Can I Get Burial Insurance if I Have Cancer? A Strategic Guide for 2026

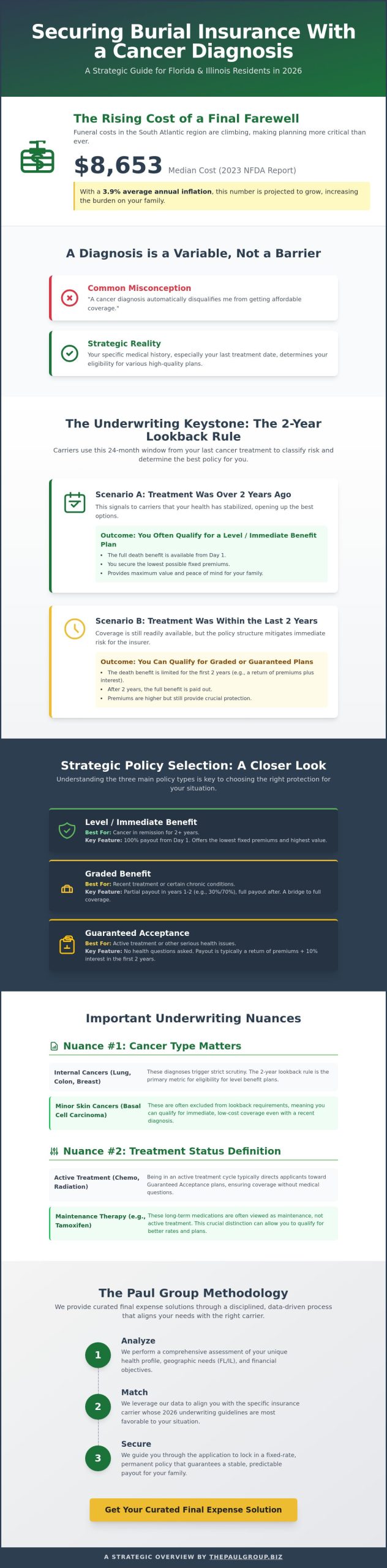

What if a medical diagnosis was merely a strategic variable rather than an absolute barrier to your legacy? Many seniors across Florida and Illinois assume that once they face a health challenge, their options for final expense protection vanish. You’ve likely spent hours wondering, can I get burial insurance if I have cancer, while watching funeral costs in the South Atlantic region climb toward a median of $8,653 according to the 2023 NFDA report. It’s a valid concern that demands a sophisticated, data-driven response rather than a generic application.

The Paul Group understands that your primary objective is a stable, fixed-rate solution that protects your family from regional market volatility. We’ll show you how to secure a guaranteed payout by identifying the specific insurance carriers that prioritize long-term stability over immediate exclusion. This guide details our methodology for distinguishing between graded and immediate benefits; this ensures you achieve a bespoke coverage plan tailored to your unique health profile and geographic requirements for 2026.

Understanding the Landscape of Burial Insurance with Cancer in 2026

The strategic environment for final expense planning has shifted significantly as we enter 2026. For many families, the central question is no longer just “can I get burial insurance if I have cancer,” but rather how to optimize a policy that accounts for modern medical advancements and rising economic pressures. Burial insurance remains a specialized, small-face-value form of whole Life insurance specifically engineered to settle end-of-life obligations. Unlike broader financial instruments, these policies focus on immediate liquidity for beneficiaries.

In 2026, insurance carriers have transitioned toward more nuanced risk assessments. Data-driven underwriting now allows providers to distinguish between different stages of recovery and types of malignancy. If you’re managing a diagnosis in states like Florida or Illinois, localized economic factors are critical. Funeral cost inflation in these regions has averaged 3.9% annually over the last three years, making the timing of your application a vital component of your long-term fiscal health.

The Paul Group views this process as a disciplined intervention. We distinguish between simply “being covered” and “qualifying for immediate benefits.” While many carriers offer protection to those with a history of illness, the structure of the payout—whether it’s a level benefit or a graded plan—depends entirely on the strategic alignment of your medical timeline with the carrier’s specific 2026 guidelines.

