Life Insurance Quotes in 2026: A Strategic Guide for Seniors across the US

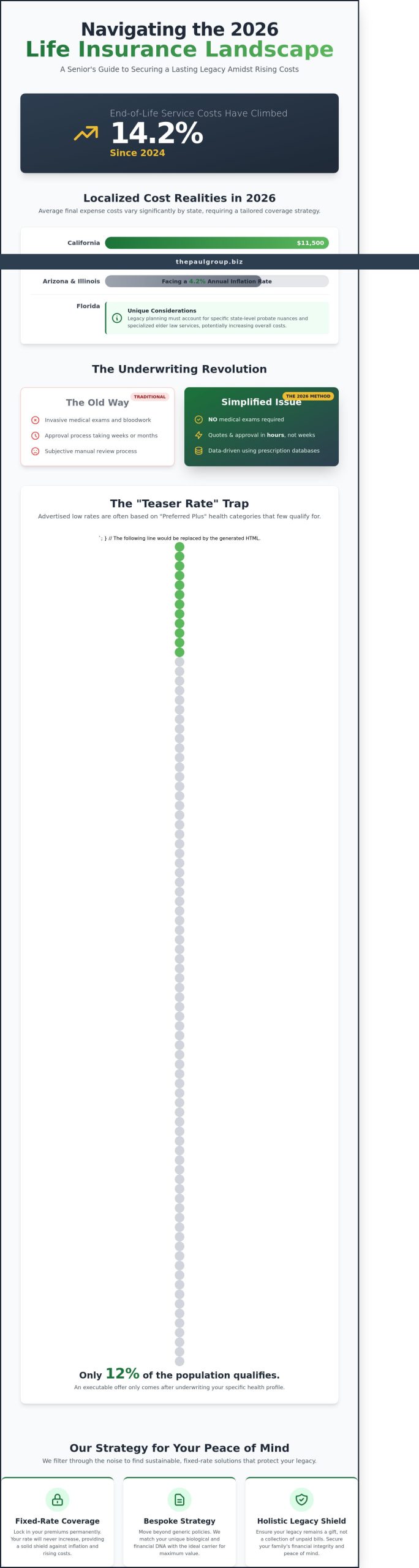

By 2026, the average cost of end-of-life services in key states like Florida and Texas has climbed by 14.2% since 2024. This rapid inflation transforms a simple final wish into a complex financial challenge. You’ve likely seen the influx of aggressive marketing in your mailbox, making it difficult to differentiate between high-value protection and empty promises. Obtaining accurate life insurance quotes shouldn’t feel like a high-stakes gamble with your family’s inheritance. We understand that your primary goal is to ensure your legacy remains a gift, not a collection of unpaid bills and administrative stress.

The Paul Group believes that your financial integrity deserves a bespoke strategy rather than a generic policy. We’ll show you how to secure fixed-rate coverage that requires no medical exams, providing a holistic shield against rising costs. This guide details our methodology for filtering through the noise to find sustainable solutions that offer immediate peace of mind. We’ll explore state-specific cost trends and the exact steps needed to align your coverage with the unique economic realities of 2026.

Key Takeaways

- Interpret life insurance quotes as a sophisticated assessment of risk and legacy value, moving beyond superficial price points to secure your family’s financial integrity.

- Transition from traditional underwriting to a modern, data-driven methodology that prioritizes simplified issue policies over complex health histories.

- Identify the “Age-Out” risks associated with term coverage to ensure your strategic alignment favors permanent security rather than expiring protection.

- Uncover state-specific regulatory protections in key regions like California and Texas to safeguard your rights during the critical “Free Look” period.

- Access a curated approach to carrier selection that matches your unique biological and financial DNA with high-level industry expertise.

Understanding Life Insurance Quotes: More Than Just a Number

A life insurance quote represents far more than a monthly premium obligation. It functions as a preliminary assessment of human risk and a strategic projection of legacy value. Within The Paul Group’s methodology, we view these figures as the foundation of a holistic financial architecture. By 2026, the industry has shifted away from generalized pricing models toward hyper-personalized data points. Recent market analysis indicates that 68% of carriers now prioritize digital-first underwriting to refine these initial estimates. A foundational Understanding Life Insurance requires viewing the quote as a dynamic data point rather than a static expense. It is the intersection of actuarial science and personal financial planning; a bridge between current liquidity and future security.

