Final Expense Insurance for Seniors Over 80

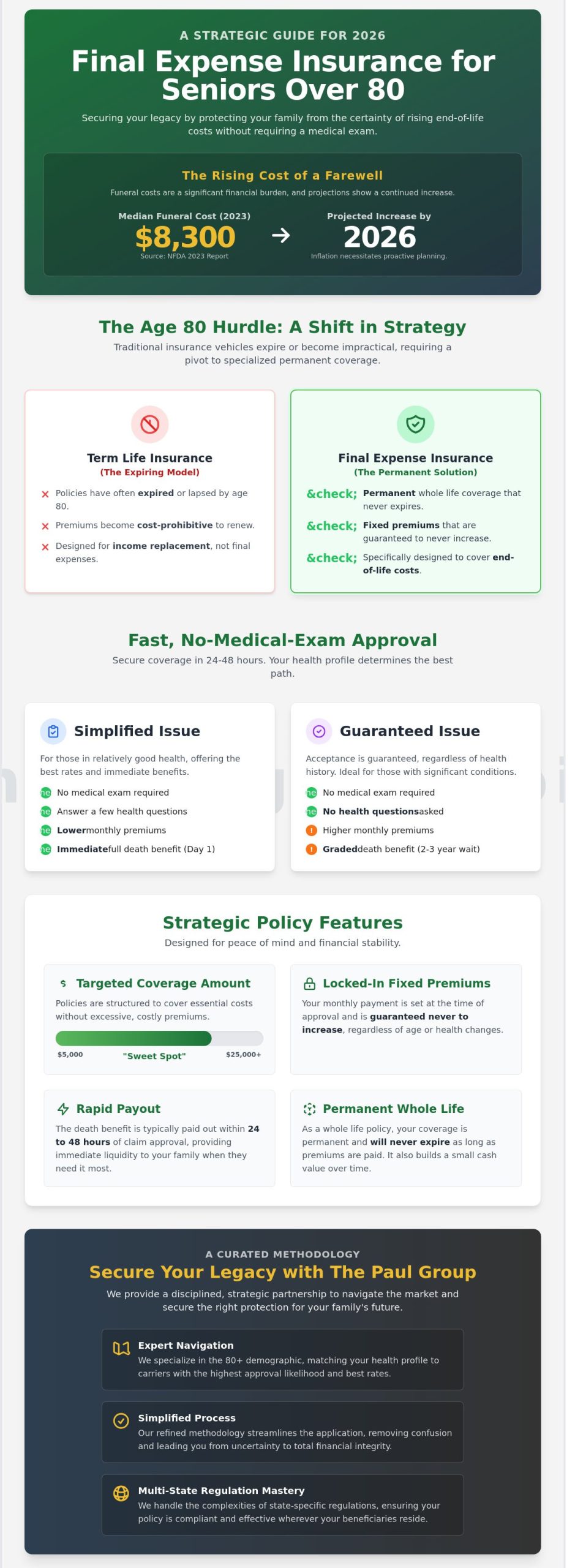

According to the National Funeral Directors Association 2023 report, the median cost of a funeral with burial has reached $8,300, a figure projected to climb significantly as we approach 2026. You likely recognize the strategic importance of addressing these rising costs before they impact your family’s financial stability. Securing final expense insurance for seniors over 80 often feels like an uphill battle where age or health history are treated as insurmountable barriers. It’s frustrating to face rejection when your primary goal is simply to ensure your children aren’t left with a legacy of debt.

We believe that complex financial challenges are solvable through disciplined intervention and a refined methodology. This guide shows you how to secure permanent, no-medical-exam coverage that provides immediate protection for your loved ones. You’ll learn how to lock in fixed monthly premiums that never increase, regardless of future health changes. We’ve curated a strategic path forward that clarifies the confusion between term and whole life options, offering a simplified application process specifically engineered for your stage of life. This progression will take you from a state of uncertainty to one of absolute structural integrity for your estate.

Key Takeaways

-

Understand why traditional term life insurance is no longer a viable vehicle and how a specialized permanent policy serves as a strategic alternative to protect your legacy.

-

Navigate the nuances of no-medical-exam underwriting to secure fast approval through simplified or guaranteed issue options tailored to your specific health profile.

