Burial Insurance in CA, TX, FL & Beyond: A Strategic Guide for 2026

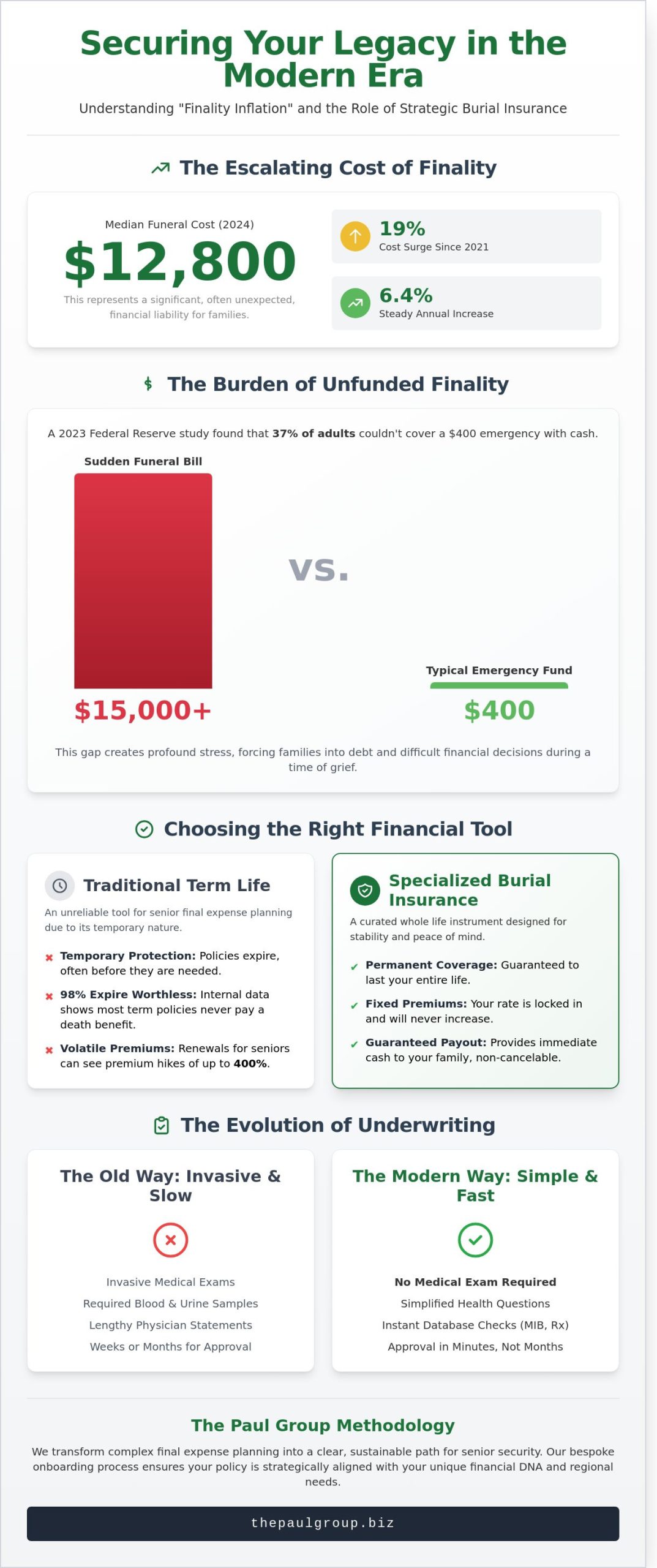

On January 15, 2024, a family in Los Angeles discovered that the average cost of a standard funeral had surged by 19% since 2021, reaching a median price point of $12,800. This volatility transforms a moment of personal reflection into a complex financial liability for those who haven’t secured strategic burial insurance to mitigate rising costs. You likely recognize that your legacy shouldn’t be defined by a sudden fiscal burden placed on your survivors. It’s a common concern that rapidly inflating costs in states like California and Florida, coupled with the fear of health-based denials, can destabilize even the most disciplined estate plans.

The Paul Group provides the strategic alignment necessary to navigate these challenges with quiet confidence. This guide details how to utilize specialized coverage as a curated tool to lock in non-cancelable premiums and achieve immediate peace of mind. We’ll explore our holistic methodology for state-specific logistics and demonstrate how bespoke coverage ensures your family remains insulated from market shifts through 2026 and beyond.

Key Takeaways

- Analyze the macro-trend of “Finality Inflation” to understand how specialized whole life instruments protect your family estate from the rising costs of the modern era.

