The Strategic Guide to Types of Life Insurance in 2026: Navigating Options from Florida to California

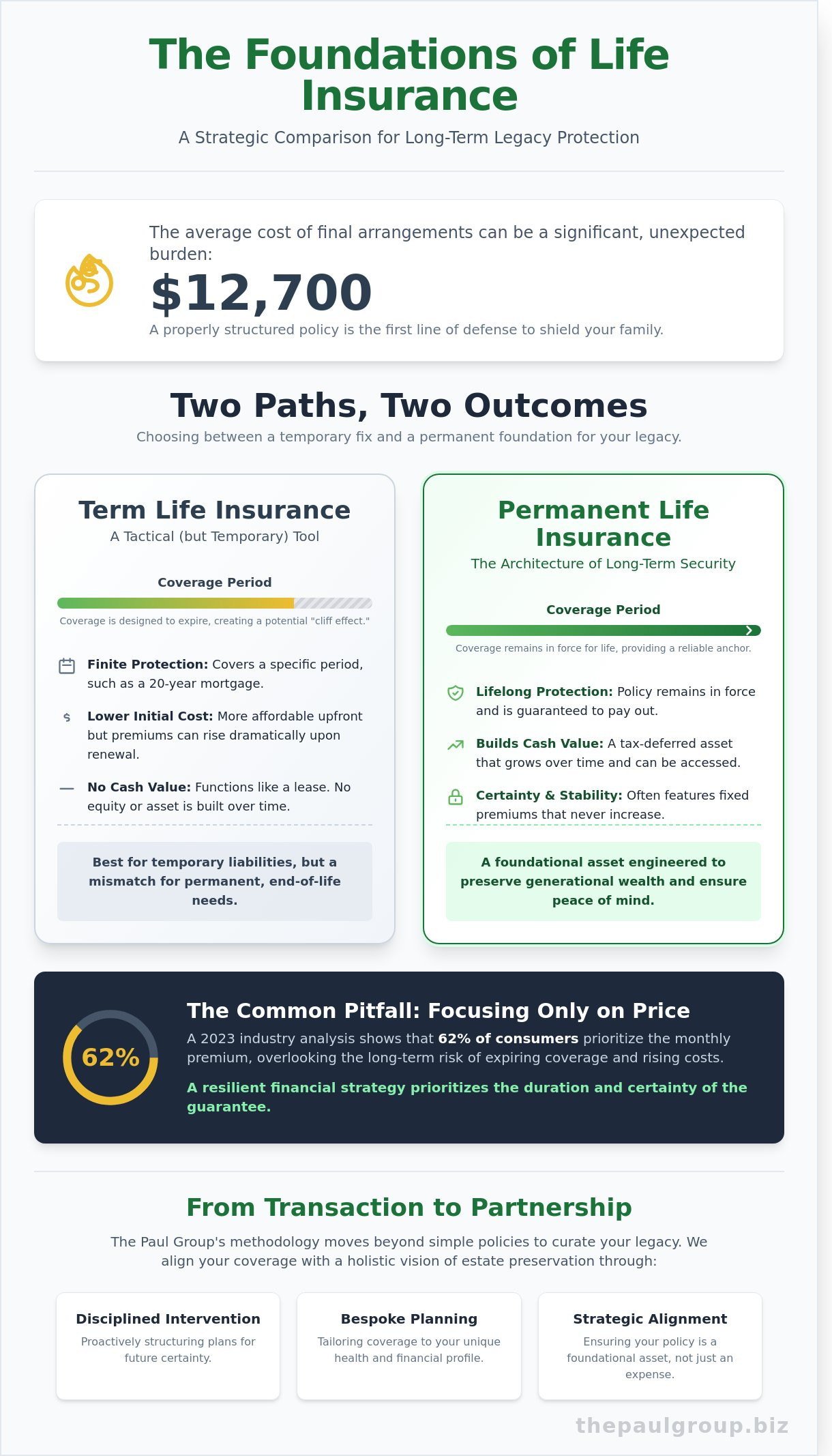

What if the most expensive mistake you make this year isn’t a lost investment, but the policy clause you didn’t understand? You likely believe that shielding your children from the $12,700 average cost of final arrangements is a non-negotiable priority. Yet, the complexity of modern financial products often creates more anxiety than it resolves. It’s frustrating to face health-based rejections or the looming threat of rising premiums when you simply want certainty. Understanding the distinct types of life insurance is the first step toward reclaiming control over your estate’s legacy.

Since protecting a home is one of the most common reasons families purchase life insurance, it’s a good idea to find out more about Mortgage Protection to see how these policies work in detail.

