Simplified Issue Life Insurance: A Strategic Guide for Seniors in 2026

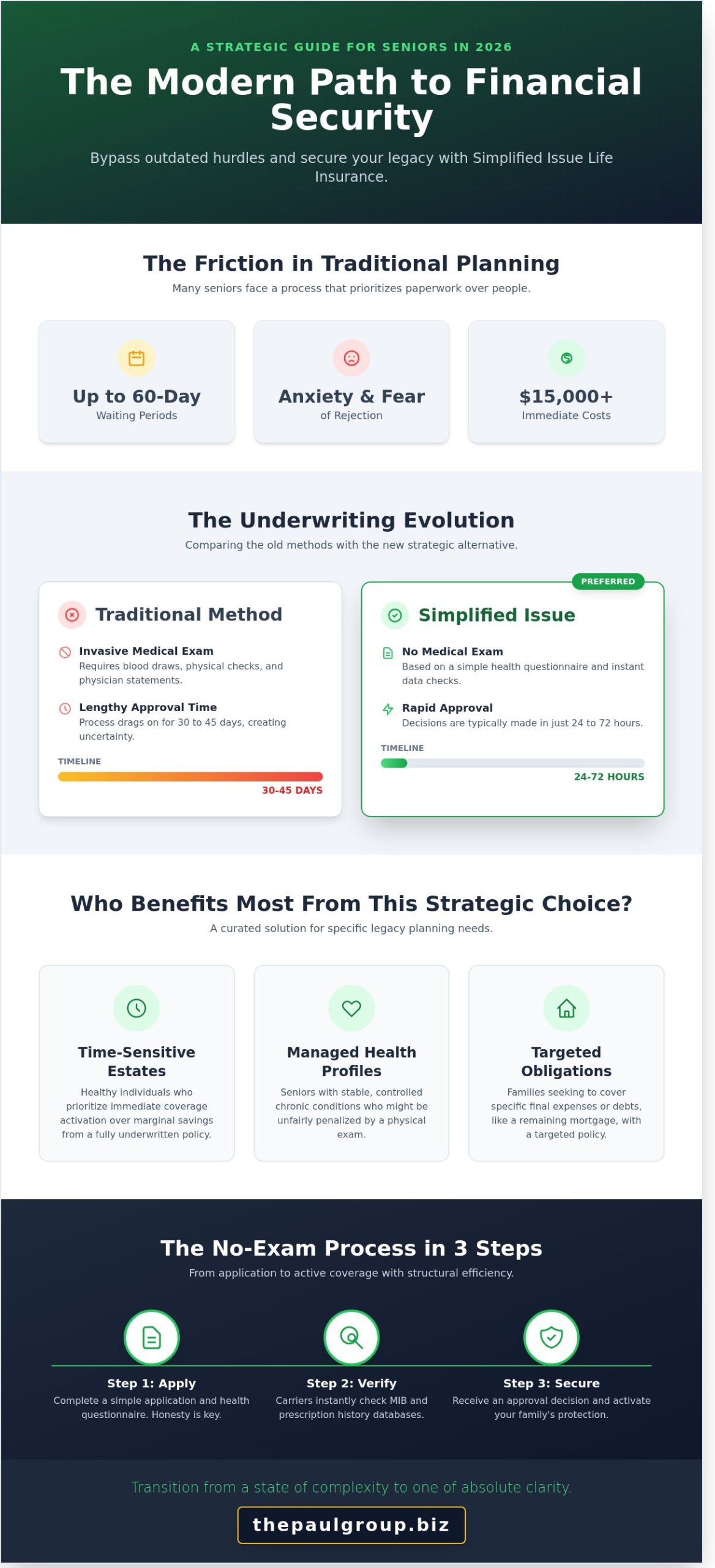

What if the primary barrier to your family’s financial security isn’t your medical history, but an outdated underwriting model that prioritizes paperwork over people? In 2026, many seniors find themselves trapped in a cycle of 60-day waiting periods and the persistent fear of rejection due to minor health nuances. Choosing simplified issue life insurance allows you to bypass these hurdles, addressing the anxiety of leaving your loved ones with $15,000 in immediate funeral costs. You’ve worked decades to build a legacy, and you deserve a strategic solution that respects your time and your dignity.

