Final Expense Insurance for Diabetics in Florida, Illinois: A 2026 Strategic Guide

A diabetes diagnosis is not a disqualifier for elite financial protection. While many carriers treat insulin use as an automatic barrier to their best rates, the 2026 insurance market has evolved to favor those who prioritize strategic stability. You’ve likely experienced the frustration of being told that your health history makes you a high-risk liability. It’s exhausting to search for final expense insurance for diabetics only to be met with multi-year waiting periods or premiums that eat away at your fixed income.

We believe your legacy deserves a foundation built on certainty, not a policy that fluctuates with the market or your blood sugar levels. This strategic guide details how seniors in Florida, Illinois can secure immediate, fixed-rate coverage that never increases, regardless of future health shifts. By aligning your coverage with 2024 NFDA data regarding regional burial expenses, we’ll move you from a state of complexity to a position of absolute financial clarity. We’ll explore the specific underwriting nuances that allow for immediate protection and a tailored plan for managing Florida, IL funeral costs.

Navigating Final Expense Insurance for Diabetics in Florida, Illinois

Final expense insurance serves as a foundational pillar for legacy protection within the Illinois senior community. It isn’t just a policy; it’s a strategic tool designed to insulate families from the immediate financial burdens of funeral costs and medical debt. For residents of Florida, IL, the 2026 insurance market presents a landscape of both complexity and opportunity. While inflationary pressures have increased the average cost of end-of-life services, expanded competition among carriers has created a more nuanced environment for those managing chronic conditions. Securing final expense insurance for diabetics in this climate requires a move away from generic products toward bespoke financial instruments.

The Paul Group views these market conditions through the lens of a Wise Advisor. We believe that obstacles are merely variables to be optimized through disciplined intervention. Standard life insurance often relies on broad health assessments that can penalize individuals for manageable conditions. In contrast, the specialized final expense plans we curate focus on the stability of your current health regimen. This distinction is vital for those seeking the best final expense insurance for seniors, as it shifts the focus from risk avoidance to strategic alignment. We don’t just find a policy; we engineer a solution that respects your health history and your financial goals.

The Local Landscape of Senior Coverage in Illinois

Burial plans within the Florida, IL region are governed by robust state-level regulations that offer significant protections for policyholders. The Illinois Department of Insurance maintains strict oversight, ensuring that carriers adhere to transparent marketing practices and maintain solvency. This regulatory framework, combined with the Illinois Life and Health Insurance Guaranty Association, provides a safety net that many seniors overlook. Working with a brokerage that understands these local nuances is essential for long-term stability. We analyze the specific providers operating within the state to ensure your plan complies with Illinois statutes while providing maximum benefit. This local expertise prevents the administrative friction often found with national, non-specialized firms that don’t understand the specific provider networks in our region.

Why Diabetes is a Strategic Consideration, Not a Barrier

Modern 2026 underwriting methodologies have evolved significantly. The industry has moved away from binary assessments. Instead, Understanding Underwriting allows us to demonstrate how consistent management and medical adherence lead to favorable premiums. Final expense insurance is a permanent whole life solution specifically engineered to cover end-of-life costs and provide immediate liquidity to beneficiaries.

The conversation for Florida residents has shifted from “if you qualify” to “how you qualify” based on specific health data like A1C levels and medication history. We utilize a holistic approach to position your medical history in the most favorable light for 2026 carriers. Choosing final expense insurance for diabetics shouldn’t feel like a compromise. It’s an opportunity for cultural and structural evolution in how you approach your estate. We look for carriers that reward those who actively manage their health, turning a medical diagnosis into a manageable underwriting factor. Our methodology ensures that your coverage is as resilient as the legacy you’re building.