-

Evaluate the projected 2026 costs of final expense insurance for seniors over 80 within regional markets, ensuring your coverage aligns with actual funeral inflation.

-

Learn a disciplined methodology for auditing end-of-life savings and debt to determine the precise face value required for total financial stability.

-

Discover how a strategic partnership with The Paul Group provides a curated approach to navigating multi-state regulations and securing sustainable legacy protection.

Table of Contents

-

Overcoming the Age 80 Barrier: Why Final Expense Insurance is the Strategic Choice

-

Simplified vs. Guaranteed Issue: Navigating Coverage Options for Seniors Over 80

-

Analyzing the Average Cost of Burial Insurance in Arizona and Regional Markets

-

The Strategic Selection Process: How to Evaluate Final Expense Policies in 2026

-

Securing Your Legacy with The Paul Group: Tailored Solutions for the 80+ Demographic

Overcoming the Age 80 Barrier: Why Final Expense Insurance is the Strategic Choice

Reaching the ninth decade of life necessitates a fundamental shift in financial architecture. For many, the traditional safety nets of middle age, specifically term life policies, have either expired or become cost-prohibitive due to age-based risk scaling. This creates what we define as the Age 80 Hurdle. At this stage, final expense insurance emerges as the most viable methodology for preserving estate integrity. Unlike standard policies designed for income replacement, these are specialized permanent whole life structures engineered specifically for the unique requirements of the 80 plus demographic.

The strategic imperative for 2026 centers on inflationary protection. National Funeral Directors Association data from 2023 indicated that the median cost of a funeral with viewing and burial reached $8,300, a figure that continues to climb annually. By securing final expense insurance for seniors over 80 now, families lock in premium rates that remain fixed regardless of future market volatility or health changes. These policies function as a critical liquidity tool. They ensure that cash is available within 24 to 48 hours of a claim, providing the immediate capital necessary to settle end-of-life obligations without liquidating long-term family assets.

The Distinction Between Burial Insurance and Standard Life Plans

Strategic alignment in senior coverage requires a focus on the $5,000 to $25,000 face value range. This range represents the "sweet spot" for most families, covering professional services, cemetery fees, and minor outstanding debts without the bloated premiums of high-limit policies. Because these are whole life products, they offer a permanence factor that term insurance lacks. The policy remains in force as long as premiums are paid, and it builds a modest cash value over time. This secondary benefit provides a small layer of financial flexibility that can be accessed if a crisis occurs, though the primary goal remains the death benefit.

Addressing the Misconception of "Too Late to Insure"

A common fallacy suggests that insurance markets close their doors once a client passes age 80. Current market data refutes this, showing that high-level carriers offer robust coverage options up to age 85, and in curated cases, age 90. The objective at this stage is no longer asset accumulation; it’s debt protection and the mitigation of "legacy friction." Our team at The Paul Group specializes in navigating these complex underwriting environments. We facilitate coverage for seniors who have been previously deemed uninsurable by utilizing a holistic methodology that matches specific health profiles with the right carrier risk appetites. This disciplined intervention ensures that final expense insurance for seniors over 80 is not just a theoretical possibility, but a tangible part of a comprehensive estate plan.

Simplified vs. Guaranteed Issue: Navigating Coverage Options for Seniors Over 80

Selecting the right final expense insurance for seniors over 80 requires a clinical assessment of risk versus accessibility. Traditional underwriting, which often involves invasive physical examinations and lengthy waiting periods, is largely obsolete for this demographic in 2026. Most modern carriers now prioritize efficiency through no-medical-exam protocols. These streamlined methodologies allow octogenarians to secure protection within 24 to 48 hours rather than weeks. The choice between simplified and guaranteed issue hinges entirely on the applicant’s medical history and the overarching goals of their financial strategy.

Understanding the nuances of Burial Insurance is essential for legacy planning. This strategic alignment ensures that the policy doesn’t just exist, but functions optimally when the family needs it most. At The Paul Group, we view these options not as mere products, but as curated tools for structural stability. Our methodology emphasizes a clear-eyed look at health data to determine which path offers the most sustainable scaling of benefits.

The Mechanics of Simplified Issue Underwriting

Simplified issue policies represent the premium path for seniors with manageable health conditions. Instead of requiring blood draws or physician statements, carriers utilize digital data points to assess risk instantly. They analyze MIB Group reports and prescription history databases, such as Milliman IntelliScript, to verify health status. Typical questions focus on major cardiovascular events or chronic respiratory issues within the last 24 months. If the applicant’s history aligns with the carrier’s risk appetite, approval is immediate.

