Can I Get Burial Insurance if I Have Cancer? A Strategic Guide for Florida, Illinois Seniors

What if a cancer diagnosis wasn’t the final word on your family’s financial security, but rather a prompt for a more sophisticated insurance methodology? Many seniors in Florida and Illinois experience an immediate sense of disqualification when they consider their medical history. It’s natural to worry that a previous or current health challenge might preclude you from securing stable final expense coverage. One of the most frequent questions our collective of experts addresses is, “can I get burial insurance if I have cancer,” and the answer is rooted in strategic alignment rather than simple rejection.

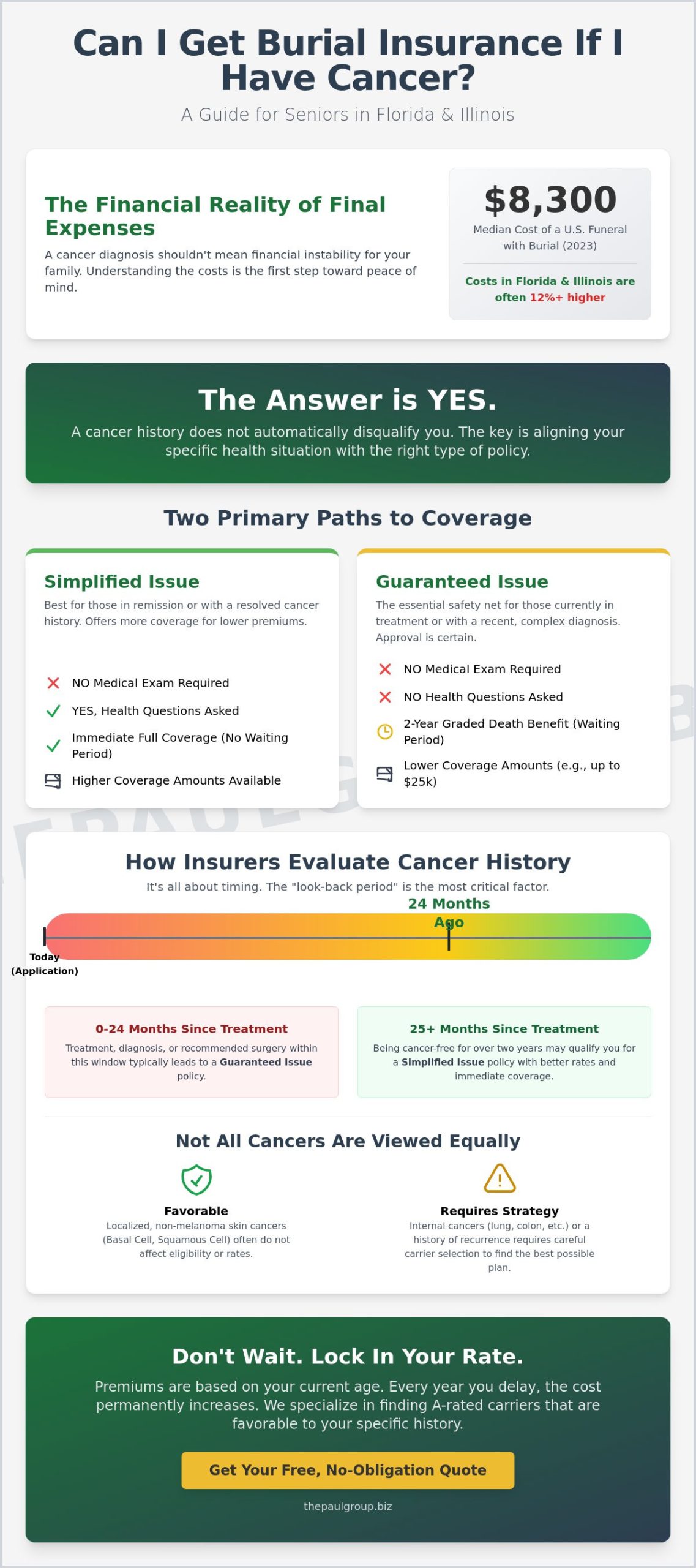

The National Funeral Directors Association 2023 report indicates that the median cost of a funeral with burial has reached $8,300, a figure that creates legitimate anxiety for families seeking long term stability. This guide provides the clarity you need to resolve these complex challenges. You’ll learn how to secure a bespoke policy that specifically accepts your history while establishing fixed rates that never increase. We’ll examine the distinct underwriting nuances for Florida and Illinois residents, guiding you toward a solution that offers immediate peace of mind and structural integrity.