Understanding Underwriting: How Your Diabetes Profile Impacts Policy Options

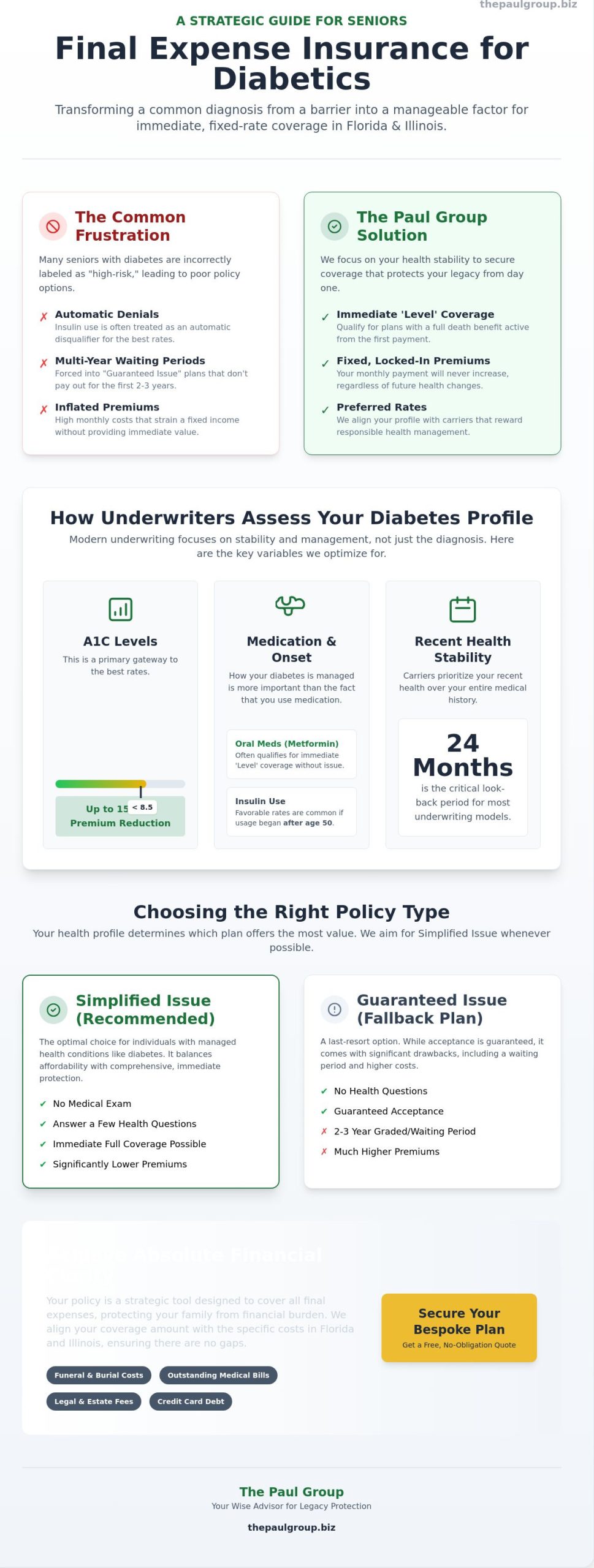

Underwriting serves as the architectural blueprint of any insurance contract. When securing final expense insurance for diabetics, the process hinges on the precision of your health data. Carriers don’t merely look for a diagnosis; they analyze the trajectory of your condition. Actuaries prioritize specific markers, most notably your A1C levels and the age of your initial diagnosis. An A1C reading below 8.5 often acts as a gateway to “Preferred” rates, which can reduce monthly premiums by 15% to 20% compared to standard offers.

The Paul Group approaches this complexity through a lens of strategic curation. We identify carriers that overlook specific diabetic markers if other health indicators, such as blood pressure and kidney function, remain stable. This methodology ensures that a single lab result doesn’t dictate your financial future. We focus on the following underwriting variables:

- Medication Type: Metformin and other oral medications are viewed as indicators of controlled Type 2 diabetes, often qualifying for immediate “Level” coverage.

- Insulin Dependency: While insulin use is a significant factor, many carriers now offer competitive rates if the usage began after age 50.

- Recent Stability: Most 2026 underwriting models prioritize your health over the last 24 months rather than your entire medical history.

Securing the right plan requires aligning your specific medical profile with a carrier’s unique risk appetite. For a broader perspective on how these choices impact your long-term legacy, you may find value in our analysis of the pros and cons of senior policies.

Type 1 vs. Type 2: The Underwriter’s Perspective

Type 2 diabetes is frequently categorized as a manageable lifestyle condition, allowing many applicants to secure first-day coverage without a waiting period. Type 1 diabetics face a different strategic path. Because Type 1 is often diagnosed in childhood, underwriters view it through the lens of long-term systemic impact. To avoid high-risk pool pricing, we pivot Type 1 clients toward carriers that emphasize current A1C stability over the duration of the illness. This shift in perspective is essential for maintaining premium stability as you age.

