a policy with The Paul Group?

You don’t need to undergo any physical examinations, blood tests, or physician visits to qualify. We utilize a non-invasive methodology that relies on a brief health questionnaire and a review of prescription history databases. This streamlined process reduces the approval window from 45 days to under 24 hours. It’s a strategic optimization designed for seniors who value both their time and their medical privacy.

What is the difference between a burial policy and a pre-paid funeral plan?

A burial policy delivers a tax-free cash benefit to your family, while a pre-paid plan locks you into specific services at a single funeral home. Cash offers holistic flexibility. If a funeral home goes out of business, pre-paid plans can become complex legal liabilities. Choosing low cost burial insurance ensures your beneficiaries can select any provider or use excess funds for outstanding medical bills or legal fees.

Can my premiums ever increase once my policy is active?

Your premiums are locked at the rate established during your initial enrollment and will never increase. We only recommend whole life structures where the cost remains fixed for the entire duration of the policy. This provides long-term fiscal stability for your 2026 budget. Even if your health declines significantly after the effective date, your monthly obligation won’t change by even 1%.

How do I know if I need $10,000 or $25,000 in coverage?

Your coverage requirement depends on the delta between your current liquid assets and anticipated 2026 end-of-life costs. A $10,000 policy typically covers a standard cremation and a basic memorial service. If you desire a traditional burial with a viewing, premium casket, and headstone, the $25,000 threshold is more appropriate. Our Wise Advisor approach helps you calculate these variables to ensure your legacy is structurally sound.

Leave a Reply