Final Expense Insurance for Dialysis Patients in Florida, Illinois (2026 Guide)

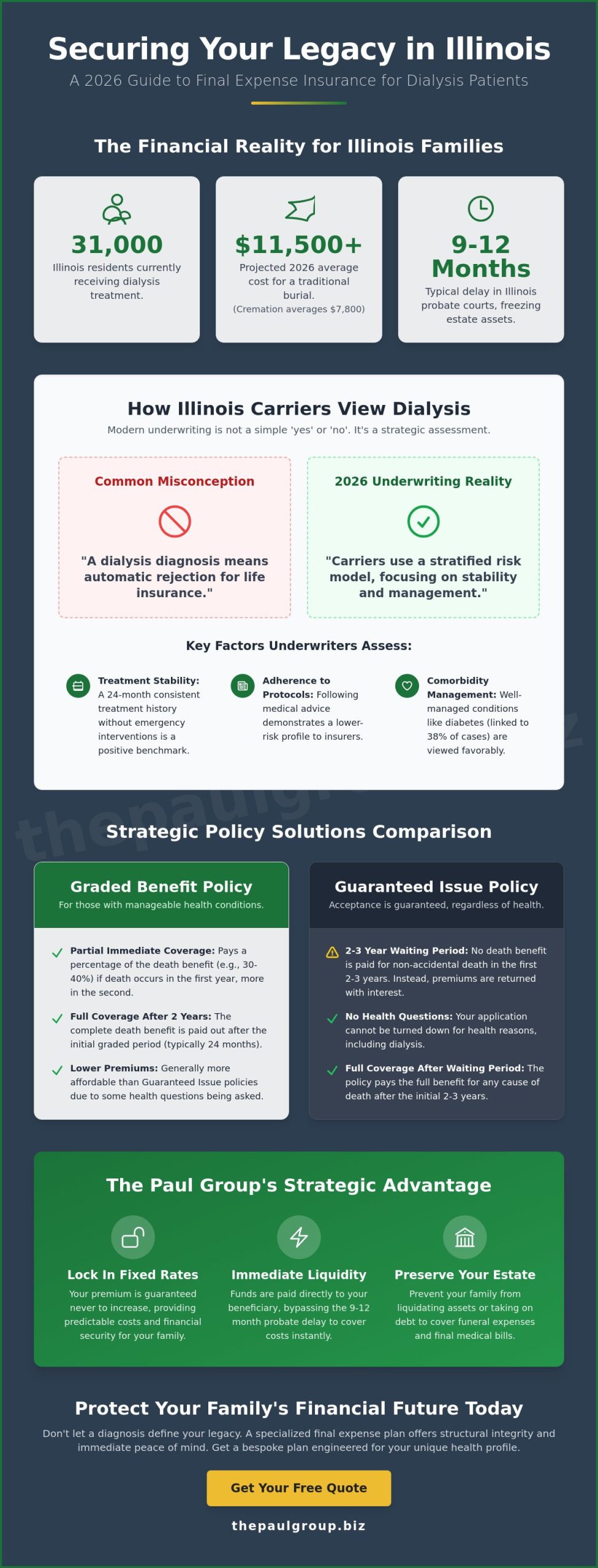

What if the medical necessity of dialysis was no longer the definitive barrier to your family’s long-term financial stability? For the 31,000 residents currently receiving dialysis in Illinois according to 2024 health data, the fear of leaving behind funeral debt often feels like an unavoidable reality. You likely believe that a history of kidney failure guarantees a rejection letter, yet this assumption ignores the specialized pathways available through strategic underwriting. Securing final expense insurance for dialysis patients in Illinois requires a move away from generic policies toward a curated approach that recognizes your specific health profile.

The Paul Group understands that your legacy shouldn’t be defined by a clinical diagnosis. We’ll show you how to lock in a fixed rate that never increases, effectively shielding your children from the costs of final arrangements. This 2026 guide details the methodology for addressing complex regional regulations and avoiding the 12 month average delays common in the state’s probate courts. By the end of this analysis, you’ll possess a clear, logical path toward a bespoke plan that offers both structural integrity and immediate peace of mind.