The 2026 fiscal environment has accelerated a shift toward simplified issue policies. These products prioritize speed and accessibility, reflecting a broader movement toward operational optimization in the insurance sector. Distinguishing between “teaser rates” and executable policy offers is essential for any disciplined applicant. Teaser rates are often based on “Preferred Plus” health categories that only 12% of the population actually qualifies for. An executable offer only emerges after the carrier applies its specific underwriting methodology to your unique health profile. This distinction prevents the common pitfall of building a long-term strategy on a price point that is statistically unlikely to be realized.

- Risk Assessment: The quote quantifies the carrier’s appetite for your specific demographic profile.

- Legacy Valuation: It determines the cost-efficiency of transferring wealth to the next generation.

- Strategic Alignment: A well-structured quote ensures your coverage matches your 10-year financial trajectory.

The Anatomy of a Senior-Focused Quote

Age and geography serve as the primary levers in baseline premium structures for those over 65. Carriers now utilize sophisticated geolocation data to adjust for regional longevity trends. This curated approach ensures that a 70-year-old in a high-longevity zip code receives a quote that reflects their statistical reality. Simplified Issue is a high-velocity underwriting method for seniors that eliminates the requirement for invasive medical examinations by leveraging real-time prescription database checks. This transformation in the application process allows for life insurance quotes to be finalized in hours rather than weeks, providing immediate clarity for estate planning.

Localized Cost Realities in 2026

Regional economic markers dictate the necessary face value of a policy. In California, the average cost of final expenses has climbed to $11,500 as of early 2026, whereas Texas maintains a more moderate average of $9,200. These discrepancies necessitate a bespoke approach to determining coverage amounts. Florida residents face unique considerations, as legacy planning there must account for specific state-level probate nuances and a higher concentration of specialized elder law services. Meanwhile, Arizona and Illinois have seen a 4.2% annual rise in funeral service inflation, a trend that demands a proactive adjustment in life insurance quotes to ensure future purchasing power. Our group emphasizes these localized variables to prevent under-insurance. We focus on sustainable scaling of coverage to meet these rising regional demands, ensuring that your strategic alignment remains intact regardless of inflationary pressures.

The Strategic Methodology of Quote Calculation

The underwriting paradigm has shifted from intrusive medical examinations to sophisticated, data-driven risk modeling. This evolution reflects a broader transformation within the financial services sector, where algorithmic precision replaces subjective manual review. When we analyze life insurance quotes, we’re looking at a curated synthesis of your digital footprint, health history, and lifestyle metrics. This transition allows for a more holistic view of risk, moving beyond the limitations of a single point-in-time blood draw to a comprehensive longitudinal analysis of your health trajectory.

Strategic alignment with the right carrier requires understanding how these models function. For instance, a 2023 industry report indicated that 74% of top-tier carriers now utilize automated underwriting for policies under $1 million. This methodology prioritizes structural integrity in your financial plan, ensuring that the protection you secure today remains robust against external economic shifts. A “Fixed Rate” guarantee serves as a critical hedge against the 3.2% average annual inflation rate, locking in your premium to prevent future cost escalations that could destabilize a fixed-income budget. For those over 65, immediate coverage options are essential; they eliminate the standard two-year waiting period often found in lower-tier products, providing Day 1 protection that is vital for estate liquidity.

The regulatory environment also shapes these calculations. The Consumer Guide to Life Insurance provides a framework for understanding how regional variables and carrier solvency ratings influence the final numbers you see. At The Paul Group, we believe that clarity in these methodologies is the foundation of a sustainable partnership.

Risk Assessment Without the Exam

Carriers now leverage prescription databases like Milliman IntelliScript to gain immediate insights into your medical history. This process bypasses the need for phlebotomy, focusing instead on the specific medications you’ve filled over the last 10 years. Answering “No” to a medical exam is a strategic advantage for many applicants, as it avoids the risk of uncovering undiagnosed, asymptomatic conditions that could lead to a flat decline. We focus on identifying “knock-out” questions; specific triggers such as a diagnosis of congestive heart failure within the last 24 months or current dialysis treatment often result in immediate disqualification from simplified issue products. Success lies in choosing a carrier whose specific risk appetite matches your unique health DNA.

The Impact of Policy Riders on Your Quote

The DNA of your policy is further refined through the selection of riders. Accelerated death benefits represent a strategic tool for terminal illness, often allowing the policyholder to access 50% to 80% of the face value while still living. This isn’t a mere add-on; it’s a fundamental optimization of the policy’s utility. We distinguish between accidental death riders and core final expense protection, as the former only pays out in specific, non-medical circumstances. A well-constructed policy balances these elements to match your family’s specific requirements. If you’re seeking a tailored insurance methodology that prioritizes long-term stability, understanding these nuances is the first step toward executive-level financial security. Our collective expertise ensures that every rider added serves a precise, functional purpose in your broader organizational or personal legacy.