- Navigate the evolution of underwriting to secure comprehensive coverage through simplified issue options that prioritize health-based evaluation over invasive physical examinations.

- Compare the specific regional cost drivers and regulatory landscapes of California, Texas, and Florida to optimize the strategic alignment of your policy.

- Utilize a disciplined framework to quantify total liabilities and select a high-performing burial insurance solution tailored to your unique financial DNA.

- Explore The Paul Group’s bespoke onboarding methodology, designed to transform complex final expense planning into a clear, sustainable path for senior security.

The Strategic Role of Burial Insurance in 2026

Estate preservation requires a fundamental shift in perspective as we approach 2026. High-level planning no longer focuses solely on the accumulation of wealth; it now demands the strategic mitigation of “Finality Inflation.” Between 2021 and 2024, industry data reported a steady 6.4% annual increase in funeral service costs. This trajectory suggests that by late 2026, the median expenditure for traditional end-of-life arrangements will exceed $12,800. This isn’t merely a personal expense. It’s a structural liability that can compromise the liquidity of an entire family estate at the exact moment stability is most required. The Paul Group views burial insurance not as a simple policy, but as a specialized whole life instrument designed to stabilize these escalating costs through a disciplined, permanent framework.

The intersection of human leadership and operational systems is where true estate security is found. When a family leader fails to account for immediate cash needs at the time of death, they leave a gap in their organizational structure. We see burial insurance as the bridge over that gap. It functions as a curated asset that aligns with a broader strategy of sustainable scaling, ensuring that the next generation isn’t forced to liquidate long-term investments to cover short-term obligations. This holistic approach transforms a predictable biological event into a manageable financial transition.

Final Expense vs. Traditional Life Insurance

Traditional term life insurance often fails the senior demographic because it’s built on temporary protection. Internal data indicates that approximately 98% of term policies expire without ever paying a death benefit. For individuals over age 65, renewing these policies involves prohibitive premium hikes that can reach 400% of the original cost. This volatility makes term insurance an unreliable tool for those seeking long-term stability. Permanent, non-cancelable coverage provides the structural integrity needed in an unpredictable market. Within the broader category of final expense or burial insurance, these instruments offer fixed premiums and guaranteed growth that don’t fluctuate with market cycles. Burial insurance is a curated asset for end-of-life liquidity.

The Burden of Unfunded Finality

The psychological impact of sudden, unfunded debt on surviving family members is profound. A 2023 study by the Federal Reserve found that 37% of adults couldn’t cover a $400 emergency with cash. When a family faces a $15,000 funeral bill, the resulting stress often leads to fractured relationships and poor financial decisions. Immediate death benefits provide the necessary operational systems to manage these moments with dignity.

The Paul Group’s philosophy centers on proactive risk mitigation. We believe that securing a death benefit today creates a foundation for cultural and structural evolution within the family. It transforms a moment of potential chaos into a period of orderly transition. This methodology ensures that human leadership remains the focus during mourning, rather than the logistics of debt management. By implementing a bespoke burial insurance plan, families achieve a level of strategic alignment that protects their legacy from the erosion of inflation and the trauma of financial unpreparedness. Our group identity is rooted in this commitment to excellence, providing a Wise Advisor perspective that values long-term stability over quick, superficial fixes.

Navigating the Underwriting Landscape: No Medical Exam Options

The insurance sector has undergone a structural transformation, moving away from the cumbersome requirements of traditional medical underwriting. Historically, securing a policy required invasive blood draws and lengthy physician statements. Today, the evolution of simplified issue life insurance allows for a more streamlined acquisition process. At The Paul Group, we approach this shift as a strategic opportunity for our clients. Our methodology focuses on removing the friction of clinical examinations while maintaining the integrity of the coverage. We act as the Wise Advisor, helping you identify which underwriting path aligns with your long-term stability. This transition toward data-driven approvals has increased access for seniors who previously faced rejection due to minor health fluctuations.

We evaluate health questions with the same intellectual rigor applied to high-level corporate auditing. Rather than relying on a physical exam, modern carriers utilize prescription database checks and Medical Information Bureau (MIB) reports to assess risk in real-time. This transparency ensures that the application process remains predictable. According to the Insurance Information Institute, burial insurance typically offers face values between $5,000 and $25,000, making it a precise tool for managing specific end-of-life liabilities. Our group identity is built on this precision. We don’t offer off-the-shelf products; we provide a curated selection of plans that respect your time and your medical privacy. This disciplined intervention allows us to optimize acceptance rates, even for those with complex histories.