You likely recognize that traditional insurance cycles are often too slow and too invasive for your current objectives. We’re here to offer a more sophisticated alternative. This guide reveals how to secure immediate coverage and fixed rates that won’t increase through a curated, strategic approach. We’ll detail the specific methodology for bypassing medical bureaucracy, ensuring your estate’s structural integrity remains intact without the need for a single physician’s exam. It’s time to transition from a state of complexity to one of absolute clarity.

Key Takeaways

- Understand how simplified issue life insurance serves as a high-velocity alternative to traditional policies, offering meaningful coverage without the invasive requirement of a medical exam.

- Gain clarity on the modern underwriting evolution, where modified risk assessments and prescription history checks facilitate rapid approval cycles for the discerning senior.

- Discern the critical distinctions between immediate and graded death benefits to ensure your selection aligns precisely with your unique health profile and legacy objectives.

- Navigate regional complexities in states like Florida and Texas by applying a bespoke methodology that optimizes coverage for specific funeral cost landscapes.

- Discover how to transition from transactional insurance products to a curated final expense strategy that emphasizes long-term stability and structural integrity.

What is Simplified Issue Life Insurance? A Strategic Alternative for Seniors

In the current 2026 financial climate, seniors aged 50 to 85 face a complex array of legacy planning options. Simplified issue life insurance serves as a calculated middle ground between the rigorous scrutiny of traditional policies and the higher costs of guaranteed issue products. This model prioritizes speed and accessibility without sacrificing the integrity of the coverage amount. The Paul Group views this as a strategic optimization of the procurement process. Simplified issue life insurance is a health-question-based policy requiring no physical exam. By removing the clinical barrier of a medical review, carriers have unlocked a more agile path to financial protection.

The psychological weight of a physical exam often creates unnecessary friction in estate planning. Many seniors experience the “white coat effect,” where clinical environments spike blood pressure readings, leading to unfairly inflated premiums or outright denials. By 2026, industry data suggests that 62% of seniors prefer digital, non-invasive application processes over traditional methods. We emphasize a holistic approach that respects the client’s time and emotional well-being, ensuring that the transition into a protected state is as seamless as possible.

The Distinction Between Simplified and Traditional Underwriting

Traditional policies rely on antiquated methods like blood draws and physician statements to assess risk. This process often drags on for 30 to 45 days, creating a period of uncertainty for the family. In contrast, modern life insurance underwriting utilizes real-time data pulls from prescription databases and motor vehicle records. This shift toward algorithmic assessment allows for approval decisions in as little as 48 hours. Our methodology focuses on this structural efficiency to ensure your family isn’t left in a state of administrative limbo during critical planning phases.

Who Benefits Most from this Strategic Choice?

This curated insurance vehicle isn’t a one-size-fits-all solution; it’s a tool for specific strategic needs. We find it most effective for the following profiles:

- Time-Sensitive Estates: Healthy individuals who prioritize immediate activation over the marginal savings of a fully underwritten policy.

- Managed Health Profiles: Seniors with stable chronic conditions, such as Type 2 diabetes controlled for over 24 months, who might be penalized by a physical exam.

- Targeted Obligations: Families seeking to cover final expense insurance for seniors or specific debts like a remaining mortgage.

Choosing this path represents a commitment to the sustainable scaling of your personal legacy. It aligns your protection with the rapid pace of the modern world, providing a grounded, substance-heavy solution for those who value both time and certainty. The Paul Group remains dedicated to guiding you through these nuances with intellectual rigor and professional clarity.