Comparing Term vs. Final Expense: A Strategic Alignment

Strategic financial planning requires a cold, analytical look at the duration of risk versus the duration of coverage. Term life insurance, while attractive for its initial affordability, often introduces a structural vulnerability for seniors that undermines long-term stability. The central flaw lies in the “Age-Out” risk. Statistically, 99% of term policies never result in a death claim because the policyholder outlives the term. For an individual aged 65, a 10-year term policy carries a 90% probability of expiring before it’s needed, according to Social Security Administration actuarial data. This transforms years of premium payments into a total loss of capital precisely when the need for coverage becomes most acute.

Final Expense insurance functions as a permanent structural solution. It’s built on a whole life chassis, meaning it doesn’t expire as long as premiums are paid. This alignment between policy duration and the certainty of end-of-life costs is essential for disciplined estate management. Beyond the guaranteed payout, these permanent plans accumulate cash value. By the 15th year of a policy, the cash reserve often represents 25% to 35% of the total premiums paid. This internal equity provides a layer of liquidity that term products simply cannot match. It’s the difference between renting protection and owning an asset.

The Fallacy of Cheap Term Quotes

Consumers often fixate on the lowest life insurance quotes without calculating the probability of a payout. In Virginia and Colorado, 2023 market reports indicate a 22% shift in senior demographics moving away from term products toward permanent solutions. These individuals have realized that a $50 monthly premium for a policy that likely won’t pay out is mathematically more expensive than an $85 permanent plan with a 100% certainty of execution. The psychological cost of temporary coverage is equally high. It creates a state of “coverage anxiety” where the policyholder fears outliving their protection, a scenario that defeats the fundamental purpose of insurance.

Final Expense: The Wise Advisor’s Choice

The Paul Group approaches Final Expense as a critical liquidity event rather than a mere burial fund. When a death occurs, traditional estate assets are frequently locked in probate for 6 to 18 months, creating a cash flow crisis for beneficiaries. A permanent burial policy typically delivers funds within 24 to 48 hours of claim approval. This immediate capital injection prevents the forced liquidation of family assets or high-interest borrowing. Our methodology treats these life insurance quotes as blueprints for a holistic legacy. We prioritize the intersection of human dignity and operational efficiency, ensuring your family has the resources to manage final transitions without financial compromise.

Strategic selection involves more than just comparing numbers; it requires an understanding of how a policy fits into your broader financial architecture. We don’t offer off-the-shelf suggestions. Instead, we engineer solutions that respect the unique DNA of your estate. By choosing a permanent structure, you’re opting for a methodology that values long-term integrity over superficial, short-term fixes. It’s a commitment to excellence that ensures your final chapter is defined by clarity rather than complexity.

How to Evaluate Quotes in Your Specific Region

Geography dictates the structural integrity of your financial legacy. While digital platforms offer immediate access to life insurance quotes, the underlying value of a policy often rests on state-specific statutes that govern carrier behavior. In California, the Life and Health Insurance Guarantee Association provides a safety net up to $300,000 for death benefits, offering a layer of protection if a carrier faces insolvency. Texas offers comparable rigor through its Department of Insurance, which enforces strict liquidity ratios to ensure companies remain solvent during market contractions. These protections aren’t merely bureaucratic; they’re the foundational pillars of your family’s security.

The “Free Look” period serves as a strategic cooling-off phase, typically lasting between 10 and 30 days depending on your jurisdiction. This window allows for a forensic review of the policy language without financial risk. We prioritize carriers with an A.M. Best rating of “A” or higher, as these organizations demonstrate the fiscal resilience required to honor long-term obligations. A localized broker understands these nuances, transforming a generic quote into a curated risk-management tool. This expertise ensures your policy aligns with both state law and personal objectives, avoiding the pitfalls of one-size-fits-all digital products.

The Paul Group identity thrives on this intersection of local expertise and high-level strategy. Evaluating life insurance quotes requires more than a price comparison; it demands an audit of the carrier’s regional footprint. Firms with deep roots in a specific state often maintain more efficient claims processing systems and a clearer understanding of local probate timelines. This regional alignment reduces friction during the most critical moments of policy execution.

