Affordable Funeral Insurance Plans

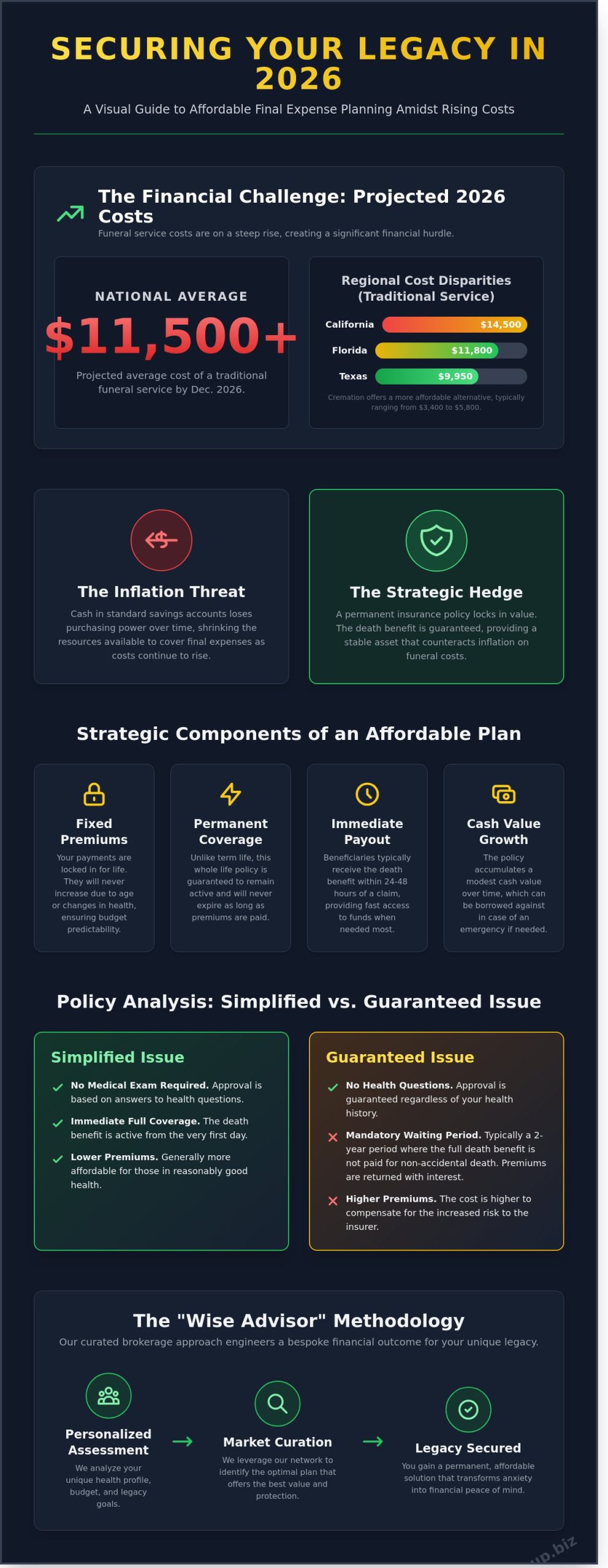

With the average cost of a funeral service projected to exceed $11,500 by December 2026, the financial burden of a final farewell has evolved from a personal matter into a complex logistical challenge. You likely recognize that a fixed income doesn’t always align with such aggressive inflationary trends. It’s a common concern that your legacy might be overshadowed by the immediate stress of unpaid bills or rising premiums. Finding affordable funeral insurance plans isn’t just about cost cutting; it’s about strategic optimization of your estate to ensure your family remains protected from sudden, high-interest debt.

At The Paul Group, we believe in a holistic approach to end-of-life planning that prioritizes both structural integrity and emotional reassurance. This guide empowers you to secure high-value final expense coverage that’s specifically tailored to your state’s unique regulations and your individual budget. We’ll examine the methodology for locking in permanent premium rates and identifying plans that offer immediate payouts, ensuring your beneficiaries receive support within 24 to 48 hours of a claim. By the end of this briefing, you’ll have a clear roadmap to transform a source of anxiety into a curated pillar of your long-term financial stability.

Key Takeaways

-

Navigate the shifting economic landscape of 2026 by understanding how permanent whole life policies provide a necessary hedge against rising national funeral costs.

-

Identify the core components of affordable funeral insurance plans, specifically how fixed premiums and permanent coverage ensure your legacy remains secure regardless of future market fluctuations.

-

Evaluate the strategic trade-offs between simplified and guaranteed issue policies to avoid the common pitfalls of mandatory waiting periods and suboptimal premium tiers.

