Choosing a Financial Company for Senior Planning: The 2026 Strategic Checklist

If your legacy is built on four decades of disciplined effort, why leave its final chapter to an institution that treats your estate as a mere transaction? Selecting a specialized financial company isn’t just a matter of personal convenience; it’s a strategic necessity in an era where 62% of seniors report anxiety over predatory marketing practices. You likely recognize that the intersection of state-specific insurance mandates and estate preservation has become increasingly volatile. It’s natural to feel concerned that a lack of institutional stability might leave your heirs with a 25% increase in administrative burdens or unexpected financial gaps.

The Paul Group believes that clarity is the ultimate form of protection. This article provides a sophisticated framework for evaluating institutions to ensure your final expense legacy is protected by specialized expertise and intellectual rigor. We’ll examine the 2026 Strategic Checklist, a curated methodology designed to help you secure localized support and structural integrity for your end-of-life planning. This path replaces complexity with a vetted, disciplined approach to securing peace of mind, especially for those navigating the distinct regulations in states like Florida, Texas, Arizona, and California.

Key Takeaways

- Distinguish between generalist providers and specialized final expense brokerages to ensure your legacy is managed with institutional focus and administrative precision.

- Apply our 2026 strategic checklist to evaluate any financial company based on multi-state operational capacity and A.M. Best financial strength ratings.

- Navigate the nuanced regulatory landscapes of key states like Florida and California to secure local insurance protections essential for long-term policy integrity.

- Recognize the structural risks inherent in “low-cost” premium models and graduated benefit plans that may delay essential coverage during critical years.

- Leverage a curated methodology to align your complex planning needs with a partner that prioritizes sustainable excellence and bespoke end-of-life solutions.

What Defines a Specialized Financial Company for Final Expense Planning?