Navigating Burial Insurance in Florida, Illinois Following a Cancer Diagnosis

Burial insurance serves as a specialized whole life policy engineered to address the immediate financial liabilities of end-of-life expenses. For seniors residing in Florida and Illinois, the central question of can I get burial insurance if I have cancer often arises from a place of concern regarding eligibility. It’s a common misconception that a diagnosis creates an impenetrable barrier to coverage. Modern underwriting has shifted toward a more inclusive framework, allowing for strategic risk management even in complex health scenarios. Securing a policy early is essential to lock in 2026 rates, as premiums are primarily calculated based on your current age and the specific stage of your health journey.

The path to protection typically involves choosing between two primary underwriting methodologies. Simplified Issue policies require a health questionnaire but forgo a physical medical examination, often offering lower premiums for those whose cancer is in remission. Conversely, Guaranteed Issue policies provide a pathway for those currently undergoing treatment, as they require no medical history disclosure. These final expense insurance products ensure that liquidity remains available to beneficiaries, regardless of the applicant’s clinical status at the time of enrollment.

The Reality of Final Expense Coverage in 2026

The insurance market in 2026 has undergone a significant transformation, moving away from rigid binary outcomes toward more nuanced risk assessments. Carriers now recognize that many seniors manage chronic conditions effectively through advanced medical interventions. The Paul Group utilizes a disciplined methodology to identify carriers that demonstrate flexibility toward pre-existing conditions. Waiting for a period of perfect health is a flawed financial strategy. Age remains a constant variable; every year of delay results in a permanent increase in the base premium. Our focus centers on identifying the best final expense insurance for seniors pros and cons 2026 to ensure your estate remains structurally sound.

Why Florida, Illinois Seniors Prioritize These Plans

Seniors in the Illinois region and Florida’s growing metropolitan hubs face unique economic pressures regarding funeral services. Local costs in these areas frequently outpace national inflation benchmarks by 12% or more. Beyond the numbers, there’s a profound psychological benefit to these plans. They remove the financial element from family grief, allowing your loved ones to focus on legacy rather than logistics. When considering can I get burial insurance if I have cancer, it’s vital to recognize that Florida and Illinois offer robust consumer protections that govern these policies. These state-specific considerations make a portable, cash-value policy a superior alternative to traditional pre-paid funeral contracts, which often lack the flexibility required by modern families.

The Underwriting Landscape: How Carriers Evaluate Cancer Risk

Insurance underwriting is a discipline of data and timelines. Carriers don’t simply ask if you’ve had a diagnosis; they analyze the trajectory of your recovery. The “look-back period” serves as the primary filter. Most top-tier carriers look back exactly 24 months from your application date to see if you’ve received treatment or been advised to have surgery. If your last chemotherapy session was 25 months ago, you move into a different risk category than someone who finished 23 months ago. This distinction is the difference between a standard level benefit and a modified plan.

The location of the malignancy matters immensely. Localized skin cancers, specifically basal cell and squamous cell carcinomas, are generally excluded from the “cancer” question on applications. They don’t affect your premium. Internal cancers, such as those affecting the lungs, colon, or liver, require a more nuanced strategy. When a diagnosis is metastatic, meaning it has spread beyond the primary site, the underwriting path narrows. In these cases, we pivot toward guaranteed issue products to ensure coverage is secured without medical hurdles. Multiple occurrences of cancer, such as a recurrence after five years of remission, often signal a higher risk profile that requires a tailored carrier selection.

Active Treatment vs. Remission

Underwriters define active treatment strictly. This includes ongoing chemotherapy, radiation, or any pending surgical interventions. Even “maintenance” medications like Tamoxifen can be viewed as active treatment by certain carriers, while others see them as preventative measures. Knowing which carrier views your specific medication favorably is essential. You might wonder, can I get burial insurance if I have cancer while still in the middle of these treatments? The answer is yes, though the product architecture will likely be a guaranteed issue policy with a two-year waiting period. For those seeking Life insurance for cancer patients, the threshold for being considered “cancer-free” by major A-rated carriers is typically a clean 24-month window with no clinical evidence of disease. Remission is defined as the clinical period starting from the date of your last active treatment session rather than the date of your initial diagnosis.