Critical Complications: Insulin Use and Neuropathy

Complications such as neuropathy or a history of insulin shock require a nuanced application strategy. If you’ve experienced a diabetic coma within the last 3 years, many standard carriers will move the policy into a “Graded” benefit structure. This means the full death benefit might not be available for the first 24 months. Transparency during the disclosure process is vital. Adhering to state regulations regarding consumer disclosures ensures that your policy remains an ironclad contract that your beneficiaries can rely upon. If your health history is complex, our strategic advisors can help you navigate these disclosures to find the most favorable terms available in the current market.

Can I Be Denied? Evaluating Guaranteed Issue vs. Simplified Issue Plans

The short answer is yes. You can be denied life insurance, but the reasons for denial differ sharply between policy types. Guaranteed issue plans are marketed with the promise that you won’t be turned away due to your health history. This is true. However, carriers still reject applications based on age requirements, residency status, or if you’ve already reached the maximum coverage limit allowed by that specific insurer. For many, these plans represent a safety net, yet they shouldn’t be your first choice.

Simplified issue plans offer a more sophisticated alternative. These policies require you to answer a series of health questions but skip the invasive physical exam. Securing final expense insurance for diabetics through a simplified issue route often results in lower premiums and immediate coverage. The Paul Group views this as a strategic priority. If your diabetes is well-managed, settling for a guaranteed issue plan means paying a premium for a risk you don’t actually pose to the insurer. Seniors should weigh the pros and cons of final expense insurance for seniors before committing to a plan that might offer less value than a customized solution.

The Truth About Denial in Guaranteed Issue Life Insurance

Guaranteed issue is a last resort. It’s designed for individuals whose medical complications are so severe that traditional underwriting is impossible. While you cannot be denied for having Type 1 or Type 2 diabetes, these policies carry a significant structural risk: the waiting period. Most national brands implement a 24-month graded death benefit. If the policyholder passes away from natural causes during this two-year window, the beneficiary only receives the premiums paid plus a small percentage of interest. In Florida and Illinois, where the cost of final arrangements is projected to rise by 4.2% by 2026, this delay creates a dangerous gap in your financial legacy. We recommend seeking simplified issue first to gain immediate protection from day one.

Strategic Alignment: When to Choose No-Exam Coverage

Simplified issue coverage aligns perfectly with the needs of diabetics who maintain a disciplined health regimen. These plans provide higher death benefits for lower monthly costs because the insurer can verify your health status through digital records. Instead of a physical exam, simplified issue plans utilize a medical database check to review your prescription history and previous insurance applications. This methodology allows for a rapid approval process, often within 24 to 48 hours.

Choosing this path requires a proactive approach. In Illinois, seniors often find that simplified issue plans offer 15% to 25% more coverage for the same dollar spent on a guaranteed issue policy. It’s about optimization. You’re leveraging your health management to secure better terms. We focus on matching your specific A1c levels and medication history with the right carrier’s underwriting appetite. This ensures your final expense insurance for diabetics is not just a policy, but a precisely engineered financial tool.

Calculating Funeral and Final Costs in Florida, Illinois

Securing final expense insurance for diabetics requires a cold-eyed assessment of the current economic climate in the Florida, Illinois region. By 2026, the cost of a standard funeral service in central Illinois has reached a median of $9,450, a figure that excludes the escalating prices of cemetery plots and headstones. These service fees have seen a 14% increase since 2022, driven by labor shortages and rising material costs for caskets and vaults. For families in the Kankakee River valley area, these numbers aren’t just statistics. They represent a significant financial hurdle that requires a disciplined, strategic response.

The Paul Group advocates for a “Safe Harbor” coverage methodology. This calculation ensures that your policy doesn’t just cover the casket, but also clears the “hidden” debts that often blindside grieving families. In Illinois, probate costs can consume 3% to 7% of an estate’s total value. When you factor in the final medical bills often associated with chronic condition management, a policy that only covers the funeral director’s bill is insufficient. We recommend a coverage amount that includes a 20% buffer above projected service costs to account for these administrative and medical liquidations.