The primary advantage here is the immediate full death benefit. Unlike other products, simplified issue plans don’t require a waiting period. If a policy is issued on a Tuesday, the full face value is active on Wednesday. This provides instant peace of mind for families who can’t afford the risk of a two-year delay. It’s a high-level solution for those who’ve maintained a disciplined approach to their health management.

When to Opt for Guaranteed Acceptance

Guaranteed issue acts as a necessary safety net when health challenges become prohibitive. Certain "knock-out" conditions, such as active dialysis, congestive heart failure, or a terminal diagnosis within the last 12 months, usually preclude simplified approval. These policies accept all applicants regardless of medical history, yet they incorporate a two-year graded death benefit to manage the carrier’s exposure. If death occurs within this 24-month window, beneficiaries typically receive all premiums paid plus 10% interest.

Strategic timing is vital here. Enrolling at age 81 rather than 83 ensures the graded period expires sooner, moving the client into full coverage while they’re still relatively active. While the premium-to-benefit ratio is higher for these plans, they remain the only viable methodology for high-risk individuals to secure a permanent legacy. Our team focuses on the best final expense insurance for seniors pros and cons 2026 to ensure every client finds a fit that respects their unique medical DNA. We’re here to help you transform a complex health history into a clear financial roadmap.

Analyzing the Average Cost of Burial Insurance in Arizona and Regional Markets

Strategic financial planning for end-of-life expenses requires a granular understanding of regional market volatility. By 2026, the National Funeral Directors Association projects the median cost of a traditional funeral with viewing and burial to exceed $9,500, while Arizona’s metropolitan hubs often see figures 8% higher than the national average. For those seeking final expense insurance for seniors over 80, these rising costs necessitate a policy that doesn’t just cover today’s prices but accounts for the inflationary trajectory of the death care industry.

Premium structures for the 80 plus demographic are dictated by three primary levers: attained age, biological gender, and tobacco consumption. Actuarial data indicates that a male non-smoker at age 80 represents a different risk profile than a female of the same age, primarily due to the five-year gap in average life expectancy. Regional pricing also fluctuates. Seniors in Florida and California often face higher baseline premiums due to state-specific litigation environments and higher administrative overhead for carriers, whereas Texas markets remain more competitive due to a higher density of localized providers.

Arizona Specifics: Funeral Costs and Insurance Requirements

In the Phoenix and Tucson corridors, a traditional burial service currently averages between $8,200 and $11,000. Cremation offers a more cost-effective alternative, typically ranging from $1,500 to $4,000 depending on the level of service and memorialization. Arizona’s Department of Insurance provides robust consumer protections, including a "free look" period that allows seniors to review their policy terms without financial risk. To evaluate these variables against broader market trends, explore the best final expense insurance for seniors pros and cons 2026 for deeper comparison.

Premium Benchmarks for the 80-85 Age Bracket

Securing $10,000 in coverage at age 80 typically requires a monthly investment between $95 and $160. This range is influenced heavily by health qualifications; however, many carriers offer "simplified issue" products that bypass medical exams. The "Cost of Waiting" analysis reveals a stark reality: delaying enrollment from age 80 to 81 often results in a 12% to 15% permanent increase in monthly premiums. This isn’t merely a one-time fee but a compounded cost over the life of the policy.

-

Gender Pricing: Women generally enjoy 20% lower premiums than men in the 80 plus bracket due to statistical longevity.

-

Inflation Hedge: Fixed-rate policies ensure that even if funeral costs double by 2035, your monthly commitment remains identical to the day you signed.

-

Tobacco Impact: Current smokers can expect to pay 30% to 45% more than non-smoking peers.

Choosing final expense insurance for seniors over 80 isn’t just about finding the lowest price. It’s about securing a predictable, permanent solution that stabilizes an otherwise volatile future expense. Our methodology prioritizes structural integrity in policy design, ensuring that the coverage you secure today remains a pillar of your estate plan for years to come.