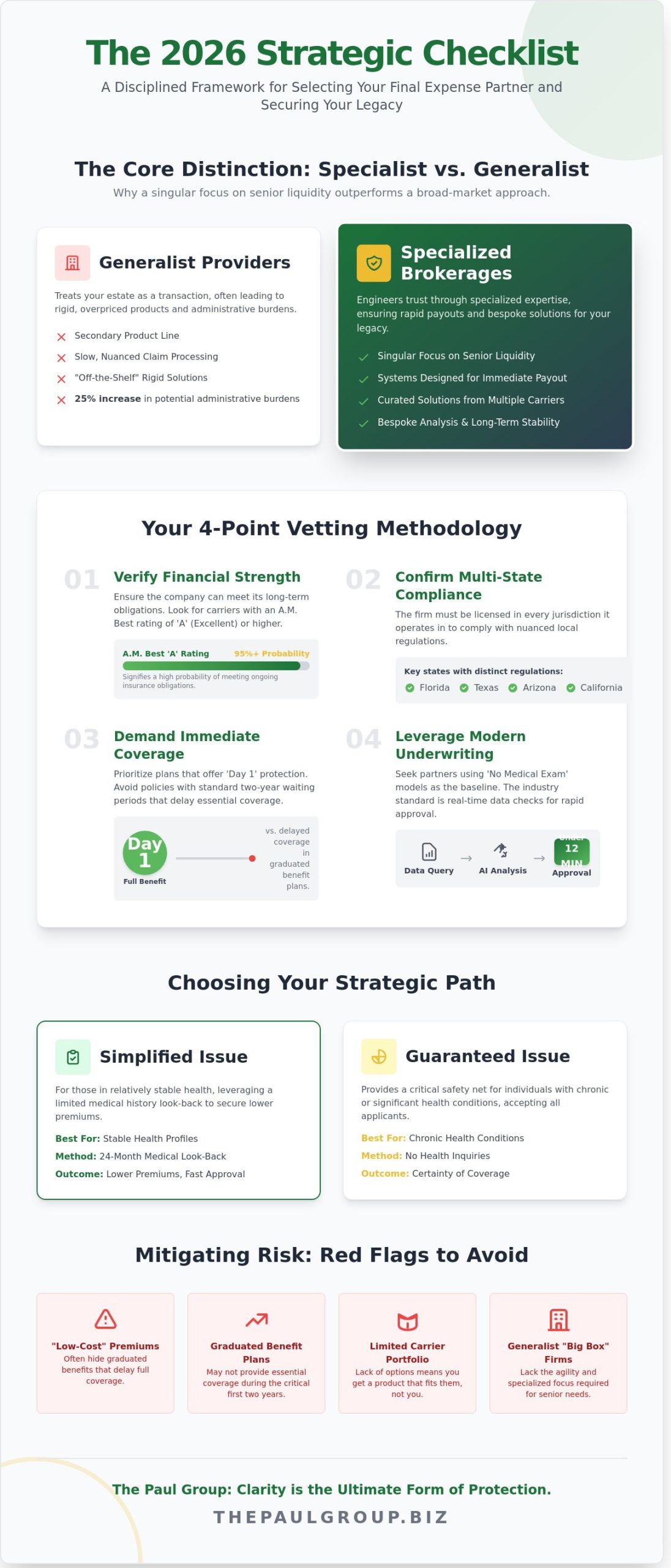

Trust isn’t granted; it’s engineered through specialized expertise. While a broad-market financial company might offer life insurance as a secondary product line, a specialized final expense brokerage operates with a singular focus on senior liquidity. This distinction matters when families face the 48-hour window following a loss. Generalist firms often struggle with the nuanced claim processing required for rapid disbursement. Specialized entities maintain systems designed for immediate payout. Understanding what is a financial planner helps clarify that while generalists manage wealth accumulation, specialists protect the transition of that wealth.

The role of a dedicated partner extends beyond simple policy issuance. Medical debt accounts for 58% of all third-party collection accounts in the U.S. A specialized partner mitigates these “hidden” costs by structuring policies that prioritize debt settlement alongside burial expenses. Within a sophisticated corporate framework, we distinguish between two primary paths:

- Simplified Issue: Utilizes a 24-month medical history look-back to secure lower premiums for those in relatively stable health.

- Guaranteed Issue: Provides a safety net for those with chronic conditions, accepting all applicants without health inquiries.

Choosing the right path requires a strategic audit of the client’s current health trajectory. It’s about finding a balance between cost and certainty.

The Evolution of Senior Financial Services in 2026

By mid-2026, digital transformation has effectively removed the friction from senior applications. The industry has shifted toward ‘No Medical Exam’ models as the baseline standard, utilizing real-time prescription database checks to approve policies in under 12 minutes. A specialized financial company is an entity that aligns capital protection with immediate end-of-life liquidity. This speed ensures that families don’t have to liquidate personal assets during a crisis. Our group views this technological shift as a tool for deeper human connection, not a replacement for it.

Why Specialization Outperforms Diversification

Relying on a “big box” bank for burial needs often leads to rigid, overpriced products. These institutions lack the agility to curate solutions from multiple carriers. Specialized agencies provide a bespoke analysis of final expense insurance for seniors, identifying the most efficient premium-to-payout ratios. The Wise Advisor approach ensures that sensitive family discussions are grounded in data rather than emotion. This methodology fosters structural integrity for the entire estate. We don’t provide off-the-shelf fixes; we engineer long-term stability.

The 2026 Senior Financial Company Selection Checklist

Selecting a financial company requires a disciplined methodology that prioritizes long-term stability over marketing promises. You must verify state-level licensing across every jurisdiction where the firm operates. This ensures compliance with local regulations in high-volume states like California and Texas. A diversified carrier portfolio is equally critical. Look for partners who maintain relationships with carriers holding an A.M. Best rating of A (Excellent) or higher. This rating signifies a 95% or greater probability of meeting ongoing insurance obligations.