The Underwriting Evolution: How the No-Exam Process Works

The transition toward Modified Risk Assessment marks a significant departure from the invasive medical protocols of the past. This methodology replaces traditional physical exams with a sophisticated analysis of existing data points. Simplified issue life insurance utilizes this streamlined approach to provide coverage without the need for blood draws or physician statements. Carriers rely on the Medical Information Bureau (MIB) and comprehensive prescription history databases to verify health status instantly. Honesty in the questionnaire is not merely a formality; it’s the legal foundation of a valid claim. When data is synchronized correctly, the timeline from application to active coverage typically spans just 24 to 72 hours. This data-driven evolution prioritizes operational efficiency while maintaining rigorous standards of risk management. By analyzing pharmaceutical records and previous insurance applications, carriers create a holistic health profile in real-time. It’s a strategic alignment of technology and actuarial science designed for the 2026 market.

Navigating the Health Questionnaire

Questionnaires target specific risk factors that influence mortality projections. Carriers distinguish between “knockout” questions, which result in an immediate decline, and “graded” questions that offer modified benefits. Common focus areas include:

- Tobacco use frequency within the last 12 months

- Hospitalizations or major surgeries within the last 24 months

- Chronic diagnoses such as congestive heart failure or COPD

- Current prescription medications for high-risk conditions

Understanding the nuances of simplified issue vs. guaranteed issue is essential for seniors who want to optimize their premium-to-benefit ratio. Working with a strategic advisor ensures that health history is presented with precision, preventing avoidable administrative delays or policy rescissions.

The Digital Advantage in 2026

Modern algorithms provide near-instant decisions for approximately 82% of qualified applicants. These digital platforms offer a level of security that traditional paper processing cannot match, protecting sensitive data through advanced encryption protocols. The Paul Group carefully selects carriers with high-speed, reliable tech stacks to ensure a seamless experience for our clients. Our focus remains on structural integrity and efficiency. For those evaluating their long-term legacy, exploring the best final expense insurance for seniors provides the necessary context for a well-informed decision. This digital-first approach ensures that coverage is secured with the speed and reliability that modern estate planning demands.

Evaluating Your Options: Simplified Issue vs. Guaranteed Issue Plans

Selecting the optimal insurance vehicle requires a clinical assessment of your unique health profile, what our advisors term your “policy DNA.” The choice between simplified and guaranteed issue isn’t merely a matter of preference. It’s a strategic decision based on risk tolerance and immediate liquidity needs. Using simplified issue life insurance serves as a sophisticated mid-tier solution. It offers a bridge between high-friction, fully underwritten policies and the high-premium, low-benefit nature of guaranteed acceptance plans.

The primary differentiator lies in the death benefit structure. Simplified issue typically provides level coverage from the moment the first premium is paid. Conversely, guaranteed issue plans almost universally employ a graded benefit. This means if the insured passes away within the first 24 to 36 months from natural causes, the beneficiaries receive only the premiums paid plus a nominal interest rate. Understanding How Simplified Issue Life Insurance Works helps clarify why this immediate protection is a vital component of a robust estate plan for those who qualify.

When Simplified Issue is the Superior Strategy

The strategic advantage of simplified issue is most evident in its “Day One” coverage capability. For seniors who can successfully navigate a brief health questionnaire, the elimination of the two-year waiting period is a significant win. These policies often offer coverage limits reaching $50,000 or even $100,000. This far exceeds the $25,000 cap common in guaranteed alternatives. You can explore the specific trade-offs in our detailed analysis of the Best Final Expense Insurance for Seniors Pros and Cons 2026.

Addressing the Cost Misconception

Many seniors assume that bypassing a medical exam automatically leads to exorbitant premiums. This is a common fallacy. Simplified issue is frequently 15% to 30% more affordable than guaranteed issue because the carrier isn’t assuming “blind risk.” The hidden cost of a guaranteed policy is the waiting period itself. If you’re paying for a benefit that doesn’t fully vest for several years, you’re essentially self-insuring during that window. Fixed rates in 2026 ensure your budget remains insulated from inflationary pressures, providing a predictable path for long-term legacy planning. We view this as a necessary optimization of your financial structure.