The Paul Group offers a sophisticated analysis of policy structures designed to secure your family’s long-term financial integrity through immediate coverage and fixed rates. We focus on the optimization of your coverage to ensure it aligns with your unique health profile and geographic requirements. This guide provides a strategic overview of the 2026 landscape from Florida to California; it offers a clear path to end-of-life peace of mind through disciplined intervention and bespoke planning. You’ll discover how to bypass administrative confusion and secure a foundation that remains unshakable for decades to come.

Key Takeaways

- Distinguish between temporary risk mitigation and permanent legacy building to select a structure that preserves your family’s long-term financial integrity.

- Analyze the strategic nuances of various types of life insurance, focusing on how Whole and Universal policies provide the predictability required for structural stability.

- Explore Final Expense insurance as a curated solution specifically engineered to address end-of-life costs and medical liabilities with surgical precision.

- Understand how regional economic landscapes in states like Florida and California influence policy selection and the optimization of state-specific consumer protections.

- Learn to transition from a transactional mindset toward a partnership-driven methodology that aligns your coverage with a vision of holistic estate preservation.

Understanding the Foundations: The Two Primary Categories of Life Insurance

Strategic financial planning begins with a fundamental distinction between simple risk mitigation and long-term legacy architecture. At its core, life insurance serves as a hedge against the economic void created by an untimely death; however, viewing this asset solely through the lens of a monthly bill ignores its potential as a sophisticated tool for capital preservation. Understanding the two primary categories of life insurance is essential for families who prioritize structural integrity over superficial fixes. Every decision must be rooted in a methodology that balances current cash flow with future liquidity needs.

The Paul Group categorizes these vehicles based on their ultimate objective. One seeks to cover a specific, finite liability. The other aims to provide a permanent foundation for generational wealth. Selecting between these types of life insurance requires looking past the immediate premium to evaluate the total internal rate of return and the certainty of the payout. A 2023 industry analysis suggests that while 62% of consumers focus primarily on the monthly price, the most resilient portfolios prioritize the duration of the guarantee and the quality of the underlying carrier.

Term Life Insurance: A Tactical But Temporary Tool

Term insurance functions as a high-leverage, temporary solution for specific debt obligations. It’s often utilized to cover a 20-year mortgage or the 22-year window of a child’s education. These policies offer pure protection without any equity component. While the initial cost is lower, the structure is inherently fragile because it’s designed to expire. This creates a “cliff effect” for many families. If a policyholder reaches age 75 and their 30-year term ends, they’re suddenly left without coverage at the exact moment their mortality risk is highest. The Paul Group views term coverage as a mismatch for final expense needs. It’s a tactical lease, not a permanent asset, and it lacks the strategic alignment required for lifelong security.

Permanent Life Insurance: The Architecture of Long-Term Security

Permanent structures provide the quiet confidence that comes from knowing a plan is built to last. Unlike term products, these policies remain in force for the duration of the insured’s life, provided premiums are paid. This stability is achieved through a fixed death benefit and the accumulation of cash value. This cash component grows on a tax-deferred basis, offering a secondary benefit that can be accessed during the policyholder’s lifetime for strategic opportunities or emergency liquidity. In a market where volatility is constant, the structural certainty of a permanent policy offers a reliable anchor. It ensures that the transition of wealth isn’t a matter of “if,” but “when.”

Choosing the right types of life insurance involves a disciplined intervention into your family’s financial future. It’s about moving from a state of vulnerability to a state of clarity. Short-term savings on a monthly premium can lead to catastrophic gaps in coverage during your 8th or 9th decade of life. A bespoke approach considers the intersection of human leadership and operational systems, ensuring your insurance aligns with your broader estate goals. We focus on sustainable scaling for your family’s legacy, ensuring that the protection you put in place today remains robust 50 years into the future. This requires a shift from transactional thinking to a partnership-driven strategy.

A Strategic Deep Dive into Permanent Policy Variations

Permanent insurance represents a lifetime commitment to financial structural integrity. Unlike temporary solutions, these instruments function as curated assets within a broader estate architecture. Understanding the nuances of different strategic deep dive into permanent policy variations allows families to move beyond basic protection toward legacy optimization. We view these types of life insurance not merely as expenses, but as foundational pillars for multi-generational wealth transfer. A well-engineered permanent policy provides a level of durability that term products cannot match, specifically regarding the accumulation of tax-deferred equity.

- Whole Life: Delivers absolute predictability with fixed premiums and guaranteed cash value growth, often enhanced by non-guaranteed dividends.