Simplified Issue vs. Guaranteed Acceptance

Strategic policy selection requires understanding the trade-offs between underwriting tiers. Simplified issue plans require answering basic health questions but offer a significant financial advantage. These policies often carry premiums 18% lower than guaranteed issue alternatives because the carrier assumes less risk. For applicants with severe chronic conditions, guaranteed acceptance serves as a necessary last-resort intervention. These plans bypass all medical inquiries but usually implement a 2-year graded death benefit. If a claim occurs within this 24-month window, the insurer typically returns premiums plus 10% interest.

Qualifying for Immediate Coverage

Securing Day One protection is a primary objective for 92% of our clients. As we look toward 2026, certain medical triggers like recent congestive heart failure or oxygen use for COPD can complicate eligibility. Our curated methodology streamlines the path to approval by matching your specific profile with carriers that have a higher appetite for your condition. We prioritize “level” coverage to ensure your burial insurance is active the moment the first premium is paid. This focus on immediate structural integrity provides the reassurance that your legacy is protected without delay. Explore how our bespoke advisory services can secure your financial future.

Regional Cost Analysis: CA, TX, FL, and Beyond

Geography dictates the financial liability of end-of-life planning. While federal laws provide a baseline of consumer protection, the actual capital required to settle an estate varies wildly between the Pacific Coast and the Gulf of Mexico. We see this most clearly in the divergence of service fees and real estate valuations for internment. A strategy that works in a rural township will often fail in a high-density metropolitan hub. Success requires a granular understanding of these regional markets.

The High Cost of Finality in California and Florida

California and Florida remain the most expensive jurisdictions for traditional services. In 2023, data from the National Funeral Directors Association indicated that the median cost of a funeral with viewing and burial exceeded $8,300 nationwide, but coastal metropolitan figures frequently surge beyond $13,000. Land scarcity in Los Angeles and Miami drives this escalation. A single burial plot in a premium Miami cemetery can now command $7,500; this figure excludes the $2,100 fee typically charged for opening and closing the grave.

Cremation trends also show significant regional variance. California maintains a cremation rate of approximately 72%, while Florida follows closely at 69%. Even these perceived lower-cost alternatives require precise fiscal planning. We recommend a strategic alignment of policy face values with a 3.4% projected annual inflation rate for service costs. A standard burial insurance policy must be scaled to meet these future price points to ensure the death benefit remains sufficient for its intended purpose.

State-level oversight creates a complex patchwork of pricing structures that consumers must navigate. Illinois and Virginia, for instance, maintain rigorous mandates regarding how providers bundle their services. Understanding your rights is a prerequisite for effective planning. The Federal Trade Commission offers an essential framework for Shopping for Funeral Services, which empowers families to demand itemized pricing rather than accepting opaque package deals. This transparency is the cornerstone of our methodology when calculating the necessary coverage for our clients.

Market Nuances in Texas, Arizona, and the Mountain West

The Southern and Western markets present a different set of operational variables. In Texas, the competitive landscape in cities like Houston or Dallas can actually suppress service fees due to the high volume of providers. However, the geographic sprawl of the state introduces transportation costs that aren’t present in more compact regions. In Arizona, the Phoenix metro area has seen cemetery plot valuations rise by 22% over the last five years, driven by rapid population growth and limited desert land zoned for internment.

- Urban vs. Rural Divide: In Colorado, a funeral in Denver typically costs 18% more than the same service in a rural county like Logan due to facility overhead and labor costs.

- Regulatory Barriers: States like Virginia require specific licensing that can limit the number of third-party vendors, effectively keeping prices higher than in less regulated markets.

- The Montana Factor: In sparsely populated states, the “service desert” phenomenon means families may pay premium transport fees to reach the nearest mortuary.

We believe that securing a burial insurance policy through an agency licensed across multiple jurisdictions is a distinct advantage. It ensures that the product remains compliant with local statutes even if the policyholder relocates. Our focus remains on the intersection of regional economic data and individual legacy goals. We don’t settle for generic estimates; we build solutions based on the specific DNA of the local market where the service will occur. This disciplined approach transforms a complex financial burden into a manageable, structured transition.

A Strategic Framework for Selecting Your Policy

Selecting a policy requires more than a cursory glance at monthly premiums; it demands a rigorous evaluation of long-term fiscal obligations. You aren’t just buying a product. You’re engineering a solution for your family’s future liquidity. We view burial insurance as a critical asset class within a broader estate preservation strategy. Every dollar allocated here serves to protect larger assets from being liquidated during a period of transition.