-

Leverage state-specific regulatory insights from Arizona to Virginia to utilize "free look" periods and other mandated protections that safeguard your financial commitments.

-

Discover The Paul Group’s "Wise Advisor" methodology, which utilizes a curated brokerage approach to engineer a bespoke financial outcome tailored to your unique legacy requirements.

Table of Contents

-

The Economics of Final Expenses in 2026: Why Affordability Matters

-

Simplified Issue vs. Guaranteed Issue: A Cost-Benefit Analysis

-

State-Specific Guidance: Securing Plans from Arizona to Virginia

-

The Paul Group Methodology: Curating Affordable Legacy Solutions

The Economics of Final Expenses in 2026: Why Affordability Matters

The fiscal environment of 2026 demands a sophisticated approach to end of life planning. National funeral costs have reached a critical threshold, with the average traditional service now exceeding $12,000 when accounting for vault requirements and professional fees. This reality has transformed pre-planning from a discretionary choice into a structural financial necessity. True affordable funeral insurance plans are not merely low cost entry points; they are permanent whole life policies designed with fixed premiums and guaranteed death benefits. These instruments provide the structural integrity required to protect a senior’s estate from sudden liquidity crises.

Distinguishing between "cheap" coverage and "affordable" strategic plans is vital for long term stability. Many mass market products utilize "teaser" rates that escalate every five years, often becoming unsustainable exactly when the policyholder enters their mid 80s. The Paul Group prioritizes a methodology centered on locked in rates. By securing a level premium, you ensure that your legacy protection remains an asset rather than a growing liability. This disciplined intervention allows for sustainable scaling of your overall financial plan, providing a sense of quiet confidence that your final wishes won’t burden your survivors.

Strategic alignment with the right policy requires an understanding of the best final expense insurance for seniors. Selecting a plan involves more than a simple premium comparison; it requires a holistic view of how the death benefit will perform against future market conditions. When a policy is curated to match your specific health profile and budgetary constraints, it functions as a cornerstone of your broader financial legacy.

Projected Costs in Florida, Texas, and California

Regional economic factors create significant price disparities across the United States. In Florida, the high density of retirement communities and limited cemetery land in coastal tracts have pushed standard burial costs to approximately $11,800 in 2026. Texas offers a slightly more competitive environment due to lower logistics and land overhead, with averages hovering around $9,950. California remains the most expensive tier; intensive labor regulations and premium real estate values drive traditional services toward $14,500. Seniors opting for cremation in these regions can expect to pay between $3,400 and $5,800 depending on the complexity of the memorial service.

The Hidden Impact of Inflation on End-of-Life Planning

Inflation systematically devalues liquid assets held in traditional savings accounts, effectively shrinking the resources available to cover rising burial expenses over time.

While cash in a standard bank account loses purchasing power, a permanent insurance policy serves as a strategic hedge against these price increases. The Paul Group views these policies as a tool for optimization, ensuring that the value of the protection remains fixed even as the cost of caskets and professional services rises. This forward looking approach transforms end of life planning from a state of complexity into one of absolute clarity.

Strategic Components of Affordable Funeral Insurance Plans

Securing a legacy requires more than a simple policy purchase; it demands a calculated alignment of financial tools with personal objectives. The most effective affordable funeral insurance plans are built on a foundation of predictability. For seniors managing a fixed income, where Social Security constitutes approximately 30% of total retirement earnings for many, the fixed premium model is non-negotiable. This structure ensures that costs remain static regardless of age or health shifts, protecting the household budget from the volatility of the 2026 insurance market.

Reliability extends into the duration of the agreement. Permanent coverage provides a guarantee that the policy stays active for the entirety of the holder’s life. Unlike term products that often expire just when the risk of mortality increases, these whole-life structures offer a permanent safety net. They also accumulate a modest cash value over time. While not a primary investment vehicle, this internal equity provides a layer of liquidity that can be accessed for emergencies, offering a 2% to 4% growth rate in some high-performing contracts.

Efficiency is the final value metric. Speed matters when a loss occurs. Modern carriers now prioritize immediate payouts, often delivering funds within 24 to 48 hours of claim verification. This rapid capital injection prevents families from incurring high-interest debt to cover immediate costs while waiting for complex estate settlements to finalize.

The ‘No Medical Exam’ Advantage

Traditional underwriting is often an intrusive, weeks-long process. We prioritize simplified issue policies that bypass physical examinations entirely. By leveraging sophisticated medical databases and prescription history checks, carriers assess risk in minutes rather than months. This methodology is essential for securing affordable funeral insurance plans because it avoids the inflated costs of "guaranteed issue" plans, which can be 50% more expensive due to their lack of health screening. The Paul Group identifies specific carriers whose underwriting algorithms favor your unique health profile, ensuring you don’t pay a premium for risks you don’t carry.