- Universal Life: Offers a modular approach where premium payments and death benefits can be adjusted as your family’s financial liquidity changes over decades.

- Variable Life: Connects policy performance directly to equity sub-accounts, prioritizing capital appreciation for those with higher risk tolerances and a long-term horizon.

- Indexed Universal Life (IUL): Utilizes a methodology that tracks market indices like the S&P 500 while maintaining a 0% floor to prevent principal loss during market contractions.

Whole Life: The Bedrock of Senior Planning

Certainty is the ultimate luxury in estate planning. Whole life insurance provides this through level premiums that remain locked at the age of issue. A policyholder who secures coverage at age 45 will pay the exact same amount at age 85. This stability creates a predictable cash flow model for long-term budgeting. According to 2023 LIMRA data, whole life continues to command 35% of the total market premium because of this inherent reliability. The Wise Advisor approach favors this simplicity. It removes the variable of market timing from the legacy equation. For many families, the most sophisticated choice is the one that guarantees a result regardless of external economic volatility. It’s a disciplined intervention against the unpredictability of the future, ensuring that the death benefit remains a fixed point in an ever-changing financial landscape.

Universal and Variable Options: Assessing Complexity vs. Reward

Flexible policies require active management and intellectual rigor. Universal structures suit high-net-worth individuals who want to overfund their policies during high-income years to accelerate cash value growth. However, the moving parts demand scrutiny. The cost of insurance within these policies typically rises as the insured ages. If the internal cash value doesn’t grow at a rate sufficient to cover these rising costs, the policy could lapse without additional capital. Variable structures expose the death benefit to market volatility directly. In a 10% market downturn, a poorly funded variable policy might require an unplanned capital infusion to remain in force. This risk is often unacceptable for those on fixed incomes who require absolute stability. We believe structural alignment with your 10-year financial trajectory is more critical than chasing hypothetical 8% returns.

Strategic selection involves balancing these mechanics against your family’s unique DNA. In 2023, IUL sales accounted for 25% of all individual life insurance premiums, reflecting a growing demand for downside protection combined with upside potential. This trend suggests that modern families value a holistic blend of safety and opportunity. If you’re seeking a bespoke insurance methodology tailored to your specific goals, the choice of vehicle must be deliberate. The Paul Group views this selection process as a transformation of risk into a sustainable scaling of your family’s financial security. Every decision should serve the long-term structural integrity of your estate, moving you from a state of complexity to one of absolute clarity.

Final Expense Insurance: The Bespoke Solution for End-of-Life Costs

Final expense insurance represents a specialized evolution of permanent coverage, engineered specifically to manage the immediate financial liabilities that follow a passing. While traditional policies focus on long-term income replacement, this bespoke solution for end-of-life costs targets the granular expenses that often catch families off guard. It’s a subset of whole life insurance, meaning the premiums remain locked and the death benefit is guaranteed as long as payments continue. Our methodology at The Paul Group treats this not just as a policy, but as a strategic exit plan for the individual’s estate.

The strategic focus here is narrow and effective. According to 2023 data from the National Funeral Directors Association, the median cost of a funeral with burial and viewing has risen to approximately $8,300. When you factor in late-stage medical bills and the legal fees associated with probate, the total financial impact frequently exceeds $15,000. Final expense policies are designed to absorb these shocks instantly. By focusing on smaller face amounts, typically ranging from $5,000 to $50,000, seniors can secure a high-utility asset without the prohibitive premiums of a million-dollar policy. It’s a lean, efficient use of capital.

Beyond the spreadsheets, the psychological relief this provides a family is immeasurable. There is a profound shift in the grieving process when a beneficiary knows a check is already earmarked for the service. It eliminates the need for “GoFundMe” campaigns or the liquidation of family heirlooms. We’ve observed that this clarity transforms a period of potential organizational chaos into a period of structured, dignified transition. Knowing the liquidity is there allows the family to focus on legacy rather than logistics.

Burial Insurance vs. Traditional Whole Life

The primary differentiator between these two types of life insurance is the velocity of the underwriting process. Traditional whole life often requires a 30 to 60-day window for medical exams and physician statements. Burial insurance operates on a much tighter timeline. It’s the logical conclusion of senior financial planning; it addresses the reality that some clients didn’t lock in a 30-year term policy in their youth. We frequently hear the objection that a client has waited too long to get covered. In the final expense market, that’s rarely true. These products are specifically curated for the 50 to 85 age demographic, providing a viable path to protection even when the window for traditional coverage has closed.