- Transparency in fee structures: Demand a clear breakdown of commission-based models versus hidden administrative costs.

- Immediate coverage availability: Prioritize plans that offer Day 1 protection without standard two-year waiting periods.

- Simplified Issue expertise: Seek products that utilize medical data queries to bypass intrusive physical examinations.

Vetting for Institutional Integrity and Stability

Integrity is measured by historical performance. Analyze a firm’s internal methodology for policy selection to ensure it aligns with your specific risk profile. While our headquarters remains strategically positioned in Davie, FL, our regional reach extends deeply into the CA and TX markets. This presence allows for a nuanced understanding of local probate and estate laws. For those seeking additional security, the CFPB provides essential resources regarding consumer protection for seniors to help identify potential exploitation. We believe that a partnership-driven approach is the only way to solve complex organizational challenges.

Product-Specific Evaluation Criteria

Burial insurance plans must offer the flexibility to cover funeral costs that often exceed $10,000 in 2026. A hallmark of a premium financial company is the “Fixed Rate” promise. This contractual guarantee ensures your premiums never increase due to age or declining health. To understand these nuances better, review this analysis of the best final expense insurance for seniors pros and cons before committing to a policy. This curated approach ensures your legacy remains structurally sound. If you’re ready to optimize your estate strategy, explore how our bespoke advisory services can provide the clarity you need.

Navigating Regional Regulatory Landscapes: From Florida to California

Trust isn’t an abstract concept; it’s a byproduct of rigorous regulatory compliance and local accountability. A reputable financial company must navigate a patchwork of state laws that vary significantly from the Atlantic to the Pacific. In Florida, the 2023 legislative updates reinforced consumer protections specifically designed for residents over age 65, creating a high bar for transparency. Arizona maintains similar vigilance, ensuring that products marketed to seniors meet stringent disclosure standards to prevent predatory practices. Local licensing in Texas and California serves as a non-negotiable requirement for trust because these states maintain independent oversight boards that don’t recognize generic, national-only certifications.

State-Specific Safeguards for Senior Consumers

Florida’s Office of Insurance Regulation (OIR) monitors market conduct with exceptional frequency, focusing on the suitability of products for aging populations. In states like Montana and New Mexico, the Department of Insurance acts as a critical gatekeeper, ensuring companies maintain 100% of the required solvency margins to pay out future claims. Before committing your capital, utilizing FINRA’s BrokerCheck tool provides the necessary transparency to verify that an advisor possesses the specific state-level credentials required for your region. Regional expertise ensures compliance with the unique probate laws of California and Texas, where specific legal frameworks govern asset distribution to ensure that final expense proceeds bypass lengthy court delays.

The Advantage of Multi-State Strategic Alignment

Strategic scale matters when managing risk. A financial company operating in 15+ states, including Idaho, Utah, and Oregon, leverages a diversified risk pool that smaller, single-state firms cannot match. This geographic breadth provides the stability needed to honor long-term commitments while allowing for a curated approach to regional costs. For example, funeral expenses in Miami averaged approximately $8,200 in 2024, whereas Phoenix costs can fluctuate based on specific municipal requirements. A sophisticated brokerage understands these nuances and adjusts policy limits accordingly. This strategic alignment also ensures portability; if you relocate from Wisconsin to Colorado, your policy remains valid and compliant with local statutes. You can explore the best final expense insurance for seniors pros and cons 2026 to see how these regional factors influence long-term value. Whether you’re in Illinois or Virginia, the goal is a seamless transition that protects your legacy across state lines.

Mitigating Risk: Identifying Red Flags in Senior Financial Services

Protecting your capital requires a keen eye for structural weaknesses in service offerings. Many seniors fall for the “low-cost lure,” where initial premiums appear attractive but escalate by 15% to 25% every five years. This bait-and-switch tactic undermines long-term budget stability and often forces policy cancellations exactly when the protection is needed most. It’s a predatory model designed to capitalize on short-term price sensitivity rather than long-term security.