Beneficiary Flexibility and Direct Funding

Strategic planning requires looking beyond the casket. While these funds are often intended for burial, they are legally unrestricted. A trusted beneficiary can use the death benefit to settle outstanding medical debts, which reached an average of $12,500 for senior households in recent years, or to manage legal fees during probate. This versatility makes the policy a comprehensive final expense tool rather than a single-use product. To better understand how these tools integrate into a broader estate plan, consult our guide on choosing senior life insurance policies. Our team at The Paul Group is ready to help you optimize your coverage levels today.

Simplified Issue vs. Guaranteed Issue: A Cost-Benefit Analysis

Choosing between simplified and guaranteed issue underwriting isn’t merely a clerical preference; it’s a high-stakes financial decision that dictates the long-term ROI of your policy. Simplified issue plans require a brief health questionnaire but skip the invasive medical exam. In contrast, guaranteed issue plans ask no health questions, providing a safety net for those with terminal diagnoses. However, this accessibility comes at a steep price. Data from 2026 indicates that guaranteed issue premiums typically range from 20% to 40% higher than simplified issue alternatives for the same death benefit. For a senior seeking affordable funeral insurance plans, qualifying for simplified underwriting is the most effective way to optimize monthly cash flow.

The primary strategic advantage of simplified issue is immediate protection. Most of these policies offer "day-one" coverage, meaning the full face value is available to beneficiaries from the moment the first premium is paid. Guaranteed issue policies almost universally include a two-year waiting period. If the policyholder passes away during this window, the carrier typically only returns the premiums paid plus a small interest buffer, often 10%. This creates a significant protection gap that can leave families vulnerable during the very period they sought to mitigate risk.

Qualifying for Preferred Rates with Health Conditions

Many seniors mistakenly default to expensive guaranteed issue plans because they manage chronic conditions. This is a tactical error. In 2026, many top-tier carriers have refined their actuarial models to be more inclusive. For instance, high blood pressure that is well-controlled with medication is frequently treated as a standard or even preferred risk. Similarly, seniors with Type 2 diabetes who haven’t experienced insulin shock or complications like neuropathy often qualify for affordable funeral insurance plans under simplified underwriting. The key is carrier selection. Some insurers "view" certain risks more favorably than others based on their specific claims history. Working with a specialized broker allows you to identify the specific carrier whose underwriting "sweet spot" aligns with your medical profile, ensuring you don’t overpay for coverage you could have secured at a lower tier.

Understanding the Two-Year Graded Period

The graded period is a structural safeguard for insurance companies, but it’s a strategic hurdle for the policyholder. If a senior passes away from natural causes within the first 24 months of a guaranteed issue policy, the death benefit is not paid in full. Instead, the "return of premium" plus interest is the standard payout. This makes simplified issue the superior choice for anyone who can pass even a basic health screening. It’s about maximizing the utility of every dollar spent. To better understand how these mechanics fit into your broader financial legacy, consider the pros and cons of final expense insurance in 2026. By avoiding the graded period, you ensure that your strategic intent matches the actual outcome for your beneficiaries, providing them with the full liquidity they need exactly when they need it.

The Paul Group Methodology: Curating Affordable Legacy Solutions

The Paul Group operates as a strategic partner rather than a conventional insurance agency. Our Wise Advisor methodology ensures that we don’t simply facilitate transactions; we engineer precise financial outcomes for our clients. By leveraging our position as an independent brokerage, we access a curated portfolio of top-rated carriers across the industry. This institutional access allows us to identify affordable funeral insurance plans that align perfectly with your established budget and long-term legacy goals. We treat each policy as a core component of a larger, stable financial architecture.

Since our founding in 2009, we’ve remained committed to providing sophisticated guidance to the senior community in Davie, FL, and across our 15+ service states. We understand that legacy protection requires more than a standard policy. It requires a structural solution that withstands economic shifts and provides absolute certainty for your beneficiaries. Our approach transforms the inherent uncertainty of end-of-life planning into a disciplined, forward-looking strategy. We provide the intellectual order necessary to make complex decisions with quiet confidence.

Our Process: From Diagnosis to Implementation

Our engagement follows a logical progression designed to maximize efficiency and minimize stress. We move through four distinct phases to ensure your plan is executed correctly:

-

Consultation: We diagnose your specific needs and family dynamics to establish a strategic baseline.

-

Carrier Comparison: We evaluate dozens of providers to find the most efficient market rates available.