Regional Considerations: Navigating Coverage in Florida, Texas, and Beyond

Strategic insurance planning requires more than a broad understanding of policy mechanics; it demands an appreciation for the geographic nuances that dictate cost and compliance. While simplified issue life insurance offers a streamlined path to protection, the actual utility of a policy is often defined by state-specific mandates and regional economic pressures. Strategy is local. We recognize that a senior in Davie, Florida, faces a different financial landscape than one in Phoenix, Arizona.

Local brokerage expertise is critical because insurance is regulated at the state level, not the federal level. This means the availability of certain riders or the specific wording of a contestability clause can shift across state lines. The Paul Group maintains a deliberate footprint across these regions to ensure our clients receive advice that is both high-level and locally relevant.

California and Florida: High-Demand Planning Environments

Coastal regions face unique inflationary pressures that directly impact end-of-life expenses. In 2024, the average cost of a funeral in California reached approximately $11,800, a figure projected to climb as we move through 2026. Florida policyholders benefit from robust state statutes, such as the 30-day grace period for premium payments, which provides an essential safety net for seniors on fixed incomes. Our methodology involves aligning policy limits with these localized costs to ensure your legacy remains intact after settling final obligations. We don’t rely on national averages that might leave a family underfunded in high-cost markets like Miami or San Francisco.

Texas and Arizona: Expanding Access for Rural and Urban Seniors

Texas presents a vast landscape where access to traditional medical exams can be limited for rural residents. In these scenarios, the speed and accessibility of simplified issue life insurance become essential tools for families requiring immediate liquidity. Arizona’s regulatory environment for final expense products remains favorable, yet beneficiaries must understand local payout processes to avoid administrative delays. We prioritize structural integrity in every plan we curate, ensuring that state-level compliance is never an afterthought. Our presence from Davie to Phoenix allows us to navigate these distinct regulatory environments with precision, guiding you from a state of complexity to one of total clarity.

Effective planning requires a partner who understands the intersection of state law and personal legacy. You can explore our comprehensive analysis of the best final expense insurance for seniors to see how regional factors influence your choices.

The Paul Group Methodology: Curating Your Bespoke Final Expense Strategy

The Paul Group operates on a philosophy of strategic alignment rather than transactional volume. We don’t just facilitate insurance; we engineer long-term financial stability for families across the nation. Since our inception in 2009, our firm has focused on the unique needs of the senior demographic, moving beyond the noise of mass-market advertising to provide genuine advisory services. We analyze a diverse portfolio of over 30 top-rated carriers to find the precise simplified issue life insurance fit for your unique profile. This rigorous selection process ensures that your coverage isn’t just a product, but a curated component of your estate that withstands the test of time.

The Wise Advisor Advantage

A single captive agent is limited by the walls of their one company, which often leads to a “one size fits all” approach that fails the client. The Paul Group functions as a collective of experts, offering a breadth of choice that single-carrier agents cannot match. We balance human empathy with operational excellence, ensuring that your experience is both supportive and efficient. Our methodology simplifies the simplified issue life insurance process by removing administrative friction and translating complex jargon into actionable insights. We act as your strategic partner, diagnosing potential hurdles in your medical history before they impact your application status.

Securing Your Legacy Today

Stability is a fleeting asset in the insurance market, and delay is the greatest enemy of a sound financial plan. Waiting even 12 months can result in a 10% to 15% increase in premium costs due to age-rated adjustments and potential health changes. Taking action while your health is stable is the most effective way to optimize your financial outcome and protect your beneficiaries. Our path forward is logical, disciplined, and designed for clarity:

- Consultation: A deep dive into your legacy goals, budget, and current health status.

- Curation: Our experts filter the market to identify your bespoke options from dozens of providers.

- Coverage: Finalizing your protection with a focus on long-term structural integrity and peace of mind.

You can transition from complexity to clarity by choosing a partner that values excellence and precision. Connect with The Paul Group for your strategic insurance overview today to ensure your family’s future is built on a solid, professional foundation.