Local Burial and Cremation Cost Trends in 2026

Strategic planning in Florida, IL reveals a widening gap between traditional burial and cremation options. While a traditional burial in the Illinois region now averages $10,200, cremation services have stabilized around $4,100 for basic packages. However, “premium cremation” with a memorial service is seeing increased demand, often reaching $6,500. Choosing between these paths isn’t merely a matter of preference; it’s a financial decision that dictates your necessary policy face value. Many seniors find that pre-paying for these services directly with a funeral home lacks the flexibility of an insurance policy. Life insurance stays with you even if you move away from the Kankakee area, whereas pre-paid plans are often tied to a single provider’s solvency.

Optimizing Your Coverage Amount for Inflation

Inflation is the silent eroder of financial security. A $10,000 policy purchased today might feel robust, but if it’s utilized in 2036, its purchasing power will likely be reduced by nearly 30% based on current trajectory models. This is why final expense insurance for diabetics should ideally be structured as a fixed-rate whole life policy. These instruments offer a locked-in premium that won’t increase as you age or as your health evolves. The Paul Group helps clients tailor their policy face value by analyzing local Illinois inflation trends, ensuring the benefit delivered to your beneficiaries is as impactful a decade from now as it’s today.

Our Group identity is built on the belief that your legacy shouldn’t be a source of stress for your heirs. We move beyond off-the-shelf solutions to provide a holistic view of your final obligations. By aligning your coverage with the actual costs of the Illinois funeral market, we transform a complex liability into a structured, manageable asset.

To better understand how to structure your protection, explore our detailed analysis of the pros and cons of senior coverage in the current market.

The Paul Group Methodology: Bespoke Final Expense Solutions for Seniors

Effective financial planning for seniors with chronic health conditions requires more than a simple transaction. It demands a disciplined, partner-driven approach that prioritizes long-term stability over quick fixes. The Paul Group serves as a Wise Advisor, guiding families through the complexities of the insurance market with an air of quiet confidence. We don’t believe in generic policies. Instead, we employ a methodology rooted in intellectual rigor to find the precise alignment between your health profile and the right carrier.

Why a Specialized Florida, IL Brokerage Matters

Since our founding in 2009, The Paul Group has remained committed to serving Illinois families through a high-level advisory model. Unlike national call centers that rely on high-volume, transactional interactions, our local presence in Florida, IL, allows for a deeper understanding of the regional landscape. We’ve spent 15 years refining our screening process to identify carriers that are genuinely diabetic-friendly. This specialized focus is critical when seeking final expense insurance for diabetics, as underwriting standards vary significantly across the industry.

- We conduct a holistic audit of your medical history to match you with carriers that accept insulin use or neuropathy.

- Our brokerage access includes multiple A-rated providers, ensuring we aren’t limited to a single company’s rigid rules.

- We prioritize fixed rates, ensuring your premiums never increase regardless of future health changes or market shifts.

Securing Your Legacy with Immediate Coverage

The emotional weight of an unprotected legacy is a burden no family should carry. Our strategic objective is to move you from a state of uncertainty to one of absolute clarity. We focus on securing immediate coverage options that activate on day one, avoiding the two-year waiting periods often found in mass-market plans. You can learn more about the nuances of these choices by reviewing our guide on best final expense insurance for seniors pros and cons 2026. This curated approach ensures your final expenses are managed with the same level of care you’ve applied to every other aspect of your life.

Starting the process is straightforward. We offer a sophisticated, no-obligation consultation designed to diagnose your needs before prescribing a solution. It’s a boardroom-level conversation focused on your individual legacy. Our Group identity represents a collective of experts dedicated to structural integrity and the optimization of your family’s financial security. Securing final expense insurance for diabetics through our methodology provides the peace of mind that comes from a perfectly engineered plan. Reach out today to experience a partnership that values your long-term stability.

Securing Your Legacy Through Strategic Alignment

Navigating the complexities of the 2026 insurance landscape requires a disciplined approach to risk management. Successfully securing final expense insurance for diabetics involves more than simply selecting a policy; it demands a deep understanding of how specific health profiles influence underwriting outcomes in Florida and Illinois. Our methodology prioritizes structural integrity, ensuring that the plan you choose today remains a stable pillar for your family tomorrow. Since 2009, The Paul Group has specialized in high-risk diabetic underwriting, moving beyond superficial fixes to provide curated solutions for seniors. We eliminate the uncertainty of medical exams while providing fixed-rate guarantees that protect against future market volatility.