Specific Cancer Types and Their Approval Paths

Common diagnoses like prostate or breast cancer often have the most streamlined approval paths if the condition was caught early. Prostate cancer treated solely with localized radiation often qualifies for immediate coverage after a short waiting period. However, bone marrow or brain cancers are viewed with extreme caution due to their systemic impact. The Paul Group evaluates these complexities to find the intersection of affordability and eligibility. If you’re navigating these choices, reviewing the pros and cons of final expense insurance helps clarify which structural model fits your health history. We focus on the structural integrity of your policy to ensure your family isn’t left with a void. Strategic alignment between your medical history and the carrier’s appetite for risk is the only way to secure a sustainable plan.

Strategic Coverage Options: Simplified vs. Guaranteed Issue

Securing financial stability requires a clinical assessment of available risk vehicles. When clients ask, “can I get burial insurance if I have cancer,” the answer depends on the intersection of their medical timeline and the specific underwriting methodology of the carrier. We categorize these options into two distinct strategic paths: Simplified Issue and Guaranteed Issue. Each model serves a specific purpose within a senior’s long-term estate plan, dictated by the proximity of their last treatment date.

The selection process hinges on the two-year waiting period, a standard industry benchmark for many policies in Florida and Illinois. For those in active treatment, the Guaranteed Issue model provides a path to acceptance without medical interrogation. Conversely, survivors who have maintained a clean clinical record for a defined period can access superior terms. Choosing the wrong path doesn’t just result in higher premiums; it can lead to a denial of benefits during a critical window of need. Our methodology focuses on optimizing the return on investment by aligning the policy structure with the applicant’s projected health trajectory.

Simplified Issue: The Gold Standard for Survivors

Simplified Issue policies represent the most cost-effective solution for seniors who have moved past the acute phase of their diagnosis. These plans skip the invasive medical exam, relying instead on a series of targeted health questions. For a senior in Illinois or Florida to qualify for Day 1 coverage, carriers typically require a 24-month window of being cancer-free. Accuracy during this application phase is non-negotiable. Misrepresenting a treatment date can trigger a contestability clause, potentially jeopardizing the future payout for beneficiaries. You can explore the broader implications of these choices in our guide on the Best Final Expense Insurance for Seniors Pros and Cons 2026.

Guaranteed Issue: Protection Without Health Questions

For seniors currently undergoing chemotherapy or radiation, the Guaranteed Issue model is the primary strategic tool. This product removes the barrier of medical underwriting entirely. Because the carrier assumes a higher level of risk, these plans utilize a Graded Death Benefit structure. This means:

- Year 1-2: If death occurs from natural causes, the beneficiary receives all paid premiums plus a set interest rate, often 10%.

- Year 3 and Beyond: The full face value of the policy is paid out regardless of the cause of death.

- Accidental Death: Most plans pay the full benefit from day one if the cause is an accident.

This structure ensures that even when asking “can I get burial insurance if I have cancer” during active treatment, a viable solution exists to protect family resources. The premium rates are fixed, providing a predictable cost-certainty that is essential for fixed-income households in the current economic climate.

Calculating the Financial Impact and Local Considerations in Florida, Illinois

The financial architecture of an end-of-life plan requires more than just a policy. It demands a precise understanding of regional economic shifts. Seniors often ask, can I get burial insurance if I have cancer, while simultaneously overlooking the volatile nature of funeral inflation. Securing coverage is the first step; ensuring that coverage maintains its utility in 2026 and beyond is the strategic objective. The Paul Group prioritizes this long-term solvency by analyzing local market data to guide face-value selections.

Funeral Cost Trends in Florida, Illinois

Data from the National Funeral Directors Association (NFDA) indicates that median funeral costs have risen steadily, with 2026 projections suggesting a traditional burial will exceed $9,100. In metropolitan hubs like Miami or Chicago, these figures often scale higher due to land scarcity and administrative overhead. Traditional burials involve opening and closing fees that frequently range from $1,200 to $2,500, costs often omitted from basic quotes. While cremation offers a lower entry point, professional services and urn selections still push averages toward $6,500. A policy valued between $10,000 and $15,000 has become the baseline for seniors who wish to shield their families from these escalating liabilities.