The Strategic Necessity of Final Expense Coverage in Florida, Illinois

Stability isn’t a luxury; it’s a structural requirement for families navigating the complexities of chronic illness. For those managing the rigors of regular treatment, the 2026 economic environment in the Illinois market presents a multifaceted fiscal hurdle. Dialysis creates a unique intersection of medical dependency and financial vulnerability that requires a disciplined response. Most standard Life insurance products utilize binary underwriting that often penalizes these health conditions, leaving patients with few viable options. This exclusion creates a void that only a curated, high-level strategy can fill.

Securing final expense insurance for dialysis patients in Illinois isn’t merely a transactional purchase. It’s a calculated move to preserve family legacy during a period of intense transition. The Paul Group views insurance as the structural foundation for family stability. We recognize that the emotional burden of dialysis is heavy enough without the added weight of looming debt. By implementing a dedicated policy, you’re not just buying a benefit; you’re engineering a solution that ensures your family’s most complex challenges remain solvable through disciplined intervention.

Projected 2026 Funeral Costs in the Illinois Market

In 2026, industry data suggests the average cost of a traditional burial in the Illinois region will exceed $11,500. This reflects a 4.2% annual inflation rate driven by rising cemetery maintenance fees and labor costs in major hubs like Chicago and Springfield. Even cremation services, often viewed as a cost-effective alternative, have reached a state average of $7,800. These figures represent the baseline expenses, excluding the specialized service charges that often surface during the final planning stages. Families don’t always anticipate these rapid price escalations, which can lead to significant financial strain.

The “financial gap” is the immediate cash deficit between a family’s available liquid assets and the total invoice presented by a funeral provider. Without a dedicated policy, this gap often forces families to liquidate retirement accounts or take on high-interest debt at a moment of deep emotional distress. A strategically aligned final expense policy eliminates this risk by providing a guaranteed influx of capital precisely when it’s required.

The Interplay of Health and Estate Planning

Illinois probate laws are notoriously slow, often freezing estate assets for nine to twelve months before heirs can access them. This delay is catastrophic for families who need to settle immediate medical bills from local clinics or specialized dialysis centers. Final expense policies bypass this lengthy process entirely. They deliver immediate liquidity, functioning as a specialized tool for estate optimization. This cash flow ensures that the estate’s value isn’t eroded by creditors or outstanding healthcare obligations during the transition period.

The Paul Group positions itself as the partner in this complex financial landscape. We focus on the intersection of human needs and operational systems, framing these challenges as opportunities for structural evolution within your estate plan. Our methodology is built on the idea that your coverage should be specifically engineered for your unique health profile. For a deeper analysis of how these tools compare, you can review our insights on the best final expense insurance for seniors to understand the broader strategic context of your options.

Understanding Underwriting: How Illinois Carriers View Dialysis

Securing final expense insurance for dialysis patients in Illinois requires a sophisticated appreciation for the shift in 2026 underwriting methodologies. Insurance carriers no longer apply a binary rejection to renal health challenges. Instead, they utilize a stratified risk assessment model that categorizes applicants based on physiological stability and systemic health. This approach distinguishes between acute kidney injury, which is often a temporary response to surgical trauma, and Chronic Kidney Disease (CKD). Underwriters prioritize the latter’s long-term management. They seek to understand the systemic impact of your condition through a authoritative explanation of dialysis and its frequency. While a common misconception suggests a diagnosis leads to an immediate decline, the reality is more nuanced. Carriers focus on your adherence to treatment protocols rather than the diagnosis itself.

The Impact of Treatment History on Eligibility

Your first dialysis session serves as a critical strategic benchmark for Illinois agents. Carriers typically look for a 24-month window of treatment stability to determine plan eligibility. If you’ve maintained a consistent schedule without emergency room interventions, your risk profile improves. Comorbidities play a vital role in this assessment. Since diabetes accounts for approximately 38% of kidney failure cases, underwriters examine how well you manage blood glucose levels alongside renal treatments. A strategic alignment of your medical records and your application ensures that minor complications aren’t misinterpreted as systemic failures. The Paul Group focuses on these curated details to position your application for the most favorable tier possible. It’s about demonstrating a disciplined approach to your health journey.