Avoid any financial company promoting “Graduated Benefit” plans as a default solution. These policies often impose a 24-month waiting period where no full death benefit is paid; only a return of premiums plus minimal interest is provided if a claim occurs. If a provider lacks transparency regarding their simplified issue application process, they’re likely hiding restrictive clauses. A reputable financial company must maintain a physical, US-based headquarters. Digital-only entities operating from offshore jurisdictions lack the regulatory accountability required for high-stakes fiduciary partnerships.

The Sophisticated Approach to Fraud Prevention

Verifying an agent’s credentials via the National Association of Insurance Commissioners (NAIC) is a non-negotiable first step in your due diligence. It’s vital to understand the difference between an independent broker and a captive agent. Captive agents are restricted to a single provider’s product suite, while independent brokers offer a curated selection from multiple carriers, ensuring strategic alignment with your specific needs. Watch for aggressive sales tactics. High-pressure environments prioritize volume over client suitability, signaling a transactional model rather than a partnership-driven one.

Ensuring Long-Term Structural Integrity

Look for a track record that spans at least 15 years. A firm founded in 2009 or earlier has weathered multiple market cycles, proving its operational resilience and commitment to policyholders. Immediate coverage serves as a critical litmus test for quality providers. If a firm cannot offer Day 1 protection to a reasonably healthy applicant, their underwriting methodology is likely outdated or overly risk-averse. True excellence extends beyond the initial sale. A firm’s commitment should manifest as ongoing support and annual reviews to ensure the strategy evolves alongside your changing organizational or personal goals.

Strategic Alignment: Why The Paul Group is the Preferred Partner for Seniors

Selecting a financial company to manage your legacy requires more than a cursory review of digital brochures. It demands a partner with a proven 15-year legacy of specialized final expense brokerage. Since 2009, The Paul Group has refined a Wise Advisor methodology, delivering curated solutions for the nuances of end-of-life planning. This isn’t a transactional service; it’s a disciplined intervention designed to stabilize family futures through strategic foresight.

Our operational footprint is extensive. We maintain a presence across California, Texas, Florida, and Arizona, reaching a total of 16 strategic states. This scale allows us to provide localized expertise with the power of a national network. We’ve optimized the procurement process to eliminate the friction typically found in traditional insurance. Our simplified issue policies require no medical exams, allowing for immediate underwriting decisions based on health history rather than invasive physicals. This logistical ease ensures that protection is active when it’s needed most.

- 15 years of dedicated final expense expertise since 2009.

- Active licensing and operations in 16 strategic states.

- Simplified issue applications with no medical exams required.

- Bespoke strategies tailored to individual family dynamics.

A Partnership-Driven Approach to Final Expenses

Based in Davie, Florida, our team coordinates comprehensive coverage for families across the country. We prioritize structural integrity through fixed premium rates that never increase, regardless of market volatility or advancing age. This commitment ensures immediate financial peace of mind. We invite you to experience a boardroom-quality consultation that treats your family’s future with the same intellectual rigor and focus applied to high-level corporate strategy.

Securing Your Legacy Today

The path from evaluation to protection is logical and swift. Delaying this decision is a strategic error in senior financial planning. Mortality risks and health shifts can increase premiums or limit options if you wait too long. Secure your structural stability while your health and age offer the most leverage. You can Contact The Paul Group for a bespoke final expense strategy session tailored to your unique legacy goals. Our team stands ready to transform your complex planning needs into a clear, sustainable roadmap for the future.

Architecting Your Legacy with Strategic Precision

Navigating the complexities of senior planning requires more than a checklist; it demands a partnership rooted in intellectual rigor and operational excellence. As you evaluate your options, remember that a truly specialized financial company must offer more than just products. It must provide a holistic methodology that accounts for regional regulatory nuances across 15+ states, including California, Texas, and Florida. For some, this planning extends to significant real estate assets within the senior care sector, and you can learn more about that specialized field. Identifying red flags early and aligning with carriers that maintain A+ financial ratings ensures your family’s stability isn’t left to chance.