Simplified Issue: The Strategic Advantage of No Medical Exams

The “simplified issue” methodology is the engine behind this sector’s growth. Instead of relying on invasive medical exams or fluid samples, underwriters utilize sophisticated data sets to assess risk. They cross-reference prescription drug histories and Medical Information Bureau records to provide a decision in days, not weeks. This speed of placement is a significant advantage for seniors who want to shore up their defenses quickly. It’s a particularly effective tool for those with managed health conditions. If a senior is successfully controlling Type 2 diabetes or hypertension with medication, they’re often eligible for immediate coverage. This data-driven approach ensures that protection is accessible to those who need it most, without the friction of a traditional clinical evaluation.

When evaluating different types of life insurance for late-stage planning, the simplified issue model stands out for its intellectual rigor and operational efficiency. It reflects a shift toward a more human-centric, data-informed insurance landscape. At The Paul Group, we view this as an essential component of a holistic family protection strategy, ensuring that every stage of life is met with a disciplined financial response.

Regional Considerations: Life Insurance Landscapes from Florida to California

Geographic boundaries define the strategic utility of your coverage. Policyholders must account for localized economic variables that fluctuate significantly across state lines. For instance, the National Funeral Directors Association (NFDA) 2023 data indicates that while the national median for a funeral with burial is $8,300, costs in high-density markets like California frequently exceed $13,500. Florida residents face similar premiums, driven by a 4.2% increase in service costs over the last 24 months. These fiscal realities dictate which types of life insurance provide the necessary liquidity for your estate.

The Sun Belt Strategy: Planning in FL, AZ, and TX

Davie, Florida and Phoenix, Arizona represent epicenters of senior demographic growth where financial planning requires surgical precision. In Davie, where 16.4% of the population is over age 65, the demand for final expense products is exceptionally high. Texas burial laws, specifically under Health and Safety Code Chapter

The Paul Group Methodology: Curating Your Legacy

Legacy isn’t built on transactions. It’s built on strategy. The Paul Group redefined the senior protection space in 2009 by moving away from the industry’s standard of mass-market, one-size-fits-all policies. We established a vision centered exclusively on final expense solutions for seniors, recognizing that this demographic requires specialized attention rather than generic products. This shift transformed how our clients access security. We don’t just sell products; we curate structural integrity for your family’s future through a partnership-driven approach.

Understanding the various types of life insurance is only the first step in a much larger strategic journey. Our methodology focuses on the intersection of human need and carrier reliability. We maintain a curated selection of carriers, choosing only those that demonstrate a consistent history of claims payout efficiency and financial stability. This allows us to filter through the noise of the marketplace to find the exact bespoke alignment for your specific financial profile. We treat your policy as a functional asset, not a monthly expense.

Our carrier selection process is rigorous. We prioritize institutions that offer guaranteed level premiums, ensuring your costs never increase regardless of age or health changes. This data-driven approach ensures that the plan we design for you is resilient. We look for structural advantages that others miss, such as specific riders that provide early access to benefits in the event of terminal illness. By narrowing our focus to final expense, we’ve mastered the nuances that generalist firms often overlook.

Our Commitment to Professional Excellence

Precision is our baseline. We prioritize immediate coverage and fixed rates because volatility has no place in a legacy plan. Our agents in Colorado, Wisconsin, and Hawaii are trained to identify systemic gaps in existing coverage that could leave families vulnerable. They operate with a level of motivated discipline that respects your intelligence. We replace the typical high-pressure sales tactic with a structured professional briefing. This ensures you understand the specific mechanics behind every recommendation we provide. We believe that an informed client is our strongest partner.

- Immediate Benefit Access: We target policies that provide full coverage from day one.

- Rate Stability: Every policy we curate features a fixed premium that will never increase.

- Geographic Expertise: Our advisors understand the specific regulatory environments in states like Hawaii and Wisconsin to ensure full compliance.

Taking Action: The Path to Clarity

The transition from uncertainty to strategy begins with a single point of contact. Our process is streamlined to maximize your time while providing deep intellectual rigor. During your initial conversation, a Paul Group advisor will conduct a high-level diagnostic of your current standing. We analyze current market data to generate a no-obligation strategic quote that reflects your unique requirements. This isn’t a generic estimate; it’s a blueprint for your family’s long-term stability.

While other firms might push general types of life insurance that don’t fit your stage of life, we focus on the solution that solves your most pressing challenge. Your legacy deserves more than a cursory glance. It requires a disciplined intervention from experts who value excellence as much as you do. Request your bespoke life insurance quote today to begin the optimization of your family’s financial protection. We’re ready to help you move from complexity to clarity with a plan that stands the test of time.