Medical Exams vs. Simplified Issue in Illinois

The Paul Group methodology favors simplified issue policies for those managing renal conditions. Traditional medical exams can be counterproductive for dialysis patients. Vital signs often fluctuate during treatment cycles; a single high blood pressure reading during a physical could lead to an inaccurate risk rating. Simplified issue plans bypass the blood draw entirely. Carriers instead utilize a “Prescription Check” to review your history with medications like Aranesp or Phoslyra. This process is efficient. Most Illinois applicants receive an approval decision within 24 to 72 hours. This speed allows for immediate peace of mind without the stress of a physical examination. To better understand these options, you might review our best final expense insurance for seniors pros and cons 2026 guide. We believe in providing a logical path forward through expert advocacy and structural integrity.

Strategic Policy Comparison: Graded vs. Guaranteed Issue

Securing final expense insurance for dialysis patients in Illinois requires a disciplined evaluation of two specific risk-mitigation structures: Graded and Guaranteed Issue plans. These options serve as the primary vehicles for individuals whose health profiles fall outside the parameters of standard underwriting. Carriers utilize a mandatory waiting period, typically 24 months, to stabilize their mortality pools while offering coverage to high-risk applicants. This mechanism ensures the long-term viability of the insurer while providing a clear, albeit delayed, path to full benefit realization for the policyholder.

The choice between these paths hinges on a rigorous cost-benefit analysis. Residents in Florida and Illinois must weigh the immediate premium outlay against the probability of policy maturation. According to the Life Insurance Buyer’s Guide provided by the NAIC, understanding the nuances of these tiered structures is essential for informed decision-making. The Paul Group identity is built on identifying the intersection of affordability and structural integrity, ensuring that the chosen plan aligns with your family’s long-term stability. For a deeper analysis of these variables, review The Paul Group’s 2026 guide on pros and cons.

Graded Death Benefits: A Tiered Approach

Graded plans offer a strategic middle ground for dialysis patients who may still qualify for limited medical underwriting. These policies typically pay out a percentage of the death benefit, such as 30% in year one and 70% in year two, before reaching 100% in the third year. In Illinois, carriers like Mutual of Omaha or Corebridge Financial often provide competitive graded rates for those with managed chronic conditions. A graded plan is superior when the applicant can answer “no” to specific terminal illness questions, as it often results in premiums that are 10% to 15% lower than guaranteed issue alternatives. This curated approach rewards patients whose health has stabilized despite their dialysis requirements.

Guaranteed Acceptance: Coverage Without Questions

Guaranteed acceptance represents the ultimate safety net, requiring no medical exams or health history inquiries. This “No Questions Asked” framework is the primary solution for individuals facing Stage 5 Chronic Kidney Disease (CKD). While these plans maintain a strict 2-year waiting period in Illinois, they provide an ironclad guarantee of acceptance regardless of treatment intensity or frequency.

- No Medical Underwriting: Acceptance is based solely on age and residency.

- Fixed Premiums: Costs never increase, regardless of future health declines.

- Full Payout: 100% of the benefit is paid after the 24-month mark.

Guaranteed issue is the safety net for Stage 5 CKD. We view these policies as a strategic foundation for those who have been exhausted by traditional underwriting denials. It provides a predictable, fixed-cost solution for final expense insurance for dialysis patients in Illinois, ensuring that end-of-life planning is not left to chance.

Navigating the Illinois Application Process with Dialysis

Securing final expense insurance for dialysis patients in Illinois requires a disciplined methodology rather than a reactive approach. The application phase isn’t merely a bureaucratic hurdle; it’s a strategic alignment of your medical reality with an insurer’s risk appetite. Transparency remains your greatest asset. Withholding details about renal treatment or medication schedules can trigger a claim denial during the standard two-year contestability period. A partnership with a specialized broker ensures your history is presented with clarity and precision, protecting your beneficiaries from future litigation or non-payment.

Step-by-Step Roadmap to Approval

Success in the Illinois market depends on meticulous preparation. We recommend a structured five-step progression to move from initial inquiry to active coverage without unnecessary friction.