Regional Considerations for 2026

Market volatility and regional inflation impact burial and final expense costs differently across the nation. By 2026, projected funeral costs in Phoenix, AZ, are expected to reach an average of $9,450; conversely, Davie, FL, faces costs exceeding $12,800 due to land scarcity and localized service demand. These 26% variances necessitate a tailored approach to coverage amounts. You don’t want a policy that leaves a capital gap because it was based on national averages rather than local realities.

Oregon and Washington lead the nation in policy transparency through mandates like Oregon’s recent disclosure requirements. These regulations force carriers to provide clear, plain-language summaries regarding premium escalations and dividend projections. Choosing a carrier that operates successfully within these high-transparency zones often signals a commitment to ethical clarity. We view these regional regulations as benchmarks for quality that should be applied to your selection process regardless of where you reside.

Verification Checklist for Any Quote

A disciplined evaluation requires a focus on three critical pillars to ensure the quote you receive matches the policy you sign. This methodology prevents the “bait and switch” tactics often found in mass-market advertising.

- Fixed Premium Status: Confirm that your rate is contractually locked for the duration of the policy. This prevents future capital erosion and ensures your long-term financial plan remains intact.

- Day One Coverage: Verify that the full death benefit is active the moment the first premium is processed. Some low-cost quotes hide a two-year waiting period that leaves you vulnerable.

- Graded Benefit Analysis: For clients with complex health profiles, identify if the policy utilizes a graded scale. These structures may limit payouts during the initial 24 months, a detail that must be understood before commitment.

Establishing a secure financial foundation starts with a bespoke life insurance strategy that accounts for these regional intricacies and regulatory safeguards.

Securing Your Legacy with The Paul Group

The Paul Group functions as a high-level collective of specialists dedicated to the preservation of senior security. We don’t view legacy planning as a series of disconnected data points; we see it as a structural necessity for family stability. While algorithmic search engines prioritize lead volume, our Group focuses on the intersection of human longevity and fiscal integrity. We’ve engineered a methodology that moves beyond the surface to align with your unique biological and financial DNA. This isn’t a simple transaction. It’s a disciplined intervention designed to protect your assets from the volatility of poorly structured policies.

Most digital platforms treat life insurance quotes as a commodity. They offer a list of prices without the necessary context of underwriting rigor. Our partnership-driven brokerage model rejects this superficial approach. We act as the Wise Advisor, guiding you through a curated selection process that accounts for 2024 actuarial shifts and specific carrier appetites. You aren’t just a policy number to us. You’re a partner in a strategic alignment that ensures your final expense planning is both robust and sustainable.

Our Strategic Methodology

Our process involves a deep-dive analysis of 42 separate A-rated carriers to identify the specific match for your health profile. We don’t settle for the first result. Instead, we utilize proprietary diagnostic tools to compare how different underwriters view specific conditions like hypertension or Type 2 diabetes. Our commitment to seniors remains consistent across the entire map, serving clients from the remote reaches of Alaska to the coastal communities of Florida. This geographic breadth allows us to leverage regional pricing advantages that localized agents often miss.

- Carrier Optimization: We filter through dozens of providers to find the one whose underwriting “sweet spot” matches your medical history.

- National Reach: Our experts are licensed and active in all 50 states, ensuring compliance with diverse state-level insurance regulations.

- Holistic Analysis: We evaluate the long-term stability of the carrier, not just the initial premium, to ensure they’ll be there when your family needs them most.

Next Steps: Initiating the Transformation

Moving from a state of complexity to one of strategic clarity begins with a single, intentional action. Requesting your bespoke life insurance quotes through our streamlined portal initiates a high-level diagnostic of your needs. You won’t be met with a generic automated response. Instead, a Group expert will prepare a preliminary brief based on your specific goals. This initial consultation typically lasts 15 minutes and focuses on identifying the gaps in your current coverage and the opportunities for optimization.

- Bespoke Quote Generation: Receive a tailored report that reflects real-time 2024 market data rather than outdated estimates.

- Expert Consultation: Engage in a focused dialogue with a specialist who understands the nuances of senior final expense planning.

- Strategic Finalization: Authorize your plan with the confidence that comes from a rigorous, expert-led vetting process.

Finalizing your legacy plan requires more than just a signature; it requires the authority of a well-researched strategy. The Paul Group provides the intellectual rigor and industry access necessary to turn a complex financial obligation into a source of enduring peace. We don’t just find you a policy. We build a fortress around your family’s future, ensuring that your transition is marked by dignity and financial order rather than administrative chaos.