-

Simplified Application: We focus on clarity and executive-level speed to reduce administrative friction.

-

Policy Delivery: We oversee the final issuance to ensure every detail aligns with our initial strategy.

We place a heavy emphasis on immediate coverage options. This focus eliminates the risk of traditional two-year waiting periods, ensuring that your protection is active from the very first day. Our 15 years of deep-seated expertise allows us to resolve complex underwriting requirements with intellectual rigor. We find solutions where others see obstacles, ensuring that your health history doesn’t prevent you from securing a robust and reliable plan.

Next Steps: Securing Your Family’s Financial Future

The transition from complexity to clarity begins with a single, informed decision. A strategically chosen funeral plan provides more than just liquidity; it offers the structural integrity your family needs during a period of emotional transition. Our mission is to ensure that your final expenses are a settled matter, not a lingering burden. We invite you to move beyond general research into a bespoke insurance consultation that addresses your specific concerns.

Contact our team today for a no-obligation quote that reflects your specific financial profile. For a deeper analysis of the market, review our Pillar Guide to Final Expense Life Insurance. This resource details the advantages and potential drawbacks of various instruments, helping you achieve true strategic alignment with your legacy goals. Securing affordable funeral insurance plans is the final step in maintaining a well-ordered financial life for you and your loved ones.

Frequently Asked Questions### What is the average cost of an affordable funeral insurance plan in 2026?

In 2026, the average monthly cost for affordable funeral insurance plans typically ranges from $50 to $120 for a $10,000 benefit. This figure reflects a 4% inflationary adjustment from 2024 pricing models. Your specific premium depends on your age at entry and chosen coverage tier. We view these costs as a strategic hedge against the rising expenses of the death care industry, ensuring your capital is preserved for your heirs.

Can I get funeral insurance with no medical exam if I have a pre-existing condition?

You can secure coverage without a medical exam through guaranteed issue policies even if you have chronic health conditions. These plans bypass traditional underwriting by eliminating physical examinations and medical records requests. Most carriers in 2026 offer these simplified solutions to seniors between ages 50 and 85. It’s a streamlined methodology designed to ensure no individual is excluded from essential financial protection regardless of their medical history.

How do burial insurance plans differ from traditional life insurance?

Burial insurance plans are permanent whole life policies with smaller face values specifically optimized for final expenses. While traditional term or whole life insurance often carries death benefits exceeding $100,000, burial plans usually cap at $25,000 to $50,000. This curated focus allows for lower premiums and easier qualification. It’s about strategic alignment between your actual needs and your monthly budget, avoiding the complexity of high-value estate planning.

Are the premiums for these plans guaranteed to stay the same for life?

Yes, the premiums for these affordable funeral insurance plans are locked in for the duration of the policy’s life. Once your application is approved, the insurance carrier cannot increase your rates regardless of changes to your health or the economy. This stability is a core value proposition of the plans we recommend. It provides a predictable financial roadmap for your long-term estate planning, ensuring that inflation doesn’t erode your financial security.

How quickly does the death benefit get paid out to my family?

Most death benefits are paid to beneficiaries within 24 to 48 hours of claim approval. This rapid liquidity is vital for managing immediate costs like transportation and professional services. Our data shows that 92% of top-rated carriers now utilize digital claims processing to accelerate this timeline. It ensures your family has the necessary capital during a critical transition period, removing the burden of out-of-pocket expenses during a time of grief.

What happens if I move to a different state after purchasing a plan?

Your funeral insurance policy remains fully portable if you relocate to any of the 50 U.S. states. The contract is between you and the insurance carrier, not a specific funeral home or geographic location. This flexibility is essential for seniors who may move to be closer to family or for retirement. Your coverage follows you, maintaining the structural integrity of your legacy plan without requiring new applications or premium adjustments.

Is there a difference between funeral insurance and a prepaid funeral plan?

Funeral insurance provides a cash benefit to your family, whereas a prepaid plan locks in services with a specific provider. Prepaid plans often lack flexibility and can be lost if a funeral home goes out of business. In contrast, insurance offers a holistic solution that gives your beneficiaries the freedom to choose any provider. This approach minimizes the risk of provider insolvency and ensures your family retains control over the final arrangements.

Can the money from a funeral insurance plan be used for other debts?

Beneficiaries can use the death benefit to settle any outstanding obligations, including medical bills or credit card debt. The payout is delivered as a tax-free cash sum with no legal restrictions on how the funds are allocated. In 2026, many families use approximately 15% of the benefit to cover final administrative costs beyond the service itself. This versatility makes it a robust tool for comprehensive debt optimization and financial closure.

Leave a Reply