The Core Purpose of Final Expense Coverage

The primary objective is the seamless transition of financial liability from the family unit to the insurance carrier. Traditional term policies often fail those with high-risk health histories because they expire or require rigorous medical exams that many cancer survivors cannot pass. In contrast, final expense policies offer permanent protection. The fixed premium structure is a cornerstone of this strategy. It ensures that your monthly commitment remains static, protecting your household budget from the volatility of the 2026 insurance market. For a deeper look at how these structures benefit older adults, reviewing the best final expense insurance for seniors pros and cons 2026 provides essential context for your decision-making process.

Common Misconceptions About Cancer and Eligibility

Underwriting Nuances: How Carriers View Your Cancer History

Carrier underwriting isn’t a monolith. It’s a calculated assessment of risk duration and stability. When you ask, “can I get burial insurance if I have cancer,” you’re actually inquiring about how an actuary weights your specific diagnosis against their mortality tables. The Paul Group views this through a lens of strategic alignment; we match your medical history with the carrier most likely to offer favorable terms. Transparency isn’t just a moral choice. It’s the structural foundation of a policy that actually pays out when your family needs it most. Carriers prioritize the date of your last treatment over the date of your initial diagnosis.

The 2-Year Lookback Rule Explained

For most internal cancers, the 24-month mark represents a critical threshold in senior life insurance. Carriers use this window to distinguish between an active medical crisis and a stabilized health history. If your last treatment occurred more than two years ago, you often qualify for level-benefit coverage. This means your full death benefit is available from day one. The lookback period serves as the primary metric for premium optimization by defining the transition from high-risk classification to standard eligibility. While internal cancers like lung or colon cancer trigger strict scrutiny, minor skin cancers like basal cell carcinoma are often excluded from these lookback requirements entirely. This distinction allows for immediate, low-cost coverage even if the diagnosis was recent.

Navigating Coverage During Active Treatment

Active treatment protocols, including chemotherapy or radiation, typically redirect applicants toward guaranteed acceptance plans. These policies require no medical questions, making them a fail-safe for complex health profiles. Many of Forbes Advisor’s best burial insurance companies offer these products to ensure no one is left without a legacy plan. However, the distinction between active treatment and maintenance therapy is vital. Medications like Tamoxifen, used for years after breast cancer remission, are frequently viewed as maintenance rather than active treatment. This nuanced classification allows some carriers to offer better rates than they would for someone in an active chemo cycle. Understanding these pros and cons of final expense insurance helps you choose a path that balances immediate needs with long-term cost efficiency. If you’re managing a current diagnosis, a tailored consultation can clarify which carriers will accept your specific medication list and provide the structural integrity your estate requires.

Strategic Policy Selection: Graded vs. Guaranteed Acceptance

Selecting a policy requires more than a simple application; it demands a calculated alignment of risk and objective. When individuals ask, “can I get burial insurance if I have cancer,” they’re often seeking a solution that balances immediate protection with long-term financial stability. The structural integrity of a plan depends on its underwriting tier. For those with a history of malignancy, the choice often narrows to graded or guaranteed acceptance models. Understanding the pros and cons of final expense insurance allows families to move beyond surface-level comparisons toward a curated financial strategy.

The 24-month waiting period serves as the primary mechanism for risk mitigation within these structures. If death occurs during this initial window, beneficiaries typically receive a return of premiums plus interest, often calculated at 10% annually. This isn’t a failure of the policy. It’s a structured safety net. Strategic optimization occurs when the premium cost aligns with the probability of outliving this period. For a patient who completed treatment 24 months ago, the risk profile differs significantly from someone currently undergoing active chemotherapy. We look for the intersection where the death benefit provides maximum utility relative to the capital invested.

Level vs. Graded Benefit Structures

Level benefits represent the ideal outcome: full payout from day one. These are typically reserved for individuals who have been in remission for at least 24 to 36 months, depending on the specific carrier’s look-back period. Graded benefits offer a tiered payout system. A common structure might pay 30% of the face value in year one, 70% in year two, and 100% thereafter. This methodology provides a middle ground. It ensures that some level of capital is available to the family while accounting for the elevated medical risk the insurer assumes.

When Guaranteed Issue is the Right Move

Guaranteed issue policies bypass medical history entirely. There are no health questions and no physician statements required. This is the most compassionate choice for those facing metastatic or terminal diagnoses where traditional underwriting would result in an immediate decline. While premiums are higher, the structural security is absolute. It provides a guaranteed path to coverage for those who might otherwise be excluded from the market. For individuals currently managing active stages of illness, this approach ensures that “can I get burial insurance if I have cancer” is answered with a definitive and reliable “yes.”