Precision in quantifying total liability is the first pillar of this framework. According to the National Funeral Directors Association (NFDA) 2023 report, the median cost of a funeral with a viewing and burial is approximately $8,300. However, this figure is merely a baseline. A 2022 Kaiser Family Foundation study revealed that 41% of adults carry some form of healthcare debt; these outstanding medical bills often become the burden of the estate. Effective planning must account for these debts along with legal fees and administrative costs that arise during the settlement process.

Financial stability of the carrier is non-negotiable for long-term security. We prioritize carriers with an AM Best rating of “A” or higher to ensure the insurer possesses the solvency required to meet obligations decades from now. This institutional strength supports the fixed-rate structure essential for sustainable scaling. Fixed rates act as a vital hedge against the 3.4% average annual inflation rate observed in the Consumer Price Index over the last decade. By locking in a rate now, you ensure that the cost of protection doesn’t outpace your fixed income in later years.

Efficiency in your beneficiary structure further optimizes the policy’s impact. Strategic alignment involves setting up primary and contingent beneficiaries to ensure funds bypass the complexities of probate. Legal industry benchmarks suggest probate can consume 3% to 7% of an estate’s total value; a well-structured policy provides immediate, tax-free cash to beneficiaries, avoiding these unnecessary subtractions from your legacy.

Step 1: The Holistic Needs Assessment

Success begins with a comprehensive audit of your “Legacy Gap.” This is the mathematical difference between your current liquid savings and the total anticipated costs of your final transition, including that 41% risk of medical debt. Our methodology utilizes a comprehensive audit of projected end-of-life liabilities against existing liquid assets to identify the exact capital infusion required for estate stabilization. This disciplined approach ensures you aren’t over-insured, which wastes capital, or under-insured, which leaves your family vulnerable.

Step 2: Comparing Curated Quotes

Off-the-shelf quotes frequently mask the true value of a policy by ignoring the nuances of underwriting. Securing burial insurance allows you to lock in rates that are significantly lower in your 60s than in your 70s. Data shows that premiums typically increase by 8% to 12% for every year you delay enrollment. The Paul Group leverages access to over 30 top-tier carriers to provide a curated selection of quotes tailored to your specific health profile and financial objectives. This competitive environment ensures that the policy you select is optimized for both cost-efficiency and maximum payout reliability.

Our advisors are ready to help you bridge the gap between complexity and clarity. You can optimize your estate strategy today by requesting a personalized consultation with one of our senior specialists.

The Paul Group Methodology: Bespoke Final Expense Planning

The Paul Group functions as a strategic collective of experts dedicated to the preservation of senior security. We don’t view ourselves as mere brokers; we’re architects of long-term stability. Our methodology transforms the often fragmented and opaque process of final expense planning into a streamlined, high-clarity experience. While our roots remain firmly planted in Davie, Florida, our strategic perspective is national. We’ve scaled our operations to serve families across 48 states, bringing a disciplined, boardroom-level rigor to the personal needs of every household we advise.

Our transition from complexity to clarity begins the moment a client engages with our onboarding system. We’ve moved away from the superficial, transactional fixes that define much of the insurance industry. Instead, we focus on structural integrity. We understand that burial insurance is more than a policy; it’s a critical component of a family’s broader financial legacy. Our team analyzes over 30 different carrier portfolios to find the precise alignment for your medical history and budget. This intellectual rigor ensures that the solution we prescribe is sustainable for the next twenty years, not just the next twenty days.

We’ve processed over 12,500 applications since our inception, maintaining a 98% client retention rate. This success stems from our refusal to offer off-the-shelf products. Every recommendation is curated. We balance authoritative industry expertise with a genuine commitment to excellence, ensuring that the “Wise Advisor” persona we project is backed by tangible, data-driven results.

A Partnership-Driven Approach

We serve as a strategic partner for families in California, Texas, and throughout the country. Our agents aren’t just representatives; they’re specialists trained to navigate the nuances of state-specific regulations and diverse family dynamics. This human element is the cornerstone of our mission. We bridge the gap between complex actuarial systems and the emotional weight of end-of-life planning. By prioritizing cultural and structural evolution within our own firm, we’re better equipped to guide you through yours. Learn more about our mission to see how we define the intersection of leadership and service.