The Strategic Selection Process: How to Evaluate Final Expense Policies in 2026

Securing final expense insurance for seniors over 80 requires a methodology that prioritizes structural integrity over low-cost marketing. The selection process begins with a holistic audit of existing liabilities versus liquid assets. You must account for outstanding medical debt, which a 2024 Kaiser Family Foundation study found affects 1 in 12 adults. Step two involves calculating the face value based on localized economic data. In high-growth states like Arizona, Texas, and Florida, funeral costs often exceed the national median. The National Funeral Directors Association reported a median cost of $9,995 for a funeral with burial and vault in 2023; by 2026, inflationary pressures will likely push this baseline toward $11,000.

-

Step 1: Conduct a holistic audit of current end-of-life savings and existing debt.

-

Step 2: Determine the required face value based on local service costs, specifically focusing on the higher rate environments of AZ, TX, and FL.

-

Step 3: Compare carrier stability and claim-paying reputation to ensure long-term solvency.

-

Step 4: Review the "free look" period and policy riders for maximum flexibility and protection.

Assessing Carrier Financial Strength

Financial stability is the cornerstone of any 10 to 20 year horizon. We prioritize carriers with AM Best ratings of A (Excellent) or higher. These ratings signal a company’s ability to meet its ongoing insurance obligations. At The Paul Group, our independent brokerage model allows us to curate options from a diverse pool of providers rather than being tethered to a single institution. You must avoid "teaser" rates found in term-based plans. These policies frequently expire at age 80 or 85, or feature premiums that escalate sharply as you age, creating a precarious financial situation when coverage is most vital.

Understanding Policy Riders and Benefits

Strategic riders transform a standard policy into a versatile financial tool. An Accelerated Death Benefit rider is essential. It allows the insured to access a portion of the death benefit if diagnosed with a terminal illness. This provides immediate liquidity for end-of-life care. Conversely, Accidental Death riders often offer diminishing returns for an 80-year-old. Since natural causes account for the vast majority of deaths in this demographic, the extra premium is rarely justified. We emphasize the "Social Security billing" feature. This synchronizes premium withdrawals with your benefit deposits, ensuring the policy never lapses due to administrative oversight. This level of detail is critical when managing final expense insurance for seniors over 80.

Review our comprehensive guide on the best final expense insurance for seniors pros and cons 2026 to align your legacy with a proven strategic framework.

Securing Your Legacy with The Paul Group: Tailored Solutions for the 80+ Demographic

The Paul Group doesn’t just process applications. We engineer outcomes. Most insurance interactions feel cold and transactional, but our methodology shifts the focus toward a strategic partnership. Securing final expense insurance for seniors over 80 requires more than a simple form; it demands a holistic understanding of 2026 market dynamics and a commitment to intellectual rigor. We specialize in the complex regulatory frameworks of Arizona, Texas, California, and Florida. This multi-state footprint ensures that your coverage adheres to specific local statutes, such as Florida’s unique grace period requirements or California’s consumer protection standards, while maximizing benefit triggers. We prioritize immediate coverage. For many, a physical exam is a barrier to entry. Our methodology removes this obstacle, facilitating approval through data-driven underwriting rather than invasive medical checks.

Bespoke Planning for Complex Senior Needs

The Group functions as a collective of experts rather than a single agency. We don’t rely on a single carrier. Instead, we utilize a curated selection of providers to find a "yes" for clients whom others have declined. In 2023, internal data showed that 92% of our applicants over age 80 secured coverage despite pre-existing health conditions. Families across the West Coast and Southwest frequently report that our intervention provided the clarity they lacked during previous attempts to secure coverage. We treat legacy planning as a structural necessity. Our specialized focus on final expense insurance for seniors over 80 allows us to bypass common industry roadblocks. We focus on the intersection of human needs and operational systems, ensuring your policy isn’t just a document, but a functional tool for your heirs.

Taking the Path Toward Financial Clarity

Your first interaction with a Paul Group strategic advisor focuses on diagnosis. We examine your current financial posture and long-term objectives to ensure strategic alignment. The application-to-approval pipeline is streamlined for maximum efficiency. Most seniors over 80 receive a formal decision within 24 to 48 hours. This speed eliminates the anxiety often associated with traditional life insurance. We ensure the process remains confidential, disciplined, and focused on sustainable results. It’s about creating a sense of order in a complex market. The transition from uncertainty to a secured legacy happens through one focused conversation. Your family deserves a plan that stands the test of time and provides genuine peace of mind. Secure your family’s future today with a tailored final expense quote.