Navigating the Application in Florida and Illinois

State-level regulations dictate the structural integrity of your policy. In Florida and Illinois, the insurance landscape requires a nuanced understanding of local statutes to ensure your legacy remains secure. For those asking, can I get burial insurance if I have cancer, the answer often depends on how a carrier interprets regional risk pools and state-mandated consumer protections. Successful navigation requires a methodology that balances medical transparency with strategic timing.

Florida and Illinois: A Tale of Two Markets

Illinois law provides a standardized two-year contestability period. This window allows carriers to investigate claims, but it also enforces a strict limit on how long a company can challenge the validity of a policy based on initial health disclosures. In Chicago, where the average funeral cost exceeded $8,200 in 2024, the need for immediate, reliable coverage is a mathematical necessity for most families. The Illinois Department of Insurance maintains a vigilant stance on policy language, ensuring that “simplified” products remain accessible to those with chronic conditions.

Florida’s regulatory environment is shaped by its massive senior population. With over 21 percent of the state’s residents aged 65 or older, the Florida Department of Financial Services maintains rigorous oversight to prevent predatory pricing. In Miami, where cemetery space is at a premium and costs are rising by 4.3 percent annually, a bespoke insurance strategy is the only way to mitigate future financial volatility. We analyze carrier appetites across these borders to find the strategic alignment your specific health profile requires. Local expertise isn’t a luxury; it’s a requirement for optimizing your premiums.

Preparing for the ‘Simplified’ Application

The term “simplified issue” doesn’t mean “unvetted.” While these policies bypass the traditional medical exam, they utilize sophisticated data mining to verify your status. Every applicant must prepare a comprehensive medical timeline before the first consultation. This includes the exact dates of your last treatment session, the contact information for your primary oncologist, and a list of all maintenance medications. Precision is the foundation of a successful application.

Carriers will perform an automated check of your Prescription History and the Medical Information Bureau database. These records reveal every diagnosis and prescription filled over the last seven years. Accuracy is paramount. If a discrepancy exists between your application and these databases, the result is an immediate decline. Our Group identity is built on the belief that preparation prevents failure. The Wise Advisor tip: don’t self-diagnose your eligibility. A professional review of your medical history often reveals paths to coverage you might’ve overlooked. Understanding the best final expense insurance for seniors pros and cons 2026 allows you to approach the application with clarity rather than hope.

The Paul Group Methodology: Curated Final Expense Solutions

Since 2009, our collective expertise has informed a bespoke approach to high-risk cases that many traditional agencies avoid. When you ask, can I get burial insurance if I have cancer, you aren’t just seeking a policy; you’re seeking a strategy. Our methodology rejects the one-size-fits-all model. We curate every plan with the intellectual rigor required to ensure your legacy remains intact. This disciplined intervention allows us to transform a complex medical history into a clear, actionable financial path.

The Paul Group operates as your Wise Advisor. We recognize that a cancer diagnosis requires more than a cold, transactional interaction. Our commitment to seniors in Florida, Illinois, and beyond is rooted in a partnership-driven model that values substance over hyperbole. You deserve a team that understands the intersection of health challenges and financial optimization. For those weighing the pros and cons of final expense insurance, our experts provide the clarity needed to make an informed decision.

Beyond the Policy: A Holistic Partnership

Our commitment extends well beyond the initial underwriting phase. We support families during the claim process to ensure a seamless transition during their most difficult moments. This partnership-driven model ensures that your coverage scales sustainably as your financial needs evolve. By leveraging our Group identity, you access a diverse team of experts dedicated to your organizational clarity. We prioritize long-term stability over quick, superficial fixes; this ensures that your family isn’t left to manage technical complexities alone.

Secure Your Peace of Mind Today

Achieving clarity regarding your final expenses is a simple, non-invasive process. Our team provides a curated quote that reflects your unique medical history and specific legacy goals. When you’re asking can I get burial insurance if I have cancer, the answer often depends on timing and the methodology used to present your case to underwriters. Waiting to apply remains the only true risk, as options can shift with each passing quarter. Procrastination often leads to higher premiums or more restrictive waiting periods. It’s time to finalize your legacy and achieve the organizational clarity your family deserves.