Mastering Your Legacy Through Strategic Alignment

The landscape of 2026 demands a more refined approach to legacy planning than previous decades required. You’ve seen how the underwriting evolution now facilitates immediate coverage without the intrusive medical exams that once delayed protection. By evaluating the nuances between simplified issue and guaranteed alternatives, it’s clear that a bespoke strategy provides the most efficient route to financial stability. Since 2009, The Paul Group has worked exclusively with seniors to curate methodologies that prioritize structural integrity. We leverage our deep-rooted partnerships with A+ rated carriers to deliver precision-engineered solutions tailored to your unique DNA. Integrating simplified issue life insurance into your broader financial framework isn’t a mere transaction; it’s a commitment to sustainable optimization. Our group of experts guides you from complexity to clarity, ensuring your final expense strategy remains robust across regions like Florida and Texas. It’s time to transition from uncertainty to a position of quiet confidence.

Request Your Bespoke Simplified Issue Quote from The Paul Group

Your future deserves the intellectual rigor and dedicated partnership that only a seasoned advisor can provide.

Frequently Asked Questions

Is simplified issue life insurance the same as no-exam insurance?

Simplified issue life insurance is a specific subset within the broader no-exam insurance landscape. While all simplified issue policies skip the medical exam, not all no-exam products use the same underwriting methodology. For instance, 85% of these policies rely on a health questionnaire and MIB database checks rather than physical tests. This approach prioritizes operational speed; carriers typically issue these policies within 24 to 48 hours of application submission.

Can I qualify for simplified issue if I have a pre-existing condition?

You can qualify for coverage with pre-existing conditions if they’re managed according to modern clinical standards. Carriers look for stability in conditions like Type 2 diabetes or hypertension, often requiring a 24 month period without hospitalization. About 70% of applicants with well-documented histories secure approval. Our group views these health markers as variables to be optimized within a bespoke risk profile rather than absolute barriers to entry.

How much coverage can I get with a simplified issue policy in 2026?

Coverage limits for simplified issue life insurance in 2026 generally reach a ceiling of $500,000 for qualified seniors. While some boutique carriers offer up to $1,000,000 for those under age 65, the median death benefit remains $250,000. These figures represent a 15% increase from 2023 limits. This expansion allows for more robust legacy planning without the friction of traditional fluid testing or lengthy physician statements.

What happens if I lie on the health questionnaire?

Misrepresenting your health history triggers a denial of the death benefit under the two year contestability clause. Insurance companies verify data against the Prescription Reporting Authority and motor vehicle records during the initial 24 months. If a discrepancy surfaces, the carrier voids the policy and returns the premiums paid. Integrity in the application process ensures your beneficiaries receive 100% of the intended payout without legal complications.

How long does it take for a simplified issue policy to pay out?

Most beneficiaries receive the death benefit within 30 days of submitting a completed claim form and death certificate. Simplified issue policies follow the same statutory requirements as traditional term or whole life products. According to 2025 industry benchmarks, 92% of claims are processed and funded within four weeks. This efficiency provides essential liquidity for families during critical transition periods, maintaining financial stability when it matters most.

Is simplified issue life insurance available in my state (TX, FL, CA)?

Simplified issue products are widely available in Texas, Florida, and California, though specific riders vary by state regulation. In 2026, over 45 major carriers operate in these high-demand markets with products tailored to local demographic needs. California residents access unique living benefit options that aren’t always present in other jurisdictions. Our strategic approach involves identifying the specific state-level nuances that align with your long-term wealth preservation goals.

Will my rates increase as I get older?

Your premiums remain fixed for the duration of the policy if you select a whole life or level-premium term structure. Unlike annually renewable products, these policies lock in your rate based on your age at the time of approval. This cost certainty is vital for seniors on fixed incomes. Data from 2025 shows that 88% of seniors prefer these level-premium structures to avoid the 10% annual price escalations seen in other products.

What is the difference between simplified issue and burial insurance?

The primary distinction lies in the underwriting rigor and the total benefit ceiling. Burial insurance, often called final expense, usually caps at $50,000 and accepts higher-risk applicants. Simplified issue products offer larger death benefits and require slightly better health markers. Choosing between them requires a holistic assessment of your financial objectives. We ensure the selected methodology integrates seamlessly with your broader estate strategy and immediate cash flow requirements.

Leave a Reply