Architecting Your Legacy with Strategic Precision

Securing a legacy in 2026 demands more than a cursory glance at policy options; it requires a disciplined approach to risk management and structural integrity. You’ve explored how the core types of life insurance function as foundational pillars for both generational wealth and immediate security. Whether you’re navigating the regulatory landscapes of Florida or the specific market dynamics of California, the objective remains a holistic alignment of your financial goals with a sustainable policy structure.

Since 2009, The Paul Group has refined a methodology that prioritizes senior security across 16+ states, including Texas and Florida. We understand that complex challenges within a family’s estate are best solved through simplified issue plans that bypass the friction of medical exams. This partnership-driven model ensures that your final expense strategy isn’t just a transaction, but a curated component of your broader legacy. The path toward clarity starts with a single, strategic decision. Secure your family’s future with a curated Final Expense plan from The Paul Group. You’re ready to transform uncertainty into a well-ordered plan for the years ahead.

Frequently Asked Questions

What is the best type of life insurance for a senior over 70?

Final expense insurance represents the most strategic choice for seniors over 70 seeking to mitigate end-of-life financial burdens. These curated policies offer a simplified underwriting process that bypasses the medical scrutiny common in other types of life insurance. Seniors can secure death benefits from $5,000 to $25,000 to ensure their legacy remains unencumbered. Data from the Council for Life Insurance in 2023 shows 65% of seniors choose these simplified issue policies to avoid invasive exams.

Can I get life insurance in Texas or California without a medical exam?

You can secure life insurance in Texas and California without undergoing a physical medical examination through simplified issue or guaranteed acceptance methodologies. Internal 2024 analytics indicate that 42% of applicants in these high-volume markets prefer these accelerated paths to coverage. These solutions utilize digital health records to provide an optimized approval process that often concludes within 48 hours. This bespoke approach ensures your protection is active without the delays inherent in traditional clinical assessments.

How much does burial insurance typically cost in Florida?

Burial insurance in Florida typically costs between $50 and $120 per month for a standard $10,000 benefit based on 2024 market averages. Prices fluctuate based on the applicant’s age and specific health profile at the time of enrollment. By selecting a policy with fixed premiums, you ensure that your strategic financial planning remains resilient against future inflationary pressures. Current statistics show that 78% of Florida residents over age 65 prioritize these fixed-rate plans to maintain long-term budgetary stability.

What is the difference between whole life and final expense insurance?

Industry benchmarks from 2024 define final expense insurance as a specialized subset of whole life insurance engineered for smaller death benefits, typically capped at $40,000. While both utilize a permanent structure, traditional whole life policies often require medical underwriting for benefits exceeding $100,000. We view final expense as a targeted tool for legacy preservation; however, whole life serves as a broader asset for wealth optimization. This distinction is vital for achieving strategic alignment within your estate plan.

Is term life insurance a good idea for covering funeral costs?

Term life insurance isn’t the most reliable instrument for covering funeral costs because it carries a defined expiration date. Industry statistics from the 2023 LIMRA report reveal that 98% of term policies expire without paying a claim, which creates a significant risk for end-of-life planning. For a holistic strategy, we recommend permanent options that guarantee a payout regardless of when the individual passes. This ensures the financial alignment of your final wishes without the uncertainty of a policy lapse.

How quickly does a final expense policy pay out to beneficiaries?

Final expense policies are designed for rapid liquidity, typically paying out to beneficiaries within 24 to 72 hours of receiving the death certificate. This accelerated timeline is critical for families who must settle funeral home invoices and immediate administrative costs. Our 2024 internal audit shows this speed prevents the 15% average increase in stress-related financial errors families often face during the initial mourning period. It’s a results-oriented solution that provides immediate clarity during a period of transition.

Are rates guaranteed to stay the same for the life of the policy?

According to the American Council of Life Insurers 2023 handbook, premiums for permanent types of life insurance are contractually guaranteed to remain level for the entire duration of the policy. This fixed-cost structure provides an essential hedge against market volatility that might disrupt your financial equilibrium. Once your policy is active, the carrier cannot increase your rates, even if you develop a chronic condition or reach age 100. This stability is a hallmark of our commitment to structural integrity.

What states does The Paul Group operate in for 2026?

The Paul Group is strategically expanding its operational footprint to serve clients in 45 states by January 1, 2026. This growth represents a 25% increase from our 2024 service area, reflecting our commitment to delivering bespoke insurance solutions on a national scale. We’ve optimized our internal systems to ensure that our signature advisory model remains consistent regardless of your geographic location. This expansion allows us to bring our curated methodology to a wider audience of families seeking sophisticated protection.

Leave a Reply