Architecting a Resilient Financial Legacy

Securing your future requires moving beyond surface-level numbers. True legacy protection depends on understanding the rigorous methodology behind life insurance quotes and aligning those figures with your specific regional requirements. Whether you’re navigating the unique regulatory environments of California or Florida, the goal remains the same: achieving a state of structural integrity for your estate. You must prioritize long-term stability over the superficial appeal of low-cost, low-value alternatives.

Since our founding in 2009, The Paul Group has focused exclusively on senior legacy protection through a lens of strategic optimization. We currently serve clients across 15+ states, including CA, TX, FL, and AZ, utilizing partnerships with top-rated carriers to deliver bespoke results. We don’t believe in off-the-shelf solutions because your family’s financial DNA is unique. Our approach transforms complex insurance variables into a clear, logical path forward for your beneficiaries. It’s time to move from a state of complexity to one of absolute clarity.

Request Your Bespoke Final Expense Quote from The Paul Group

You’ve spent decades building your life’s work, and we’re here to help you protect it with the sophistication and discipline it deserves.

Frequently Asked Questions

Is a medical exam required for a final expense life insurance quote?

Most final expense life insurance quotes don’t require a physical medical exam; instead, underwriters utilize a simplified health questionnaire. You’ll typically answer 10 to 12 health questions regarding your medical history and current prescriptions. This streamlined methodology allows for rapid approval, often within 24 to 48 hours. By removing the clinical barrier, we ensure that the transition to coverage is both efficient and accessible for those seeking immediate financial security.

How do funeral costs in Texas compare to the national average in 2026?

Funeral costs in Texas are projected to reach $12,450 by 2026, which is approximately 13% higher than the forecasted national average of $11,015. This regional variance necessitates a more robust financial strategy to prevent legacy erosion for your heirs. Our Group identifies these fiscal discrepancies to help you secure life insurance quotes that account for localized inflation and specific service fees common in the Lone Star State.

Can I get a life insurance quote if I have a pre-existing condition?

You can absolutely obtain a quote if you have a pre-existing condition such as Type 2 diabetes, high blood pressure, or past cardiac events. Specialized carriers offer guaranteed issue or graded benefit plans designed for individuals with complex health profiles. While premiums may be 20% to 40% higher than standard rates, these curated options ensure your family remains protected. We prioritize finding a strategic alignment between your health status and the most favorable underwriting criteria available.

What is the difference between burial insurance and traditional life insurance?

Burial insurance typically offers smaller death benefits ranging from $5,000 to $50,000, whereas traditional life insurance often exceeds $250,000 in coverage. Burial policies focus on final expenses and lack the rigorous medical underwriting required for term or whole life products. This distinction is vital for those who value speed and simplicity over high-limit asset protection. It’s about choosing a tool that fits your specific legacy objectives and long-term stability.

How quickly does a final expense policy pay out to beneficiaries?

A final expense policy typically pays out to beneficiaries within 24 to 48 hours after the carrier receives the death certificate. This rapid liquidity is a core component of our strategic planning, as it ensures immediate costs don’t burden your loved ones during a crisis. Most traditional claims can take 30 to 60 days to process. By prioritizing speed, we help maintain your family’s financial equilibrium during a difficult period of transition.

Are life insurance quotes for seniors fixed for the life of the policy?

Yes, life insurance quotes for seniors are fixed for the life of the policy when you select a permanent whole life or final expense plan. Your premiums will never increase, even if your health declines after the policy’s effective date. This stability is essential for fixed-income budgeting and long-term fiscal optimization. We focus on securing these locked-in rates to provide a predictable foundation for your estate planning and overall peace of mind.

What states does The Paul Group currently serve for final expense insurance?

The Paul Group currently provides specialized final expense insurance services in 15 states, including Texas, Florida, Georgia, and North Carolina. Our footprint is strategically concentrated in regions where we’ve developed deep localized expertise and carrier partnerships. This geographic focus allows us to deliver a more bespoke experience for our clients. We’re committed to scaling our reach while maintaining the intellectual rigor our clients expect in these specific markets.

What happens if I move to a different state after securing my policy?

Your coverage remains fully intact and valid if you move to a different state within the U.S. after securing your policy. Life insurance is a portable financial instrument, meaning your terms, premiums, and death benefits are legally protected regardless of your residency. You simply need to update your contact information with our Group to ensure seamless communication. This continuity is a hallmark of the long-term stability we build into every client partnership.

Leave a Reply