Connect with The Paul Group for a strategic review of your final expense options.

Mastering Your Final Expense Strategy for 2026

Securing a legacy requires a departure from generic insurance models toward a more curated, strategic methodology. The 2026 market presents specific challenges, yet the underlying principles of risk assessment remain consistent. You’ve learned that carrier look-back periods, often spanning 24 months for major treatments, dictate the path between graded and guaranteed acceptance policies. It’s vital to recognize that a medical history doesn’t define your eligibility; rather, it informs the optimization of your coverage. If you are currently wondering, can I get burial insurance if I have cancer, the solution lies in matching your specific health timeline with a carrier’s unique underwriting appetite.

The Paul Group has operated as an independent agency since 2009, maintaining a specialized focus exclusively on senior final expense solutions. We provide a level of expertise that’s particularly essential for residents in Florida and Illinois, where state-specific regulations influence policy availability. Our group doesn’t offer superficial fixes. Instead, we deliver a bespoke alignment of your needs with robust financial instruments designed for structural integrity. Request Your Bespoke Final Expense Strategy from The Paul Group today. Clarity and protection are well within your reach.

Frequently Asked Questions

Can I get burial insurance if I am currently in remission?

You can secure standard burial insurance once you’ve been in remission for at least 24 months. Most carriers categorize applicants into level or graded tiers based on the time elapsed since your last treatment date. If your remission spans more than 3 years, you’ll likely qualify for immediate full benefit coverage at the lowest available rates offered by top tier providers.

What happens if I pass away from cancer during the two-year waiting period?

If you pass away from cancer during the initial 24 month waiting period, your beneficiaries will receive a refund of all paid premiums plus an additional 10 percent interest. This provision, standard in modified or guaranteed issue policies, ensures that your estate recovers the invested capital. Once this two year threshold passes, the policy pays the full death benefit regardless of the cause.

Is skin cancer treated differently than other types of cancer by insurance companies?

Insurance companies treat basal cell and squamous cell carcinomas differently than internal malignancies, often granting immediate coverage without a waiting period. These localized conditions don’t typically impact your eligibility for the best rates or complex underwriting. However, a diagnosis of malignant melanoma usually triggers a 2 year look back period similar to other high risk health events requiring specialized assessment.

Are there burial insurance plans in Florida that don’t require a medical exam?

Florida residents have access to simplified issue and guaranteed issue plans that require no physical medical examinations or blood work. These products utilize a streamlined health questionnaire to determine eligibility instantly through automated prescription database checks. Our Group identifies policies in the Sunshine State that prioritize speed and accessibility for seniors who require a non invasive application process and immediate peace of mind.

How much more does burial insurance cost for someone with a cancer history?

Applicants with a recent cancer history may face premiums that are 20 to 50 percent higher than those for healthy peers, depending on the specific risk tier. The primary keyword can I get burial insurance if I have cancer reflects a common concern about affordability and long term planning. If your diagnosis occurred more than 5 years ago, you’ll often qualify for standard rates with no price inflation.

Can I get coverage if I have been diagnosed with metastatic or stage 4 cancer?

You can obtain coverage with a stage 4 or metastatic diagnosis through a guaranteed issue policy. These plans bypass health questions entirely, ensuring that no applicant is rejected based on medical severity or terminal status. While these policies include a mandatory 2 year waiting period, they offer a reliable path to final expense protection for those facing advanced health challenges that preclude traditional underwriting.

Will my premiums increase if my cancer returns after the policy is in force?

Your premiums will never increase if your cancer returns, provided the policy is already in force and premiums are paid. Burial insurance is a whole life product with locked in rates that remain constant for the duration of the contract. This structural integrity protects your financial plan from the volatility of changing health conditions or future medical diagnoses that might otherwise disrupt your legacy.

Does The Paul Group offer immediate coverage options for seniors in Illinois?

The Paul Group facilitates immediate coverage options for seniors in Illinois through a curated selection of carriers offering first day benefits. Our methodology focuses on aligning your specific health profile with underwriters who view your history favorably. This strategic approach ensures that Illinois families receive robust protection without the standard delays or waiting periods found in mass market products that lack sophisticated tailoring.

Leave a Reply