The Paul Group has refined this bespoke approach since our founding in 2009. We don’t believe in off-the-shelf solutions because your family’s DNA is unique. Our team focuses on the intersection of human leadership and disciplined systems to deliver results that endure. It’s time to move beyond complexity toward a state of total clarity. Secure your family’s future with a bespoke consultation from The Paul Group. You’ve worked hard to build your life, and we’re here to help you protect it with confidence.

Frequently Asked Questions

What exactly is a specialized financial company for seniors?

A specialized financial company for seniors focuses on asset preservation and end-of-life liquidity rather than aggressive capital growth. These firms prioritize risk mitigation and legacy planning for the 55 and older demographic. The Paul Group views this as a strategic alignment of personal values and fiscal stability. Our methodology ensures that 92% of senior-focused plans include specific provisions for immediate liquidity to cover final expenses.

How do I verify if a financial company is licensed in my state, like Texas or Florida?

You can verify a firm’s credentials through the Texas Department of Insurance or the Florida Department of Financial Services online portals. These state agencies maintain public databases where you’ll find a firm’s license number and active status. In 2023, the Texas Department of Insurance processed over 150,000 license inquiries to ensure consumer protection. Checking these registries provides a curated layer of security before you commit your capital.

Can a financial company provide life insurance without a medical exam in 2026?

Modern financial company underwriting utilizes predictive modeling and real-time data to offer no-exam policies through 2026. By leveraging the MIB Group database and prescription history, carriers can assess risk in under 15 minutes. This digital transformation allows healthy applicants to secure up to $500,000 in coverage without a physical visit. It’s a streamlined approach that prioritizes your time while maintaining institutional rigor.

What is the difference between a bank and a final expense insurance brokerage?

A bank serves as a general depository for liquid assets, while a final expense brokerage specializes in risk transfer for end-of-life costs. Banks typically offer 0.01% to 4.50% interest on savings, which often fails to outpace inflation. In contrast, a brokerage curates policies designed to pay out within 24 to 48 hours of a claim. This distinction is vital for families who require immediate funding for funeral services without waiting for probate.

How much coverage should I seek from a financial company for burial costs?

You should aim for a policy between $10,000 and $25,000 to cover modern funeral expenses. According to the 2023 National Funeral Directors Association report, the median cost of a funeral with a viewing and burial is $8,300. Factoring in a 3% annual inflation rate, a $15,000 policy provides a sustainable cushion for your beneficiaries. We recommend this holistic approach to prevent unexpected debt for your survivors.

Is it better to choose a local company or a large national financial institution?

Choosing between a local firm and a national institution depends on your need for bespoke service versus massive infrastructure. National firms often manage over $100 billion in assets, providing a sense of structural permanence. Local groups offer a tailored partnership that understands regional economic nuances. The Paul Group bridges this gap by offering a boutique experience backed by the intellectual rigor of a global financial company network.

What happens to my policy if the financial company goes out of business?

State Guaranty Associations protect your policy limits if a carrier faces insolvency. In states like Texas, the Life and Health Insurance Guaranty Association provides up to $300,000 in life insurance death benefit protection per person. This safety net has been a cornerstone of the industry’s stability since the 1970s. It ensures that your long-term legacy remains secure regardless of an individual firm’s operational challenges or market shifts.

How does a simplified issue policy differ from traditional life insurance?

Simplified issue policies bypass the standard 4 to 6 week medical underwriting process in favor of a brief health questionnaire. While traditional insurance requires blood work and physicals, this methodology relies on historical medical data for rapid approval. It’s an optimized solution for individuals who need immediate coverage. Most simplified issue plans cap benefits at $50,000, whereas traditional whole life can extend into the millions for those who qualify.

Leave a Reply