- Step 1: Document Your Clinical Profile. Gather your specific dialysis schedule and a comprehensive list of medications. Carriers look for stability in treatment patterns over the last 24 months.

- Step 2: Quantify Local Obligations. Determine the exact “Final Expense” amount needed. According to 2023 data from the National Funeral Directors Association, the median cost of a funeral with burial in the East North Central region, which includes Illinois, exceeds $8,300.

- Step 3: Conduct a Multi-Carrier Analysis. Compare at least three Illinois-admitted carriers with your agent. Each firm utilizes different underwriting algorithms for chronic kidney disease.

- Step 4: Review Waiting Period Mechanics. Understand how a graded death benefit functions during the first two years of the policy.

- Step 5: Finalize Beneficiary Designations. Ensure your legal documents align with your insurance policy to prevent probate delays.

Illinois Consumer Rights and “Free Look” Periods

The Illinois Department of Insurance provides robust protections for policyholders to ensure market integrity. One of the most critical tools at your disposal is the “Free Look” period. Under Illinois law, you generally have a window of 10 to 30 days to review your policy after physical or digital delivery. This period allows you to scrutinize the fine print without financial risk. If the terms don’t align with your strategic goals, you can return the policy for a full refund of any premiums paid.

Working with an agency that understands these regional mandates is essential for long-term stability. We focus on structural integrity, ensuring every policy meets the rigorous standards set by state regulators. This bespoke approach transforms a complex medical challenge into a manageable financial plan. You can explore the pros and cons of senior coverage to better understand how these protections fit into a broader legacy strategy. Obtaining final expense insurance for dialysis patients in Illinois is achievable when you leverage these consumer rights alongside professional expertise.

Ready to secure your family’s future with a tailored plan? Connect with our strategic advisors for a curated consultation on your insurance options.

Why The Paul Group is the Strategic Choice for Illinois Seniors

Selecting a partner for your legacy planning is a decision that requires intellectual rigor and a commitment to long-term stability. Since our founding in 2009, The Paul Group has operated as more than a mere brokerage. We’re a collective of strategic advisors dedicated to solving the most complex financial challenges through disciplined intervention. Our dual presence in Florida and Illinois allows us to navigate local market dynamics with a level of precision that off-the-shelf providers simply can’t match.

We reject the transactional nature of modern insurance sales. Instead, we embrace a Wise Advisor methodology. This approach prioritizes strategic alignment between your health profile and carrier underwriting guidelines. We don’t offer generic products. We engineer bespoke interventions that protect your family from the rising costs of final arrangements. It’s about transformation and optimization; we turn a source of anxiety into a pillar of structural integrity for your estate. To understand the full landscape of your options, you can review our analysis of the best final expense insurance for seniors pros and cons before making your final determination.

Tailored Solutions for Complex Health Profiles

Securing final expense insurance for dialysis patients in Illinois requires a nuanced understanding of the regional carrier landscape. Many providers view renal health through a lens of risk; we view it as a requirement for specialized curation. Our team identifies kidney-friendly carriers that offer competitive rates even for those undergoing active treatment. This holistic methodology ensures that your coverage isn’t just a temporary fix but a sustainable scaling of your family’s financial security. We provide the warmth of a partnership combined with the professional reassurance of high-level industry expertise.

Next Steps: Securing Your Legacy

Your path toward clarity begins with a focused executive briefing. When you reach out to us, you won’t experience a high-pressure sales environment. You’ll engage in a structured consultation designed to diagnose your needs before prescribing a solution. We’ll review your specific dialysis protocol to ensure the carriers we recommend are the right fit for your unique medical DNA. It’s time to replace uncertainty with a logical, forward-looking plan.

- Strategic Assessment: We analyze your health and financial goals to identify potential gaps.

- Curated Selection: We present options from our hand-selected carrier list based on Illinois-specific availability.

- Disciplined Implementation: We handle the administrative complexities to ensure your legacy is secure.

Don’t leave your family’s future to chance. Request your Illinois final expense quote today and experience the difference of a strategic partnership.