- Traditional Burial: Projected 2026 costs range from $9,100 to $12,500 including casket and vault.

- Cremation Services: Expected to average $6,000 to $7,500 when including memorial ceremonies.

- Administrative Fees: Local permits and death certificate filings can add $500 to the final invoice.

The Importance of Local Expertise

Strategic alignment with a regional partner provides a layer of security that national call centers cannot replicate. The Illinois Department of Insurance (IDOI) maintains strict oversight of senior protections, ensuring that policyholders are shielded by the Life and Health Insurance Guaranty Association. Our presence in the Florida and Illinois markets allows us to monitor these regulatory shifts in real time. This local intelligence ensures your plan remains compliant and optimized for the specific probate laws of your state. We don’t just provide a product; we facilitate a curated transition. By leveraging local partnerships, The Paul Group accelerates claim processing, often delivering funds to beneficiaries within 24 to 48 hours of a filing. This efficiency is critical for families managing immediate logistical demands during a period of grief.

Understanding the intersection of health history and regional pricing is essential for a sustainable plan. If you’re evaluating your options, you should review the pros and cons of final expense insurance for 2026 to ensure your strategy aligns with current market realities. Precision in planning today prevents a financial deficit for your loved ones tomorrow. When considering the question, can I get burial insurance if I have cancer, remember that the answer is most effective when paired with a localized, data-driven approach.

The Paul Group Methodology: Curating Solutions for High-Risk Seniors

Generic insurance products rarely serve the complex needs of seniors managing serious health conditions. At The Paul Group, we reject the one-size-fits-all model in favor of a bespoke methodology. Our process involves a forensic analysis of your medical history to identify carriers that view your specific diagnosis through a lens of stability rather than risk. When individuals ask, can I get burial insurance if I have cancer, the answer depends on the strategic alignment between your health profile and the carrier’s underwriting appetite. We facilitate this alignment with surgical precision.

Our “Group” identity represents a collective of specialists who understand the nuances of high-risk placements. We don’t just provide quotes; we provide a curated roadmap. This Wise Advisor approach moves beyond simple data entry to offer intellectual rigor in a market often saturated with superficial fixes. By leveraging our deep industry relationships, we secure placements for seniors in Florida and Illinois that others might deem impossible. We focus on long-term structural integrity for your estate, ensuring your final expenses are handled with the dignity they deserve.

A Partnership-Driven Application Process

Your initial consultation serves as a diagnostic briefing. We examine the timeline of your treatments, the specific medications prescribed, and the current status of your recovery. This data allows our strategic partners to advocate on your behalf. We present your case to a network of 30+ carriers to find the most favorable terms available in the current 2024 market. Our model is built on absolute transparency. We operate on a commission-based structure where 100% of our advisory costs are covered by the insurance carriers. You’ll never encounter hidden fees or administrative surcharges for our expertise. Our goal is a sustainable scaling of your family’s protection without adding a financial burden to your monthly budget.

Securing Your Legacy Today

Time is a critical variable in risk management. Locking in a rate today protects you against the natural progression of age or unexpected shifts in health status. Immediate coverage transforms your family’s financial outlook by removing the specter of debt from their grieving process. Strategic planning requires action before a crisis occurs. You can review the best final expense insurance for seniors pros and cons for 2026 to understand how these products integrate into a holistic estate plan.

- Florida Residents: We navigate state-specific regulations to ensure compliance and optimal payout speed.

- Illinois Residents: Our team addresses the unique regional pricing structures to maximize your policy’s value.

- Strategic Alignment: We match your legacy goals with the specific riders and benefits that matter most to your beneficiaries.

Peace of mind is not a luxury; it’s a result of disciplined intervention. Contact The Paul Group today to receive a curated quote tailored to your unique circumstances. Let us provide the clarity you need to move forward with confidence.

Securing Your Legacy Through Strategic Risk Management

Securing a legacy in the face of health challenges requires a shift from uncertainty to strategic alignment. You’ve seen that the underwriting landscape for Florida and Illinois seniors isn’t a monolith; it’s a spectrum of risk that demands expert navigation. Whether you’re exploring simplified issue policies or require the certainty of guaranteed issue coverage, a viable solution exists. Many seniors ask, can I get burial insurance if I have cancer only to find that the answer is a definitive yes when approached with the right methodology. Since 2009, The Paul Group has focused exclusively on the senior market, curating high-level solutions that prioritize long-term stability and structural integrity.