This strategic alignment between your health history and policy structure is essential for long-term optimization of your estate. Your legacy isn’t a transaction; it’s a commitment to excellence that deserves professional oversight. Consult with The Paul Group to secure your bespoke final expense plan today. You’ve worked hard to build your life, and we’re here to ensure your final arrangements reflect that same level of care and precision.

Frequently Asked Questions

Can I be denied guaranteed issue life insurance if I have severe diabetes?

You cannot be denied guaranteed issue coverage regardless of the severity of your diabetes. This specific policy type eliminates medical inquiries entirely, ensuring that 100 percent of applicants between the ages of 50 and 85 qualify for protection. The Paul Group views this as a critical safety net for those with complex health histories. While these plans include a standard two year graded death benefit period, they offer a definitive path to securing legacy stability when other avenues remain closed.

Is there a waiting period for final expense insurance if I use insulin?

A waiting period isn’t a universal requirement for insulin users. While many carriers impose a 24 month graded period for those who began insulin treatment before age 40, several top tier providers now offer first day coverage for Type 2 diabetics who maintain controlled glucose levels. The Paul Group utilizes a rigorous selection methodology to identify carriers that reward disciplined health management. This strategic alignment ensures that your final expense insurance for diabetics provides immediate peace of mind rather than delayed utility.

How much does burial insurance cost for a diabetic in Florida, Illinois?

Premiums for diabetic applicants are determined by individual risk profiles and regional actuarial data. According to the 2024 LIMRA Insurance Barometer Study, average monthly costs for a 10,000 dollar policy can range from 40 to 90 dollars depending on the severity of the condition. Florida and Illinois residents benefit from a competitive marketplace where 15 major carriers vie for market share. Our group analyzes these market fluctuations to secure bespoke pricing that reflects your specific health trajectory and financial objectives.

What happens if I don’t disclose my diabetes on a life insurance application?

Non-disclosure of diabetes triggers a two year contestability period that allows carriers to void the policy or deny claims. If an insurer discovers omitted medical history through the Medical Information Bureau or prescription database checks, they’ll likely rescind the contract for material misrepresentation. The Paul Group advocates for radical transparency during the application process. This integrity ensures your beneficiaries receive the full death benefit without the risk of legal entanglements or financial forfeiture.

Can I get life insurance if I have diabetic complications like neuropathy or retinopathy?

You can secure coverage even with advanced complications like neuropathy or retinopathy. These conditions typically move an applicant from “standard” to “graded” or “guaranteed” risk categories. Statistics from the American Diabetes Association indicate that over 37 million Americans manage these complexities, prompting insurers to develop specialized products. We curate these options to ensure that physical challenges don’t translate into a lack of financial security for your family.

Does Type 2 diabetes always result in higher insurance premiums?

Type 2 diabetes doesn’t automatically dictate premium increases. Applicants who maintain an A1C level below 7.0 percent and utilize oral medications often qualify for standard rates identical to non-diabetics. The Paul Group focuses on the optimization of your application by highlighting your commitment to health maintenance. By demonstrating consistent medical compliance, you can access final expense insurance for diabetics that remains both affordable and comprehensive.

What is the difference between burial insurance and final expense insurance?

Burial insurance and final expense insurance are functionally identical terms describing small whole life policies. Both products are engineered to cover end of life costs, including funeral services and outstanding medical debts. The primary distinction lies in marketing nomenclature rather than structural design. Our strategic approach simplifies this landscape, focusing on the underlying policy guarantees and cash value accumulation rather than the labels used by various agencies.

Is a medical exam required for seniors in Illinois to get coverage?

A medical exam is rarely required for seniors seeking final expense coverage in Illinois. Most providers utilize a simplified issue methodology that relies on a brief health questionnaire and a review of prescription history. Data from 2023 industry reports show that 85 percent of final expense applications are processed without a physical exam. This streamlined intervention allows for rapid approval cycles, often providing active coverage within 24 to 48 hours of submission.

Leave a Reply