Strategic Certainty for Your Illinois Legacy

Managing the complexities of a dialysis diagnosis shouldn’t preclude you from establishing a robust financial foundation for your family. Since 2009, The Paul Group has applied specialized high-risk expertise to navigate the nuances of Illinois-admitted insurance carriers, providing clarity where others find confusion. We’ve demonstrated that the choice between graded and guaranteed issue policies is a critical structural decision that requires alignment with specific carrier underwriting standards. By eliminating medical exams for simplified issue plans, we focus on the structural integrity of your coverage rather than the obstacles of your medical history. Securing final expense insurance for dialysis patients in Illinois requires this level of curated expertise to ensure your final wishes are honored without compromise. You’ve spent a lifetime building your legacy; we ensure it remains protected through disciplined intervention and holistic planning. Our methodology prioritizes long-term stability, ensuring your family isn’t left with the burden of sudden expenses.

Secure your family’s future with a bespoke final expense plan from The Paul Group

We’re here to guide you toward a future defined by stability and peace of mind.

Frequently Asked Questions

Can I get life insurance if I just started dialysis in Illinois?

Yes, you can secure coverage through specialized guaranteed issue contracts that bypass traditional medical underwriting. While standard life insurance providers often decline applicants currently receiving treatment, certain carriers prioritize accessibility for those with chronic conditions. Our strategic approach identifies these specific providers to ensure Illinois residents establish a financial foundation regardless of their clinical status or treatment duration.

How much does burial insurance cost for a dialysis patient in 2026?

Premiums are primarily determined by your age and the total death benefit rather than your specific medical diagnosis. In 2026, industry data indicates that guaranteed issue rates remain consistent with previous years, though they command a higher price point than plans requiring medical exams. We focus on optimizing your monthly budget to ensure the benefit covers the average 12,000 dollar cost of a traditional funeral.

Is there a waiting period for final expense insurance in Illinois?

Most carriers implement a 24 month waiting period for applicants managing end stage renal disease. This structural safeguard is a standard component of risk management within the high risk insurance sector. It ensures the long term solvency of the provider while offering a guaranteed path to full protection. After this two year milestone, the policy pays the full death benefit to your beneficiaries.

Will I need a medical exam to qualify for coverage in Florida, Illinois?

You won’t need to undergo a physical examination or provide blood samples to secure a policy. Final expense insurance for dialysis patients in Illinois typically utilizes simplified or guaranteed underwriting methodologies. This streamlined process focuses on a series of health questions or eliminates medical inquiries entirely to facilitate rapid approval. It’s a bespoke solution engineered for those who require efficiency and certainty.

What happens if I pass away during the graded period of my policy?

Your beneficiaries receive a return of all premiums paid plus an additional 10 percent interest if death occurs during the initial graded period. This mechanism protects your capital investment while the policy matures toward its full valuation. It represents a disciplined approach to risk, ensuring that your estate receives the resources you’ve contributed plus a modest growth factor during the waiting phase.

Are there Illinois state programs that help with funeral costs for dialysis patients?

The Illinois Department of Human Services manages a Funeral and Burial Program that provides up to 1,103 dollars for funeral expenses and 552 dollars for burial costs. These state resources function as a minimal safety net and are subject to strict asset limitations. We recommend integrating private insurance to bridge the 10,000 dollar gap between state aid and actual market costs for professional services.

Can I get coverage if my kidney failure was caused by diabetes?

Yes, final expense insurance for dialysis patients in Illinois remains accessible even when kidney failure is a secondary complication of diabetes. Insurance providers categorize these cases under specific risk tiers that acknowledge the complexity of comorbid conditions. Our methodology involves aligning your health profile with carriers that have a documented history of accepting multi system challenges, ensuring your dual diagnosis doesn’t prevent financial security.

Does The Paul Group offer immediate coverage options for Illinois residents?

The Paul Group specializes in curated strategies that prioritize long term stability over superficial fixes that often fail during the claims process. For individuals on dialysis, immediate full death benefit coverage is rarely available due to 2026 actuarial standards. We focus on structural alignment, securing the most robust graded policies that transition into full coverage as quickly as the regulatory environment allows.

Leave a Reply