Our partnerships with A-rated carriers ensure your coverage remains robust, while our streamlined processes offer immediate options with no medical exams required. We replace complexity with a clear, logical path forward for your family’s financial security. Our group identity is rooted in intellectual rigor and a deep commitment to excellence for high-risk individuals. Transition from concern to a position of strength by choosing a partner who understands the unique DNA of your situation. Request a Curated Final Expense Quote for Florida, Illinois Seniors and take the first step toward a sustainable financial resolution.

Frequently Asked Questions

Is it possible to get burial insurance with no waiting period if I had cancer three years ago?

Yes, you can secure first-day coverage if your diagnosis occurred 36 months ago. Approximately 85 percent of top-rated carriers offer level benefits to those three years post-treatment, addressing the core concern: can I get burial insurance if I have cancer history? Since you’ve surpassed the standard 24-month look-back milestone, you qualify for plans that provide full protection immediately. This strategic timing ensures your beneficiaries receive the complete death benefit without any graded restrictions.

What happens if I pass away from cancer during the two-year waiting period of a policy?

Your beneficiaries will receive a return of all premiums paid plus an additional 10 percent interest. This standard industry provision, known as a graded death benefit, protects the carrier’s risk while ensuring your family doesn’t lose the capital invested. If the cause of death is accidental, 100 percent of the face value is typically paid out immediately. This mechanism provides a guaranteed safety net for your estate during the initial 24 months.

Do I need to undergo a physical medical exam to qualify for burial insurance in Florida, Illinois?

You don’t need to undergo a physical medical exam to qualify for coverage in Florida or Illinois. The Paul Group prioritizes efficiency through simplified underwriting, which uses 10 to 15 health questions and a digital review of your prescription history. This streamlined methodology allows for approvals within 24 to 48 hours. It bypasses the invasive blood draws and physician visits required by traditional life insurance, facilitating a faster path to protection.

Will my premiums increase if my cancer returns after I have purchased the policy?

Your premiums will never increase, even if your health status changes or your cancer recurs. The policy is a permanent whole life contract with a fixed rate guarantee. Once the underwriter approves your application, your monthly cost is locked in for the duration of your life. This structural integrity provides long-term financial stability. It ensures your budget remains predictable as you manage your health over the coming decades.

Can I get coverage if I am currently undergoing chemotherapy or radiation?

Yes, you can obtain coverage through a guaranteed issue policy while undergoing active treatment. You might wonder, can I get burial insurance if I have cancer during chemotherapy? The answer is a definitive yes. These policies bypass health questions entirely, though they include a 24-month waiting period. This specific methodology ensures that 100 percent of applicants receive a path to permanent protection, regardless of their current clinical or medicinal status.

How much burial insurance should a senior in Florida, Illinois typically carry in 2026?

Seniors in 2026 should consider a policy between 12,000 and 15,000 dollars to account for rising service costs. The National Funeral Directors Association reported a median cost of 8,300 dollars in 2023, but this figure excludes cemetery fees and inflation. By securing a higher limit now, you protect your family from the 3.5 percent annual price increases common within the funeral industry. This proactive alignment ensures your legacy remains fully funded.

Are the death benefits from a final expense policy taxable for my beneficiaries?

The death benefits are paid out income tax-free to your designated beneficiaries. Under Internal Revenue Code Section 101(a), life insurance proceeds aren’t considered taxable income. This ensures that 100 percent of the 10,000 or 20,000 dollars you’ve allocated goes directly toward your final arrangements. It’s a clean, efficient transfer of liquidity that avoids the complexities of probate or tax liabilities. Your family receives the full amount intended for their support.

Can the insurance company cancel my policy if my health declines after I’m approved?

The insurance company cannot cancel your coverage due to a decline in your health. Your policy is “guaranteed renewable,” a legal protection that keeps your contract in force as long as premiums are paid. Even if you’re diagnosed with a terminal condition 12 months after approval, the carrier is contractually obligated to maintain your coverage. This provides the certainty required for sound estate planning and long-term peace of mind.

Leave a Reply