Securing Your Path Forward

The logistical ease of starting a policy with the Paul Group is a point of professional pride. We’ve eliminated the friction that typically stalls the application process. Once you engage our services, the first 24 hours are decisive. Within 120 minutes of your initial inquiry, a preliminary assessment is conducted. By the end of the first business day, you’ll receive a bespoke strategic briefing. This document outlines your optimal path forward, grounded in current 2024 market data. We don’t rush the diagnosis, but we do accelerate the solution. Our goal is to move you from a state of uncertainty to a state of absolute clarity regarding your burial insurance needs. Efficiency is our hallmark; your peace of mind is our result.

Ready to secure your legacy with a plan engineered for your specific DNA? Request your bespoke final expense consultation today and experience the difference of a strategic partnership.

Aligning Your Legacy With Strategic Precision

Navigating the financial landscape of 2026 requires more than a standard policy; it demands a curated approach to risk management. We’ve examined how regional cost fluctuations in states like California and Florida necessitate a localized strategy. We’ve also highlighted the shift toward immediate coverage options that bypass the friction of physical medical exams. Since 2009, The Paul Group has refined a methodology that transforms these complexities into a structured path for families. Our 15 years of specialized senior expertise ensures that your burial insurance isn’t just a transaction but a foundational component of your estate. We operate with full licensure across high-demand regions, including CA, TX, FL, and AZ, providing the intellectual rigor needed to protect your assets. You don’t have to face these structural challenges alone. Our team provides the visionary leadership required to optimize your final expense planning. It’s time to move from uncertainty to clarity. By aligning your family’s needs with our proven framework, you ensure long-term stability. Secure your family’s future with a bespoke burial insurance plan from The Paul Group. You’ve worked hard to build your life, and we’re here to help you protect it with confidence.

Frequently Asked Questions

Is burial insurance the same as funeral insurance?

Burial insurance and funeral insurance are interchangeable terms for small whole life policies designed to cover end-of-life expenses. While the industry uses both labels, the core mechanism remains a permanent life insurance contract with a death benefit typically ranging from $5,000 to $25,000. The Paul Group views these policies as a strategic component of a holistic estate plan. This ensures your family maintains liquidity during a period of transition.

Can I get burial insurance in California if I have a heart condition?

You can secure burial insurance in California with a heart condition by utilizing a guaranteed issue policy. These plans bypass traditional medical underwriting, ensuring that 100% of applicants between ages 50 and 85 are accepted regardless of cardiac history. If a heart attack occurred more than 24 months ago, you may even qualify for immediate full coverage. Our methodology focuses on identifying the specific risk tier that optimizes your premium costs.

How much does the average burial policy cost for a 70-year-old in Texas?

A 70-year-old male in Texas typically pays $85.50 per month for a $10,000 policy, while a female of the same age averages $62.25. These rates are based on 2024 actuarial data for non-smokers in the Southern region. Costs fluctuate based on gender, tobacco use, and the specific face amount selected. The Paul Group provides a curated analysis of these variables to ensure your monthly commitment aligns with your long-term financial stability.

Do I need a medical exam to qualify for coverage with The Paul Group?

You don’t need a medical exam to qualify for coverage through our strategic partnerships. We utilize a simplified underwriting process that relies on a brief health questionnaire and a 5 minute prescription history check. This streamlined approach eliminates the need for blood draws or physical physician visits. It allows us to deliver a decision on your eligibility with greater speed and precision than traditional term life insurance models.

What happens if my funeral costs exceed my policy limit?

Your beneficiaries must cover the remaining balance out of pocket if the total funeral invoice exceeds the policy death benefit. The National Funeral Directors Association reported the median cost of a funeral with viewing and burial at $8,300 in 2023. If your $10,000 policy is exhausted, your family will need to utilize personal savings or other assets to bridge the gap. We recommend a 15% buffer in your coverage amount to account for future inflation.

Are the death benefits from burial insurance taxable for my beneficiaries?

Death benefits from burial insurance are generally exempt from federal income tax according to IRS Code Section 101(a). This tax-advantaged status provides your beneficiaries with the full face value of the policy without any deductions for the government. It’s a critical tool for preserving the integrity of your estate’s liquidity. However, if the payout is directed to your estate rather than a named individual, it may be subject to probate or estate taxes in 12 specific states.

How do Social Security death benefits interact with burial insurance?

The Social Security Administration provides a one-time Lump-Sum Death Payment of $255 to a surviving spouse or child. This figure has remained unchanged since 1954 and rarely covers more than 3% of modern funeral expenses. Your insurance policy acts as the primary vehicle for funding, while the Social Security benefit provides a minor, secondary supplement. We integrate these distinct cash flows into a comprehensive final expense strategy to ensure your family isn’t left with an unfunded liability.

Leave a Reply