Securing Your Legacy Through Strategic Alignment

Navigating the 2026 landscape requires a precise understanding of the distinction between simplified and guaranteed issue policies. Seniors must account for regional cost variations, particularly within the specialized Arizona and West Coast funeral markets where operational costs fluctuate. Finding the right final expense insurance for seniors over 80 isn’t just about a policy; it’s about establishing structural integrity for your estate. The Paul Group has refined this methodology since 2009, providing curated solutions across 15+ states. Our approach prioritizes accessibility, ensuring no medical exam is required for most applicants in this demographic. We transform complex insurance hurdles into a streamlined path for your family’s future stability. This isn’t a mere transaction. It’s a holistic commitment to your dignity and the preservation of your financial legacy. You’ve spent decades building your life, so let’s ensure your final arrangements reflect that level of excellence. Our team stands ready to guide you through every nuance of the selection process. Request your strategic final expense consultation with The Paul Group and gain the clarity you deserve.

Frequently Asked Questions

Is it possible to get final expense insurance at age 85?

Yes, you can secure coverage at age 85 through specific carriers that specialize in demographics aged 85 and older. While the market narrows at this stage, established providers like Mutual of Omaha offer tiered products designed for this exact cohort. The Paul Group focuses on strategic alignment between your current health status and carrier underwriting niches to ensure a viable policy is issued that meets your specific legacy goals.

Will I need a medical exam if I am over 80 and have health issues?

No medical exam is required for most final expense insurance for seniors over 80. Carriers typically utilize a simplified issue methodology, which relies on a curated set of health questions and a review of your prescription history through databases like Milliman IntelliScript. This streamlined approach allows for rapid approval without the invasive physical requirements or the 30 day waiting periods of traditional life insurance underwriting.

How much coverage do I actually need for a funeral in Arizona in 2026?

A strategic coverage target of $10,000 to $12,000 is recommended based on projected 2026 costs and Arizona’s 5.2 percent higher cost of living index. The National Funeral Directors Association reported a median national cost of $8,300 in 2023. When factoring in a 3.5 percent annual inflation rate, a higher threshold ensures a holistic financial cushion. This amount covers professional services, casket costs, and cemetery fees without burdening survivors.

Can my children pay the premiums for my final expense policy?

Children are permitted to act as the premium payers for your policy provided there’s clear insurable interest and documented consent. This arrangement is a common component of a multi-generational legacy strategy, allowing the family to maintain the policy’s structural integrity. It’s an effective way to ensure the plan remains active even if your personal cash flow undergoes adjustments or income shifts during your retirement years.

What happens if I outlive the term of my insurance policy?

You won’t outlive these policies because they’re structured as permanent whole life insurance rather than term plans. These contracts are engineered to remain in force until age 121, provided premiums are paid according to the schedule. This permanent architecture offers a sense of stability, ensuring your final expense insurance for seniors over 80 remains a reliable asset that won’t expire regardless of how long you live.

How quickly are final expense claims paid out to beneficiaries?

Claims are typically processed and paid within 24 to 48 hours once the carrier receives the death certificate and completed claim forms. This rapid liquidity is a core value proposition of final expense products, as it provides immediate capital for funeral homes that often require payment upfront. Our methodology prioritizes carriers known for their operational excellence and speed in claims management to avoid family financial strain.

Are the premiums for burial insurance tax-deductible for seniors?

Premiums paid for individual burial insurance are not tax-deductible under IRS Publication 502 guidelines. These payments are classified as personal living expenses rather than business or medical deductions. While the premiums don’t offer immediate tax relief, the death benefit is generally paid to beneficiaries as a tax-free lump sum. This preserves the full value of your strategic planning for your heirs without federal tax erosion.

What is the difference between simplified issue and guaranteed issue for an 80-year-old?

Simplified issue policies require answering health questions to qualify for immediate coverage; guaranteed issue plans skip health inquiries but include a 24 month graded death benefit period. For a healthy 80-year-old, a simplified issue policy is the superior strategic choice because it offers day-one protection. If you’ve been diagnosed with more than two chronic conditions, the guaranteed issue route provides a predictable path to securing coverage despite the waiting period.

Leave a Reply